Precinct Properties New Zealand Limited (NZX: PCT) is engaged in investing in prime central business district (CBD) properties in New Zealand. It invests mainly in premium A-grade commercial office property. The Company owns inner-city business spaces in Auckland and Wellington. The company offers its buildings to businesses and government organizations, including Air New Zealand, ANZ, Microsoft, PwC, The Treasury, State Insurance and Zurich.

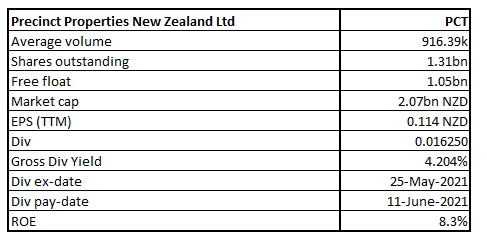

PCT Details

Precinct Properties New Zealand Limited (NZX: PCT) is the largest owner and developer of premium inner-city business space in Auckland and Wellington. The company has a market capitalization of ~$2.07 billion as on May 31, 2021.

Looking at the past performance, PCT’s topline for FY16-20 grew at a decent compounded annual growth rate (CAGR) of 0.98%. Its total revenue for FY20 stood at $151.8 million, as compared to $146.0 million in FY16.

Results Performance (Half-Year Ended 31st December 2020 – H1FY21)

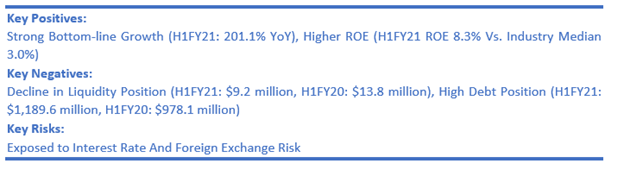

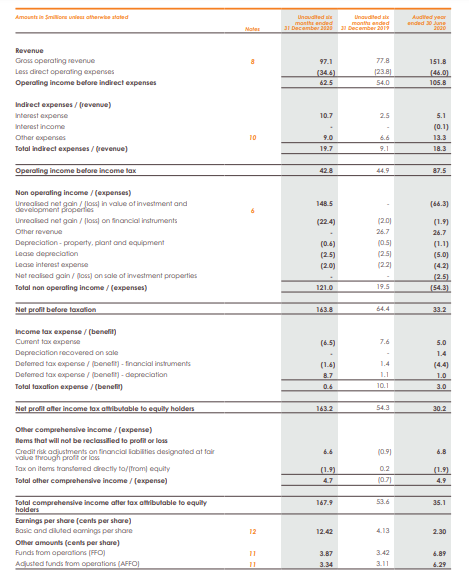

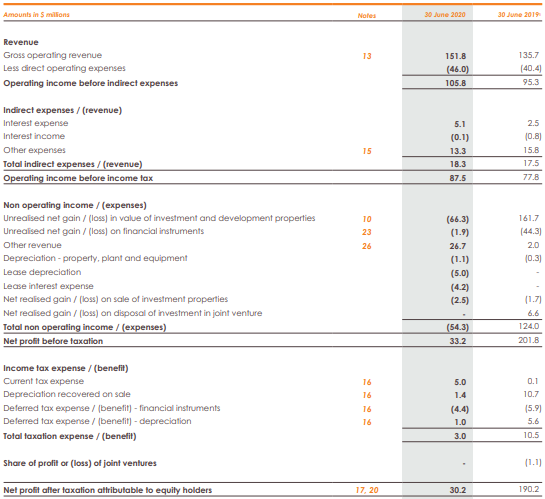

The company’s total comprehensive income after tax for the interim period stood at $167.9 million, an increase of 213% on the previous corresponding period (pcp). This can be attributed to a strong half-year portfolio revaluation gain of $148.5 million. Operating income for the period stood at $62.5 million, an increase of 15.7% on pcp as a result of the completion of developments.

Adjusted funds from operations (AFFO), which adjusts for several non-cash items stood at $43.8 million, an increase of 7.4% on pcp. The balance sheet remains in a strong position with a gearing of 29.9%, as compared to 28.8% in June 2020.

