Company Overview: Precinct Properties New Zealand Limited (NZX: PCT) is engaged in investing in prime central business district properties in New Zealand. The company owns inner-city business spaces in Auckland and Wellington.

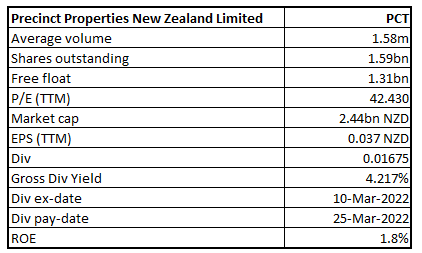

PCT Details

Precinct Properties New Zealand Limited (NZX: PCT) is the largest owner and developer of premium inner-city business space in Auckland and Wellington. The market capitalisation of the company stood at ~$2.44 billion on 28th March 2022.

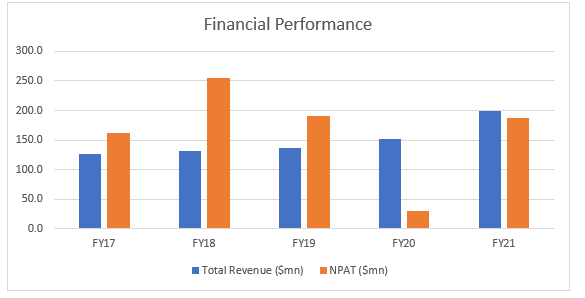

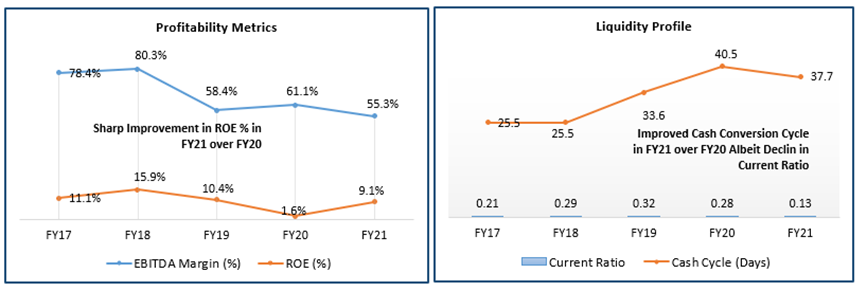

Looking at the past performance over FY17 to FY21, PCT’s top line and bottom line grew with a compounded annual growth rate (CAGR) of 12.17% and 3.73%, respectively. PCT’s total revenue improved from $126.2 million in FY17 to $199.8 million in FY21. NPAT grew from $162.1 million in FY17 to $187.7 million in FY21.

Exhibit 1: Financial Statistics

Source: Analysis by Kalkine Group

Result Performance for H1FY22 (6 Months Ended 31 December 2021)

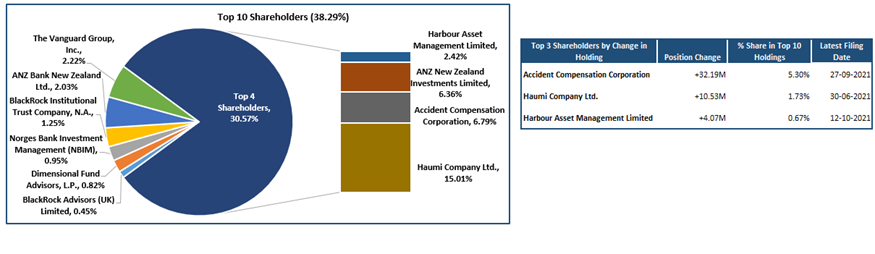

Top 10 Shareholders:

The top 10 shareholders have been highlighted in the table, which together forms ~38.29% of the total shareholding.

Exhibit 2: Top 10 Shareholders

Source: Analysis by Kalkine Group

A Quick Look at Key Metrics: In FY 2021, the company has posted net margin of 93.9% as compared to the industry median of 69.2%. Therefore, it could be said that PCT possesses better capabilities to convert its top line into bottom line. Its ROE stood at 9.1% as compared to the industry median figure of 8.8%.

Exhibit 3: Key Metrics

Analysis by Kalkine Group

Recent Updates:

On 21 December 2021, PCT announced that it committed to the development of 124 Halsey Street and the Flowers Building, which is the third stage of the master-planned Wynyard Quarter Innovation Precinct.

Outlook:

PCT is focused on the next stage of its strategic evolution and has been actively identifying value add opportunities and progressing them over the first half of FY22. The establishment of its third-party platform and diversifying its capital sources enabled the business to grow to take advantage of any future market opportunities.

The Board expects an FY22 dividend of 6.70 cps, representing a 3.1% YoY growth in total cash dividends to shareholders. In addition, the Board expects to see PCT’s dividend payout ratio modestly exceed 100% of its AFFO.

Risks:

The company is exposed to credit, market, and liquidity risk that arises in the normal course of the business. The company is also prone to the risks associated with COVID-19. PCT is subject to complying with stringent regulations in order to operate.

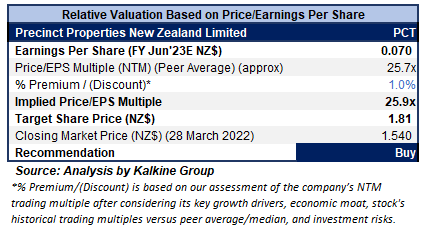

Valuation Methodology: Price/EPS Based Relative Valuation (Illustrative)

Technical Overview

Chart

.png)

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Performance:

Despite ongoing impacts to the business, the company will continue to leverage the quality and resilience of its portfolio and people. PCT’s gearing level, as measured under borrower covenants, is well under PCT’s borrower covenant level of 50%, at 31.8%. The company has demonstrated robust resilience in the operating performance considering that the majority of the business was impacted by lockdowns during the first half.

The stock has been valued using Price/EPS based relative valuation (on an illustrative basis), and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to Price/EPS Multiple (NTM) (Peer Average) considering the decent outlook and increased NPI.

Considering the above facts and its current trading levels, we give a “Buy” recommendation on the stock at the closing market price of NZ$1.540 per share, down by 1.60% on 28th March 2022.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

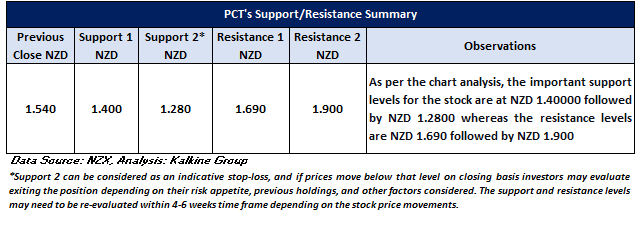

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...