Company Overview: A technology company, Over the Wire Holdings Limited (ASX: OTW) offers telecommunications, cloud and IT solutions to customers throughout Australia and New Zealand. Its services include Data Networks and Internet, Voice, Data Centre co-location, Cloud and Managed Services. The company seeks to accelerate growth through strategic acquisitions and strengthening geographical footprint. It offers a simplified and reliable platform to customers, through continuous engagement in building new capabilities.

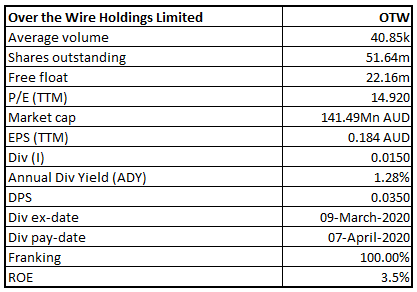

OTW Details

.png)

OTW Rides on Synergies from Acquisitions & Higher Customer Retention Rate: Over the Wire Holdings Limited (ASX: OTW) is engaged in offering telecommunications, cloud and IT solutions in all major Australian capital cities, including Auckland, New Zealand. The company provides an integrated suite of products and services to enhance the customers’ experience. During FY19, the company remained on track to deliver remarkable organic growth while pursuing its expansion plans through acquisitions. In FY19, the company reported total revenue from ordinary activities of $79.59 million, an increase of 49% year over year. The result mainly indicated higher demand from customers across all four product lines. OTW reported organic revenue growth of 15%, with all the regions demonstrating positive results. Geographically, revenues from Queensland, New South Wales, South Australia and Victoria boosted 17%, 14%, 13% and 11%, respectively. On a statutory basis, South Australia witnessed the highest growth of ~ 230%, mainly due to expansion into the market through the Access Digital Networks buyout in November 2018.

Since 2015, the company remains on track to carry out a number of acquisitions, with timely realisation of synergies and cost savings via integration. On 1 November 2018, the company acquired 100% of the shares in Access Digital and Comlinx. These acquisitions aid OTW with cross-selling opportunities. In FY19, the company’s Data Networks revenue soared ~26% year over year. The company also witnessed demand from customers across all product lines, with Cloud and Managed Services reporting the highest increase in revenue, up 217% year over year. The increase was aided by synergies of acquisitions and organic growth. EBITDA for the year increased a whopping 64% and stood at $20.06 million, whereas NPAT increased by 83%, driven by cost management initiatives and a higher revenue base. Coming to the half-year results for the period ended 31st December 2019, OTW reported around 25% increase in its statutory revenue, as a result of continued demand from customers across all product lines.

The company has a track record of consistent growth in revenue, profitability and shareholder returns. It reported a CAGR of 49% and 54.5% in revenue and EBITDA, respectively, over FY15-FY19. OTW’s efforts to provide better experiences to customers have led to high levels of customer service and retention.

.png)

.png)

Past Track Record of Revenue, EBITDA & Customer Retention (Source: Company Reports)

The company remains on track to achieve its long-term growth through the acquisition of new customers and increased sales to existing customers. With an extremely devoted team offering, the company is confident about achieving another strong year in FY20. The company is also focusing to complete several new capabilities in the coming six months. These new facilities involve unveiling a Microsoft Teams Direct Routing service and adding mobile services on post-paid basis to OTW’s product portfolio. Matched by acquisition synergies, the company touts to remain committed delivering on its strategy and leverage on strong opportunities for future growth.

1HFY20 Key Highlights for the Period Ended 31st December 2019: In 1HFY20, the company reported total statutory revenue of $42.9 million, increasing 25% from the prior corresponding period of restated revenue of $34.3 million, after including the impact of AASB16. Product-wise, revenue from Data Networks increased 8% year over year and came in at $19.1 million. Revenues from Security & Services stood at $9.5 million, up a whopping 118% year over year. Revenues from Vice and Hosting increased by 14% and 21%, respectively, on a year over year basis. Recurring revenue for the period grew 5% year over year and stood at $36.6 million, up 5% on prior corresponding period. EBITDA from recurring revenues increased 19%, while EBITDA margins went up by 2% year over year. However, the negative impact of NBN downward repricing on Data Revenue continues, which led to a decrease of 1% from Data Network sales. The non-recurring business went down 39% year over year, owing to a significant drop in one-off revenue. The company reported EBITDA of $8.2 million, up 1% year over. NPATA for the period came in at $4.2 million, representing a decline of 2% year over year. NPAT went down by 27% and came in at $2.3 million. The company declared an interim dividend of 1.5 cents, payable on 7 April 2020.

.png)

P&L Statement (Source: Company Reports)

.png)

Segmental Details (Source: Company Reports)

Key Growth Strategies: In 1HFY20, OTW made significant investments to drive growth in the recurring business. Over the period, the company doubled the number of sales roles, with the goal of winning new business and customers. The company also commenced offshoring of non-customer facing operational roles. The company also expanded its development team during the period, owing to higher operational efficiencies from the development initiatives. Although, these investments added an additional $1 million in expenses during 1HFY20, the company increased monthly recurring revenue growth of 25% in a span of 18 months’ time.