The period witnessed occupancy levels of 98% similar as in June 2020, on a weighted average lease term (WALT) of 7.7 years, as compared to 8.0 years in June 2020. Generator performance impacted over the short term due to Covid, however, demand is recovering strongly, and the outlook is positive. Commercial Bay operating income lower for the first half due to timing impacts from Covid following delays in opening. Trade performance continues to track in line with expectations after adjusting for no international visitors.

The Board of Directors declared a dividend of 3.25 cps during the period.

Exhibit 1: Income Statement of H1FY21

(Source: Company Reports)

Results Performance (Year Ended 30th June 2020)

The company reported a total comprehensive income after tax of $35.1 million for FY20 in line with guidance. The adjusted funds from operations (AFFO) for the period stood at 6.29 cents per share (cps), an increase of 5.9% YoY.

The company’s portfolio benefited from high occupancy and a long WALT during the year with portfolio occupancy maintained at 98% and a WALT of 8.0 years.

The Board of Directors declared a full-year dividend of 6.30 cps, an increase of 5.0% YoY.

Exhibit 2: Income Statement FY20

(Source: Company Reports)

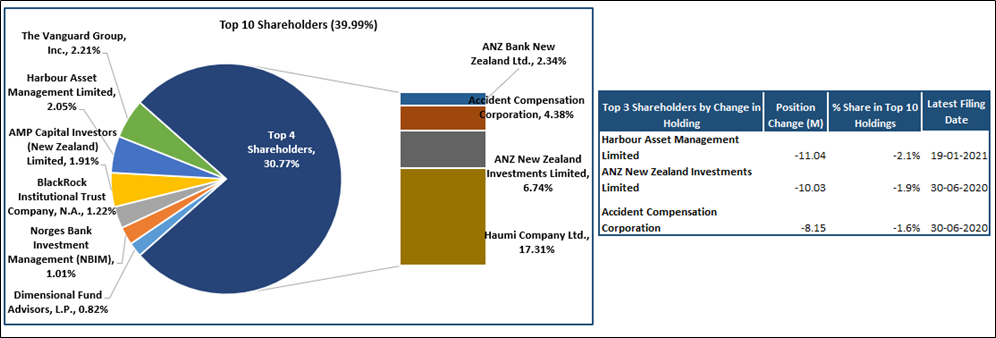

Top 10 Shareholders: The top 10 shareholders have been highlighted in the pie chart, which together form around 39.99% of the total shareholding. Haumi Company Ltd. and ANZ New Zealand Investments Limited are holding a maximum stake in the company at 17.31% and 6.74%, respectively, as provided in the table below:

Exhibit 3: Top 10 Shareholders

Source: Analysis by Kalkine Group

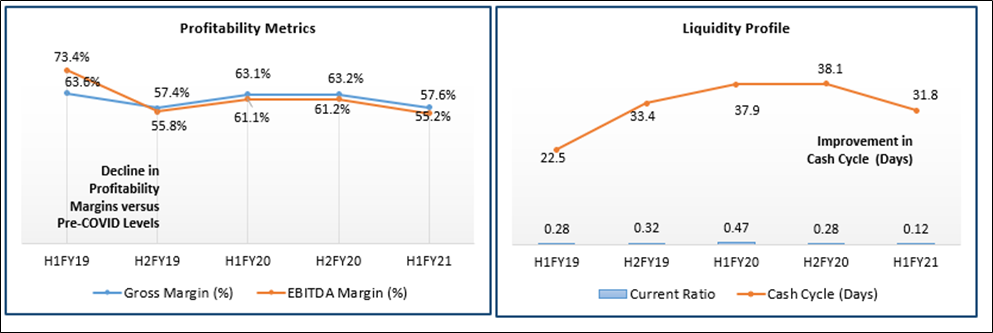

A Quick Look at Key Metrics: The company’s gross margin and EBITDA margin experienced contractions during the interim period after a prior year of consistent performance. The period witnessed improvement in cash cycle days to 31.8 days from H2 FY 2020 figure of 38.1 days. However, current ratio for the period declined to 0.12x as against 0.28x in H2 FY 2020.

Exhibit 4: Key Metrics

Source: Analysis by Kalkine Group

Recent Updates:

Under dividend update, the company has declared a second-quarter dividend of 1.625 cps with the payment date on 26 March 2021 which takes the total dividend to 3.25 cps during H1FY21 as against 3.15 cps in H1FY20. The H1FY21 dividend accounted for around 98% of its H1FY21’s AFFO of 3.34 cps. Meanwhile, the company has guided for the FY21 dividend to be maintained at 6.50cps.

