Company Overview: Port of Tauranga Limited (NZX: POT) is a New Zealand-based company, which operates a port and natural freight gateway to and from international markets for various New Zealand's businesses. It operates through three segments: Port Operations, Property Services and Marshalling Services. The Port Operations segment's operations consist of providing and managing port services, and cargo handling facilities through the Port of Tauranga and MetroPort. The Property Services segment consists of managing and maintaining the port's property assets. The Marshalling Services segment consists of the contracted terminal operations, stevedoring, marshalling and scaling activities of Quality Marshalling (Mount Maunganui) Limited, a subsidiary of the company.

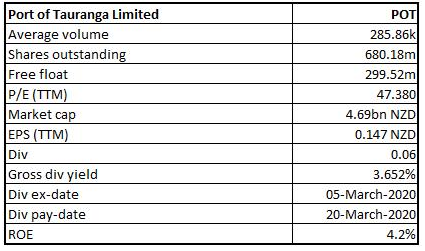

POT Details

Investment Summary:

Port of Tauranga Continues to Operate Essential Cargoes: Port of Tauranga Limited (NZX: POT) is New Zealand’s largest port and international freight gateway. The location of the port is central to key export commodity sources. The market capitalisation of the company stood at around $4.68 billion as on April 20, 2020. The company registered total revenue and net income growth at CAGR (compounded annual growth rate) of 8.47% and 9.18%, respectively, over FY16 to FY19. Group’s total revenue improved from $245.5 Mn in FY16 to $313.3 Mn in FY19, and net income improved from $77.3 Mn in FY16 to $100.6 Mn in FY19. The company announced stable profitability for the first six months of the financial year 2020, despite decrease in total cargo volumes by 4.2% to just under 13.3 million tonnes. Developments such as extending strategic alliances with Kotahi and plan to form a 50:50 JVs with Tainui Group Holdings, will drive expansion plan which, in turn, is expected to add revenue growth.

The current pandemic has sent strong ripples across different sectors, and the lockdown has added salt on the wounds of the companies especially those whose operations are global in nature. Port operation also involves shipping of cargos of essential goods and commodities such as meat, dairy products, fruits, oil products, food and medical supplies and therefore, port will continue to attract cargo volumes. As the pandemic subsides, a huge uplift in trade activities can be expected.

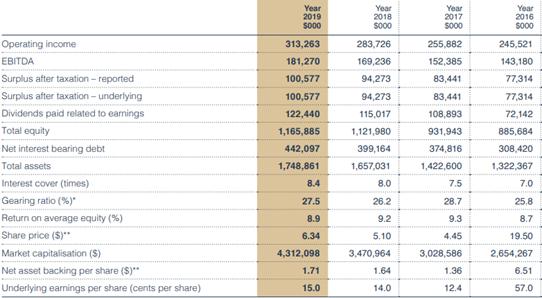

POT’s Historical Performance (Source: Company Reports)

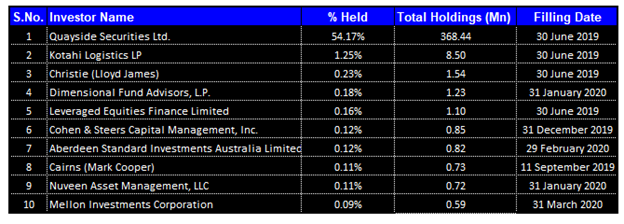

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in POT:

Top 10 Shareholders (Source: Thomson Reuters)

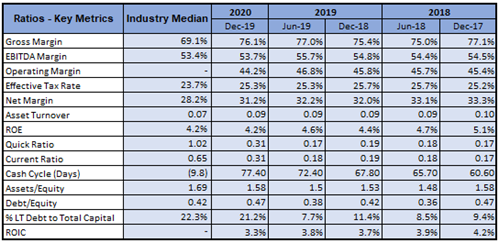

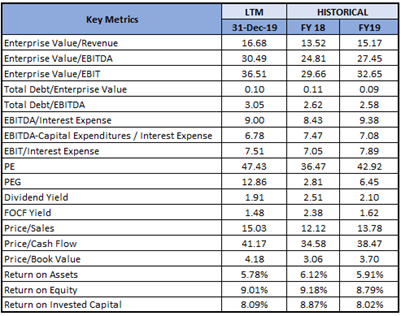

Quick Look at Key Metrics: Its gross margin, EBITDA margin and net margin for H1FY20 stood at 76.1%, 53.7% and 31.2%, better than the industry median of 69.1%, 53.4% and 28.2%, implying ability of the company to rationalize its operating costs. ROE for H1FY20 stood at 4.2% which came in-line with the industry median, implying that the company generated satisfactory returns for its shareholders. The company’s percentage of long-term debt to total capital stood at 21.2% as compared to industry median figure of 22.3%.