Balance Sheet $ Cash Flow Details: The company exited the period with cash and cash equivalents amounting to $7.4 million and net assets amounting to $66.8 million. The business remained debt-free as at 31st December 2019 and is well-positioned for the next few acquisitions through debt, without exceeding a net-debt to EBITDA ratio of 1.5x. On the heels of continuous investment in business development, OTW has built a strong sales pipeline for monthly recurring revenue, which increased by 39% in 1HFY20 and 58% in CY19. Net cash provided from operating activities in 1HFY20 stood at $4.2 million, whereas net cash used in investing activities and financing activities stood at $3.3 million and $3.8 million, respectively.

.png)

Cash Flow Statement (Source: Company Reports)

Recent Update: The company released an announcement notifying that CFO and Company Secretary Mike Stabb has shifted into a new team to focus on mergers & acquisitions, new product enhancement and new market opportunities. Simone Dejun will take over the role of Company Secretary, effective from 1 April 2020. The organisational changes were done keeping in mind the continuity of the business and to provide high-quality customer experience and expand at a strong organic rate.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 71.27% of the total shareholding. Omeros (Michael Nictarios) held the maximum number of shares with a percentage holding of 25.22%, followed by Paddon (Brent Evans) holding 22.28% of the shares.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

Key Metrics: For the half year ended 31st December 2019, the company reported a gross margin of 83.2%, which is higher than the industry median of 74.8%. Debt to Equity multiple stood at 0.16x, as compared to a multiple of 0.26x in the prior corresponding half and the industry median of 0.49x. The company improved on its short-term liquidity with a current ratio of 1.02x in 1HFY20, as compared to a current ratio of 0.75x in the prior corresponding half.

.png)

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company is eyeing continued organic growth through a strong sales pipeline. A debt-free balance sheet will aid the company to attain its long-term objectives of expanding the business through acquisitions and delivering continued growth in shareholders’ returns. As the business holds the ability to carry out additional acquisitions, it is seeking to discover the next set of quality businesses that can perform as drivers for future growth. Additionally, the company’s effort to provide complete telecommunications, cloud and IT Services offering to businesses, through the help of a dedicated support team, gives OTW confidence to predict future growth beyond FY20.

The COVID-19 outbreak is changing the way people perform their day-to-day lives and how they communicate with friends and family. A change in working habits has also been noticed. Cloud computing is playing a huge role, in aiding organizations distantly process a lot of information, and run crucial applications and services. It is also helping employees work together from anywhere across the globe. Given the major role that cloud computing is playing during this virus-driven crisis, OTW stands to benefit as the work from home trend continues.

In 1HFY20, the company reported a rise of 24% in new monthly recurring revenue won, as compared to 1HFY19. Sales pipeline for monthly recurring revenue has increased by 58% on the calendar year 2019. The impetus is expected to persist in the coming years. Another area of focus has been the expansion of the product portfolio, with new products set to be launched in the second half of FY20.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

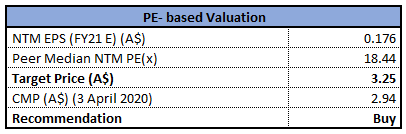

Valuation Methodology 1: Price to Earnings Multiple Based Relative Valuation

Price/Earnings Based Relative Valuation (Source: Thomson Reuters)

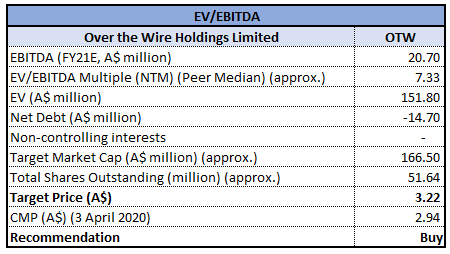

Valuation Methodology 2:EV/EBITDA Multiple Based Relative Valuation

EV/EBITDA Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company corrected by 39.91% in the past three months and is currently trading close to its 52-week low level of $1.830. The company has a market capitalisation of $141.49 million, with a P/E ratio of 14.92x (on TTM basis) and annual dividend yield of 1.28%. In 1HFY20, the company witnessed customer demand across all its product lines and continued to make relevant investments for development on the platform. Additionally, the company is also focusing on new business opportunities that can complement its current offerings and deliver enhanced customer experience. We have valued the stock using two relative valuation methods, i.e., Price to Earnings and EV/EBITDA multiples. For the said purpose, we have considered peers like TechnologyOne Ltd (ASX: TNE), Citadel Group Ltd (ASX: CGL), Data#3 Ltd (ASX: DTL) to name a few. As a result, we have arrived at a target price with an upside of higher single-digit to lower double-digit (in percentage terms). Considering the above factors, we give a “Buy” recommendation on the stock at the current market price of $2.94, up 7.299% on 3 April 2020.

OTW Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...