Investment Summary

S&P/NZX All Information Technology (Sector) (Gross with Imputation) vs S&P/NZX50 Index (Source: Refinitiv (Thomson Reuters))

The technology sector of New Zealand is a combination of high-tech manufacturing and ICT that features high levels of connectedness, innovation, and expenditure on R&D. New Zealand offers a strong technology ecosystem. It ranks first in the world for ease of doing business, being the least corrupt nation, having a skilled workforce, sound financial markets, and stable political and regulatory environment. The enabling environment so created, has led to the emergence of high growth technology companies with world-leading ambitions. The top 200 tech exporting companies are attracting significant investment from all over the world.

Key Data (Source: NZTech)

According to last year’s TIN report, the 200 largest tech exporters had a combined revenue of $12.1 billion, reflecting a rise of 10% from 2018. There were 28 new technology sector jobs which were created in Northland and 212 in Waikato, 95 in the Bay of Plenty, 113 in Canterbury and 21 in Otago in 2019.

Exports grew by 5.4% in 2019 to reach $7.4 billion. The top 200 exporters managed to generate $8.7 billion with respect to overseas sales in 2019, up 11.3% from 2018.

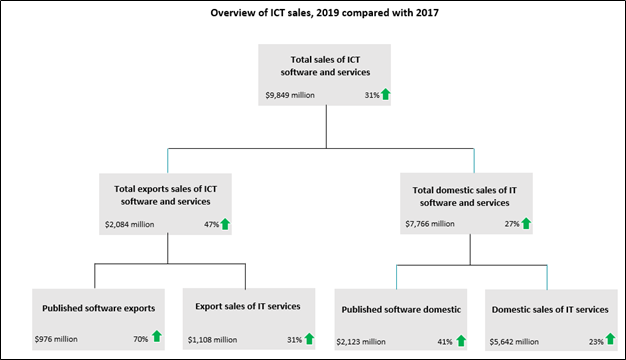

Overview of ICT Sales (Source: Stats NZ)

Far Reaching Impact Across All Sectors

As the tech sector grows, development of other industries can also be witnessed. The internet and cloud services are allowing firms to move their operation faster and reach international markets. New computing platforms are significantly lowering the costs of doing business, and technology innovations are transforming the way businesses work to improve their productivity.

Digital Technologies to Disrupt Manufacturing Sector

The country’s manufacturing industries make a crucial contribution to the national economy. Digital technologies have started to disrupt the manufacturing sector as they have done with the other sectors like the media and finance. New computing capabilities as well as increasing data, together with advances in robotics, automation, additive technology, AI and human-machine interfaces are releasing innovations, thereby, disrupting manufacturing. Key benefits include reduction in costs, quality improvement, and new product launches at a faster pace.

NZIER has calculated that an upgrade of 4% in tech sector productivity would go through manufacturing sector and will also be raising GDP by about $700 million.

Retail Sector Focused on Better Customer Experience

With the rise in tech productivity, the retail sector would respond strongly via various benefits of improved inventory management, latest sensor technology, better connectivity to retail services and more effective relationships between retailers as well as customers.

Fastest Growing NZ Fintech Sector

The fintech sector has the potential to provide the best opportunities for future economic growth in New Zealand.

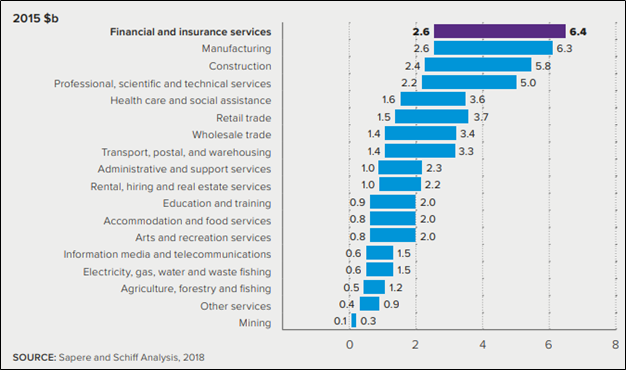

Estimated Ranges of Economic Benefits of Labour Efficiencies from AI in New Zealand Industries in 2035 (Source: NZ Tech)

Digital Technologies: Life-line of NZ Economy

Whether it is agri-tech which helps produce more food for the country, biotech which helps improve health and fintech which redefines the way people borrow, lend, spend and transfer money, they all are helping New Zealand prosper into the future. Fintech is the fastest growing among them, growing at 33.2%.

