Summary:

Transport sector in New Zealand can be considered as the backbone of broader economic development, and the growth of the industry is primarily helped by government support, stable and favourable business environment and robust fundamentals. Broader transport sector consists of port and freight services along with aviation services. It can be said that the export revenue is the lifeline of the broader economic growth in New Zealand. External trade, significant opportunities and policy support are the key factors responsible for the overall growth in the port business. Increased demand, support of government and headroom for significant investments are the key factors influencing the broader aviation space.

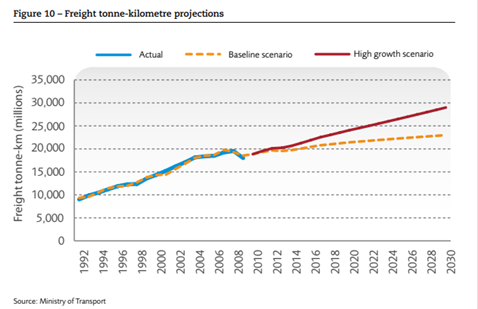

Key Data (Source: Ministry of Transport)

Overview of Transport Sector

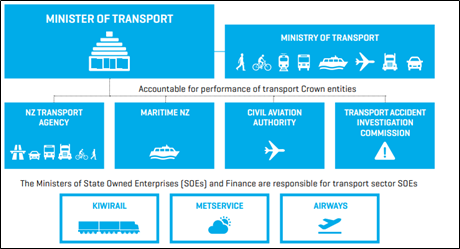

The government transport sector is comprised of five specialist transport agencies and three State-Owned Enterprises.

The Government Transport Sector (Source: Ministry of Transport)

The Ministry is the government’s principal adviser on transport policy. The Ministry advises the government on all issues relating to transport and the regulatory framework that supports it.

The Ministry has three key functions:

There are three transport-related State-Owned Enterprises (SOEs):

KiwiRail is responsible for operating freight and tourism passenger services on 3500 kilometres of the rail network and three interisland ferries. KiwiRail also provides the rail network for Auckland and Wellington metro rail services.

MetService’s core purpose is to provide weather services that support the safety of life and property and, as an SOE, add value to the New Zealand economy.

Airways provides air navigation services, which enable safe, reliable, and efficient air transport within New Zealand airspace, and across the Pacific Oceanic Flight Information Region, one of the largest airspace regions in the world.

Port Sector: A Key Driver for Growth in International trade

The country is very much focused on port productivity, driving greater performance and value for money from maritime, improving maritime safety, and improving public information on the performance of maritime and freight transport.

Sea export value has increased with the growth of dairy and wood exports, but the prices of those commodities have experienced a decline. Bulk sea export to China have grown significantly, but of late, they are sluggish. Much of the containerized growth has been to the Chinese market.

A Look at Government’s Support Initiatives: Announcement of Aviation Relief Package

On March 19, 2020, Transport Minister, Phil Twyford, outlined the first tranche of $600 million aviation sector relief package which is a part of the Government’s $12.1 billion COVID-19 economic response. The initial part of the aviation package aims to secure the operators of New Zealand’s aviation security system and includes:

Challenges and Risks In Transport and Logistics Industries

Increased use of technologies at trucking companies and in port services has led to better optimization of space and distances travelled. This places small players who cannot afford the technologies at a distinct price disadvantage. Thus, the behaviour change, facilitated by technology, is leading to lower demand and restricted logistics services growth.

Exports of late have been affected by a slowdown in the global economy as a result of outbreak of trade war involving leading economies and then with the outbreak of COVID-19 which forced many nations to impose lockdown on themselves, thereby, disrupting trade activities. Fortunately, there has been an improvement in the situation at COVID-19 front in some parts of the world, but the majority are still struggling with the issue.

Drivers of Transport Sector in New Zealand: The Road Ahead

The governments across the world have resorted to huge fiscal and monetary stimulus to help recover their respective economies from the crisis. Hopefully, things may change in short-to-medium term and trade will be back to normal. Any revival in trading sentiment will lead to a steeper rise in global trade. Moving forward, resilient nature of the broader transport sector, opening up the economies, stable business policies and increased investments are expected to act as primary growth drivers. Overall, increased investments and better demand scenario place the broader transport sector in a lucrative position.