Key Metrics (Source: Thomson Reuters)

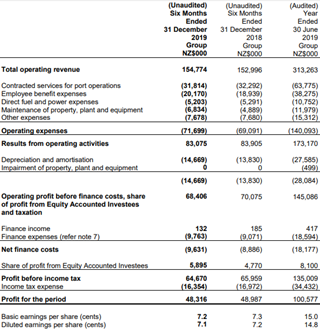

Topline for First Half FY20 Improved by 1.2%: The group’s net profit after tax for the first half of FY20 (ended December 31, 2019) was reported at $48.3 million, a decline of 1.4% on the previous corresponding period (pcp). The NPAT, after the adjustment for the impact of adopting new accounting standard NZ IFRS 16 for leases, reported a further decline of $0.587 million. On the positive side, container numbers improved by 3.4% (on pcp) to 642,209 TEUs; and transshipment, where cargo is transferred from one ship to another at Tauranga, improved by 3.7%. Total trade for the period was down by 4.2%, however, there was an increase in revenue by 1.2% to $154.8 million.

The company has taken the delivery of ninth container crane and would be extending the container terminal wharves by up to 220 metres by converting cargo storage land to the south of existing berths. Future stages of expansion are expected to be driven by cargo volume growth and may primarily involve rail-mounted electric stacking cranes and additional ship-to-shore cranes. POT and Tainui Group Holdings agreed to form a 50:50 joint venture to develop the Ruakura Inland Port at Hamilton over the next few years. This JV would take 50 year ground lease and aims to open inland port to coincide with completion of the nearby Hamilton section of Waikato Expressway, currently scheduled for 2021 end.

H1FY20 Income Statement (Source: Company Reports)

Key Risks: The company is susceptible to certain risks such as global economic slowdown, trade barriers as a result of inward-looking policies, fluctuations in the foreign exchange rate, commodity prices, and interest rate etc.

Overview of Recent Updates: The company’s Director David Alan Pilkington acquired 15,000 shares at value $89,250. On March 26, 2020, POT withdrew its earnings guidance for the year to 30th June 2020 due to the impact of government measures against the Covid-19 pandemic. The company earlier gave full year profit guidance in the range of $96 million - $101 million to $94 million - $99 million and had committed to provide update to the market on a regular basis.

The company’s operations have been classified as an essential service, allowing it to operate under the Covid-19 Level 4 restrictions imposed. Some of its customers, on being classified as non-essential services, suspended shipping during the lockdown. However, the Board members have expressed confidence that the company remains in a strong position to withstand the impact of the pandemic.

Recently, NZ’s largest containerised freight exporter, Kotahi and NZ’s international cargo gateway, POT, announced an extension to their long-term volume commitment agreement. The renewed agreement extends Kotahi’s commitment to Port of Tauranga for an additional seven years, till mid-2031. This marks a significant development for POT because Kotahi manages freight on behalf of more than 40 of New Zealand’s importers and exporters, including its shareholders Fonterra and Silver Fern Farms.

What to Expect from POT Moving Forward: As per the report, the company highlighted that the full impact on trade from the coronavirus outbreak is yet to be determined. Log exports were hardest hit, as volumes were already impacted by lower international prices and demand since the middle of 2019. Log inventories in China surged due to the extended Chinese New Year shutdown. However, POT is well positioned to weather the market fluctuations, as its customers are primarily large forest owners, who are less susceptible to commodity pricing volatility than smaller, at-wharf-gate log exporters. Further, there are signs that, in China, businesses are returning to normal which is likely to drive food, medical supplies and other cargos.

Key Valuation Metrics (Source: Thomson Reuters)

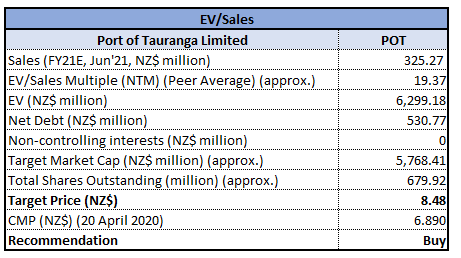

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

EV/Sales Multiple Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Analysis:

Weekly Chart:

Source: Thomson Reuters

Note: Purple colour lines are Bollinger Bands, yellow lines are retracement lines and orange colour dotted line is Parabolic SAR.

The stock was broadly in uptrend and while maintaining the underlying uptrend, it made the high of $8.09. From the recent high, the stock was caught under bearish trap which drove the price to the low of $4.91. From the low, the stock gave big rebound in its prices covering all key retracement levels of two extreme prices. On this date of just started week, the stock has traded virtually flattish and has closed on low of this date at $6.89, taking support at 61.8% retracement level.

Technical indicators such as MACD hovering around signal line while trending up and RSI with 52 reading and curve at the end, pointing up suggest strength in bullish momentum.

Going ahead, we believe that the stock will continue to be on lately assumed bull path and it could meet with resistance around recent high of $8.09. On the downside, 50% retracement level of $6.5 which also happens to be the previous week low, should provide strong support.

Stock Recommendation: The company has a robust balance sheet with strong operating cashflows from its diversified business. Many of its major exports, including meat, dairy products and kiwifruit, have been classified as essential cargoes. Imports of oil products, food and medical supplies have also been deemed as essential cargoes.

Moreover, in order to strengthen its balance sheet, the company has secured an increase to, and extension of its debt facilities that were maturing in January 2021. The extension of the strategic alliance between Kotahi and POT is expected to help both the entities moving forward.

Considering the aforesaid facts, recent updates, H1FY20 results, profitability margins and outlook, we have valued the stock using EV/Sales multiple based method (on an illustrative basis) and we have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$6.890 per share, down by 1.01% on April 20, 2020.

.png)

POT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...