There has been rapid rise in the number of IT firms. In 2019, the number of tech firms in New Zealand increased by 3% to 21,870. A strong pipeline of promising startups is expected to drive continued growth. Given the image of high-quality product producers, some of these small firms may emerge one day as major exporters of software from the country.

Headwinds Faced by Technology Sector

However, there have been discussions on how technology affects jobs, whether and how technological forces are shaping work, and how New Zealanders should best prepare for the change in the future.

New Zealand’s future prosperity will largely depend on how well it is able to adopt technology rather than treat technology as a threat. The government needs to remove all restrictions to firms adopting technologies.

Since we now have a broad idea of technology sector, it is important to look at the performance of some companies operating in the same sector.

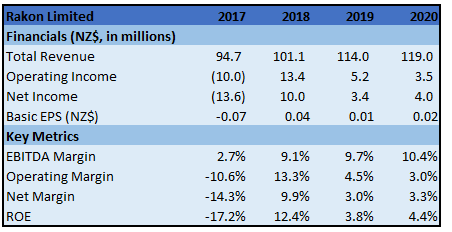

1. Rakon Limited (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$89.332 Million)

Business Description: Rakon Limited (NZX: RAK) designs and manufactures advanced frequency control and timing solutions. Its three core markets are Global Positioning, Telecommunications and Space and Defence.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company’s market share is growing in the high precision sub-segment for low g-sensitivity products, and this movement is likely to be continued. In the high-volume sub-segment, competitive difficulties from global positioning module makers in Asia are anticipated to raise price pressure; however, considering the company’s alliance with low-cost manufacturer Taiwan-based Siward Crystal Technology Co. Limited, there are expectations that the company will remain competitive.

Key Risks: The company is having exposure to risks like credit risk, liquidity risk and market risk.