With the gradual opening of the global economies, the transport sector in NZ might witness positive impacts. We will now have a look at 4 companies operating in this space (AIA, MFT, NPH, MMH).

1. Auckland International Airport Limited (NZX: AIA) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$9.36 billion, Gross Dividend Yield: 2.434%)

Business Description: Auckland International Airport Limited is the third busiest international airport in Australasia. The airport plays a significant role in supporting New Zealand businesses, with around $15 billion worth of freight passing through the airport every year.

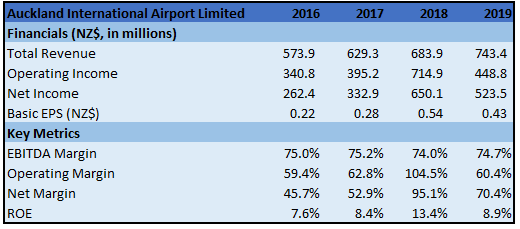

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The airline has suspended underlying earnings guidance for the current financial year due to the significant uncertainty surrounding the duration and impact of COVID-19 travel restrictions on the business. It responded quickly to the disruption of tourism and aviation markets through a comprehensive plan to bolster liquidity, reduce operating costs and suspend or terminate capital expenditure. Some of the measures include deep cuts to discretionary expenditure, reviewed and suspended external consulting work, reduced the number of external contractors supporting the capital programme and wider business, reduced remuneration of directors and executives to 80% and lowered most other employees’ hours/salaries to 80%.

Key Risks: The airport company is exposed to constant risk of any major events like natural calamities, pandemics, airline crashes and terrorism.

Valuation: On a TTM basis, EV/Sales multiple of the stood at 21.7x which is higher than the industry average (Industrials) of 23.2x. Also, its P/B multiple came in at 1.6x as compared to industry average of 4.8x. Therefore, it can be said that the stock is slightly undervalued.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Green colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock had softer close in the previous week at its weekly low. However, it seems to have gained strength in uptrend in the on-going week having given close above 20 period SMA and 38.2% retracement level. Technical indicator RSI with around 45 reading suggests gaining of bullish momentum.

Going forward, the stock may have resistance around 61.8% retracement level of $7.75 while support could be around 23.6% retracement level of $5.58.

Thus, we give a “Buy” recommendation on the stock at the current price of NZ$6.360 per share.

2. Mainfreight Limited (NZX: MFT) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$3.96 Billion, Gross Dividend Yield: 2.067%)

Business Description: Mainfreight Limited (NZX: MFT) provides international and domestic freight forwarding and managed warehousing. The company has its team and branches across China, Australia, New Zealand, Europe, and the Americas Mainfreight continues to grow its global footprint.

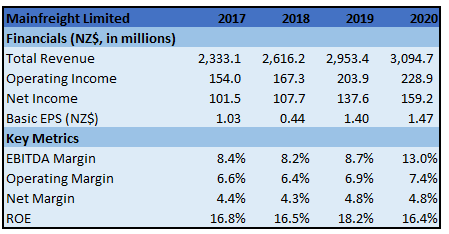

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company reported satisfactory results in the past year. However, COVID-19 pandemic had a significant impact and is expected to affect economic conditions for some time. While freight remains able to cross borders, slowing consumer demand will see freight volumes and supply chain activity contracts. The company has been positively surprised at the levels of activity in New Zealand, Australia, Asia, and some parts of Europe, and this has been reflected in their estimated weekly profits in April and May.

Key Risks: The main risks arising from the company’s financial instruments are cash flow interest rate risk, fair value interest rate risk, liquidity risk, foreign currency risk and credit risk. Its exposure to cash flow risk through changes in market interest rates relates primarily to the Group’s long-term debt obligations with a floating interest rate. The company is also exposed to currency risk as a result of its operations in Australia, America, Europe, and Asia.