On May 24, 2021, the company informed the market about the completion of a comprehensive re-design, construction of the One Queen Street redevelopment which is expected to comprise a luxury hotel, premium office accommodation and a variety of unique food and beverage options. Importantly, the revised scheme remains fully integrated into the Commercial Bay retail precinct.

As per another update on May 12, 2021, the company announced further leasing progress at 44 Bowen Street. It has secured a 12-year term lease with Waka Kotahi NZ Transport Agency who will occupy 6 contiguous floors across the ground and levels 1 to 5, totaling 8,660 sqm of space. PCT committed to the 44 Bowen Street project on a pre-committed basis with leasing to KPMG secured at the end of last year. With Waka Kotahi NZ Transport Agency secured, the building will now be 100% leased.

In the release dated 21st May 2021, PCT announced that, after the successful bookbuild process for the offer of six-year secured, fixed rate green bonds, the offer has been closed as well as NZ$150,000,000 of Green Bonds (which includes the oversubscriptions amounting to $50,000,000) have been allocated to the participants (or their clients) in the bookbuild process.

Outlook:

Despite prevailing economic uncertainty, the company has delivered a solid result. For the interim period 1HFY21 ending December 2020, the occupancy levels remained strong at 98% (June 2020: 98%) with a weighted average lease term (WALT) of 7.7 years (June 2020: 8.0 years). Moreover, the balance sheet position stayed robust with a gearing of 29.9% (June 2020: 28.8%), which is expected to reduce further to around 26% following the sale of ANZ Centre as the company has entered into an agreement to divest the balance stake of 50% in ANZ Centre for a consideration of $177 million. The company sources its revenue from government and high-quality occupiers which ensures sustained growth.

In the meanwhile, the company continues to witness strong demand for high-quality, city centre office space with amenities on the back of increased business activities and expectations that the stance on the interest rate will remain accommodative in the near future.

Key Risks:

The company is susceptible to certain risks such as market risk which arises from adverse changes in the New Zealand economic environment, regulatory environment and the broader investment market. The risk of being unable to continue to obtain insurance cover, or following an event, not having sufficient cover in place to repay creditors. This could result in significant business interruption. Climate risk includes physical risks (acute and chronic) and transitional risks. Interest rate risk arises through changes in interest rate market conditions leading to earnings volatility or breach of interest cover covenant levels.

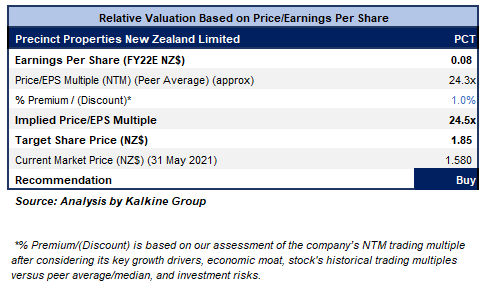

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

After a sharp sell-off in the previous week, the stock has given a stronger close at $1.58 on the first trading session of the ongoing week, forming a ‘Bullish Harami’ pattern implying bullish trend reversal from the existing bearish trend. The technical indicator RSI with a reading around 42 and a curve at the end pointing up suggests neutral to up momentum for the stock.

Going forward, the stock may have resistance around the converging point of 38.2% retracement level and 20 periods SMA of $1.64 whereas support could be around $1.54.

Stock Recommendation:

The company’s performance in the first half was strong with the portfolio continuing to show its resilience and performance in these uncertain times. While market conditions are expected to remain challenging in 2021, PCT expects to see demand for high quality, city-centre office space with surrounding amenities. With a further 11,300 sqm of leasing transactions completed in the period, the portfolio continues to attract businesses who want to occupy premium assets and be in highly attractive locations.

We have applied P/E based relative valuation (on an illustrative basis) and the target price so arrived reflects a rise of low double-digit (in % terms). We have applied a slight premium to Price/EPS Multiple (NTM) (Peer Average) considering its bottom-line performance and decent outlook.

Considering the portfolio strength along with high occupancy levels, solid development pipeline and completion of developments and sale of non-core assets, we give a “Buy” recommendation on the stock at the current market price of $1.580 per share, up by 1.94% on 31st May 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...