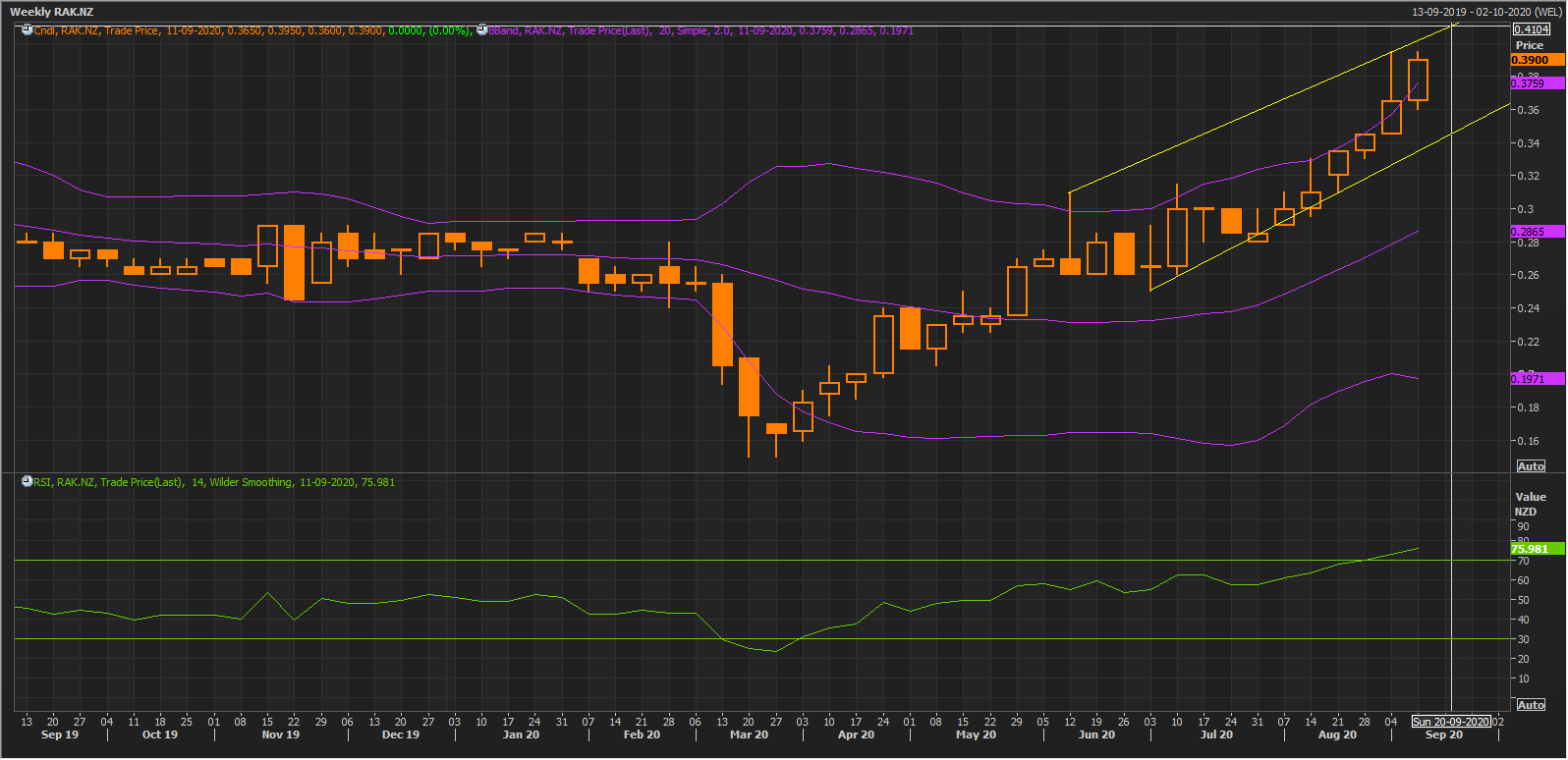

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has been in a strong uptrend. In the process, it has entered into uncharted territory, trading above the upper Bollinger band. The technical indicator RSI with around 76 reading and curve at the end pointing up, suggests stock to have reached into a highly overbought zone.

Going forward, the stock may have resistance around $0.410 whereas support could be around $0.345, as have been derived by trendline analysis.

Valuation: On TTM basis, the company's EV/EBITDA multiple stood at 8.4x as compared to industry average (Industrials) of 9.0x. Its P/BV multiple stood at 1.0x while the industry average is 1.9x.

We give a “Speculative Buy” at the current price of NZ$0.390 per share on September 10, 2020.

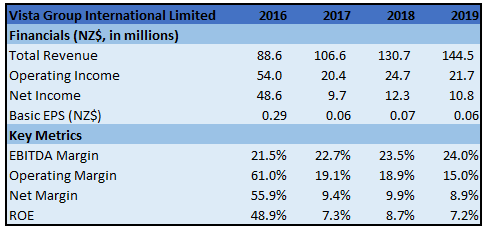

2. Vista Group International Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$422.94 Million, Dividend Yield: 0.84%)

Business Description: Vista Group International Limited (NZX: VGL) is in the business of providing software and additional technology solutions throughout the global film industry sectors of distribution, exhibition, as well as consumer.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has undertaken a thorough review of its businesses. Consequently, it has started the discussion with its staff over a proposed new structure for the core Vista Group companies that are Vista Cinema, Vista Group and Movio. This proposal gives a new organisational structure worldwide, a structure with fewer people as compared to present status.