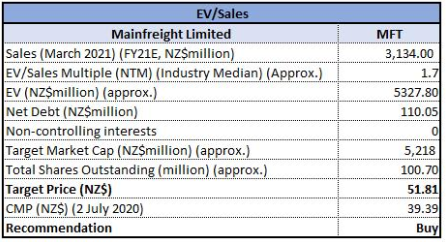

Valuation: In FY 2020, the company’s operating cash flows amounted to $300.80 million ($200.16 million pre-NZ IFRS 16), reflecting a rise from $197.42 million in the previous year, implying increased profitability as well as acceptable cash collection. We have applied EV/Sales Based Relative Valuation (on an illustrative basis) and the target price reflects a rise of lowe double-digit (in % terms).

EV/Sales Based Relative Valuation (Illustrative)

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

3. Napier Port Holdings Limited (NZX: NPH) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$721.55 Million, Gross Dividend Yield: 0.962%)

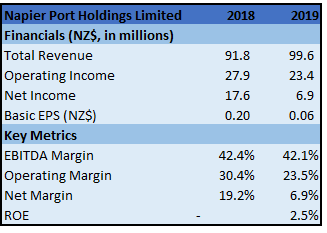

Business Description: Napier Port Holdings Limited is New Zealand’s fourth-largest port by container volume. It is the main gateway for Hawke’s Bay exports and operate a long-term regional infrastructure asset that supports the regional economy.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The timing of recovery and the future trade outlook of the cruise industry is still uncertain and is now totally dependent on public health developments of COVID-19 and the economic impact in the country. The company continues to interact with the owners of cargo to understand the impact of COVID-19 on operating conditions and how it is influencing them. The company remains focussed on supporting and working with customers and region and continuing to operate as an agile and resilient gateway to world markets.

Key Risks: The company’s activities expose it to a variety of financial risks, including credit risk, liquidity risk, foreign currency risk and cash flow interest rate risk.

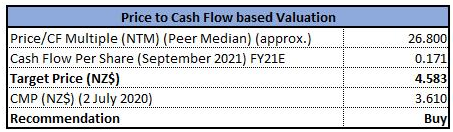

Valuation: The company is possessing a robust balance sheet after the capital raising in the previous year. Additionally, the company has undrawn bank facilities amounting to $180 million, the majority of which mature in 2024. We have applied P/CF Based Relative Valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms).

P/CF Based Relative Valuation (Illustrative)

P/CF Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

4. Marsden Maritime Holdings Limited (NZX: MMH) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$268.45 Million, Gross Dividend Yield: 3.467%)

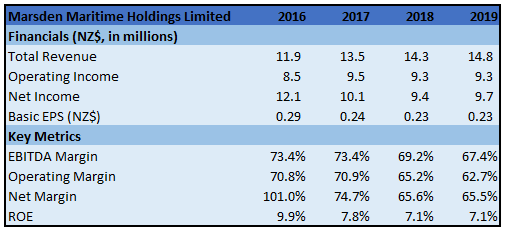

Business Description: Marsden Maritime Holdings Limited is a designated Port Company with stake holdings in several business activities in the Greater Marsden Point Area, including port operator, Northport Ltd. A key focus of the company is to attract business to the port area, through long-term lease arrangements on land owned adjacent to the port.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: Due to the disruption in current market condition because of COVID-19, the company expects a slowdown in log export through Northport from the levels seen over the first six months and therefore a softening of the expected year-end result. The company is still unable to quantify the potential financial impact currently and is closely monitoring changes to trading patterns, particularly as it affects log export through Northport and the key Chinese destination market.

Key Risks: The company’s activities expose it to a variety of financial risks including movements in fair value, liquidity risk, credit risk, price risk, interest rate risk and to a lesser extent foreign exchange risk.

Valuation: On a TTM basis, the stock’s EV/Sales multiple stood at 18.2x as compared to industry average (Industrials) of 23.2x. Also, its P/B multiple came in at 1.9x while industry average was 4.8x. Therefore, it can be said that the stock is slightly undervalued.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Green colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has given close around $6.50 at its peak price of the on-going week. A closure looks at the chart reveals that the stock has formed Bullish Rectangle which is towards confirmation of continuation of bullish trend. Technical indicator RSI with around 53 reading, suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around $7.05, as provided by upper Bollinger band while support could be around 50% retracement level of $6.26.

Thus, we give a “Buy” recommendation on the stock at the current price of NZ$6.500 per share.

.png)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...