Key Risks: The shutdown caused by COVID-19 has severely impacted the company’s trading performance and will continue to have an impact until cinemas are able to open in a meaningful way.

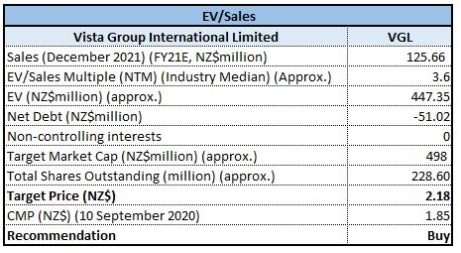

Valuation: We have applied EV/Sales multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

We give a “Buy” at the current price of NZ$1.85 per share on September 10, 2020.

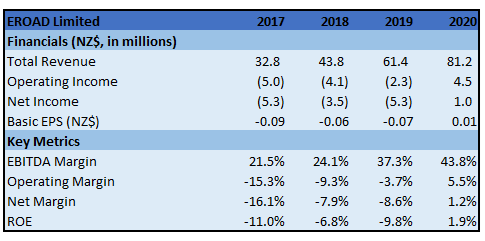

3. EROAD Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: ~NZ$297.11 Million)

Business Description: EROAD Limited (NZX: ERD) develops technology solutions that handle vehicle fleets, improve driver safety, support regulatory compliance, as well as reduce costs related to driving.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: Regardless of economic insecurity across all markets, the company is well-positioned for FY21. This is mainly because of its future contracted income, strong customer value proposition, and diverse customer base throughout regions, business size and industry. While ambiguity results in longer sales lead-times, it remains confident in continued unit growth across all 3 markets, although it is likely to be less than delivered in FY20 and previously expected for FY 2021.

Key Risks: The company has exposure towards credit risk, liquidity risk and market risks which include commodity price risk, foreign currency risk as well as interest rate risk.

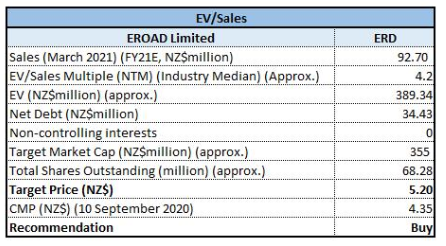

Valuation: We have applied EV/Sales multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

We give a “Buy” at the current price of NZ$4.35 per share, up by 1.16% on September 10, 2020.

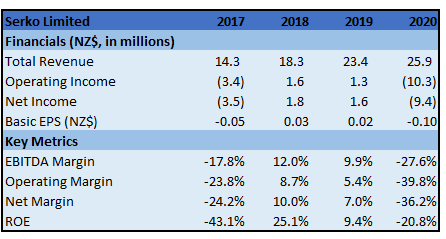

4. Serko Limited (Recommendation: Hold, Potential Upside: Higher Single-Digit), (M-Cap: ~NZ$398.83 Million)

Business Description: Serko Limited (NZX: SKO) is a market-leading travel and expense technology solution provider.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company considers itself to be well-positioned for growth when the travel industry recovers, and trading conditions start to improve. The company has a strong hold in Australasia, with its major transactions being domestic and Trans-Tasman in home markets. The company now mainly focuses on domestic travel within North America, where it has been adding resellers to its platform and continue the development work in order to localise content.

Key Risks: The company’s activities expose it to the travel industry, which currently is under a lot of pressure. The revival of travel industry is still uncertain and, hence, the recovery is also expected to be delayed.

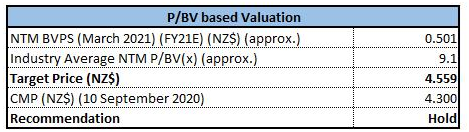

Valuation: We have applied P/BV multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of higher single-digit (in % terms).

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

We give a “Hold” at the current price of NZ$4.300 per share on September 10, 2020.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...