Company Overview: Specialist outdoor retailer, Kathmandu Holdings Limited (NZX: KMD) is engaged in designing, marketing and retailing of clothing and equipment for travel and adventure. The company's segments include New Zealand, Australia and the United Kingdom. It offers a range of apparels, including waterproof jackets, down jackets, thermals, fleece jackets, shirts and pants, merino apparel and thermals, and footwear and socks. It also offers equipment including packs, bags, sleeping bags, tents, travel accessories and camping accessories. The company operates approximately 110 stores in Australia, over 46 stores in New Zealand and approximately four in the United Kingdom. The company's subsidiaries include Milford Group Holdings Limited, Kathmandu Limited, Kathmandu Pty Limited and Kathmandu (U.K.) Limited.

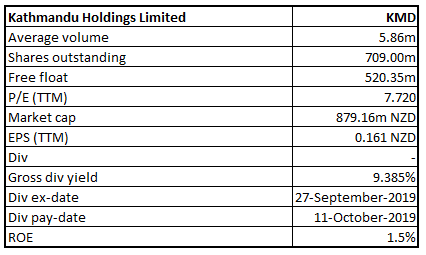

KMD Details

Investment Summary:

Retail Stores Fully Operational in NZ and AUS Region: Kathmandu Holdings Limited (NZX: KMD) is a marketer, designer, wholesaler and retailer of footwear, clothing, and equipment for travel and adventure. The company operates in New Zealand, the United Kingdom, the United States of America and Australia.

Looking at the past performance over FY15 to FY19, top line and the bottom line of the company witnessed a compounded annual growth rate (CAGR) of ~7.44% and ~29.63%, respectively. The company’s total revenue improved from $409.4 million in FY15 to $545.6 million in FY19, and its net income improved from $20.4 million in FY15 to $57.6 million in FY19.

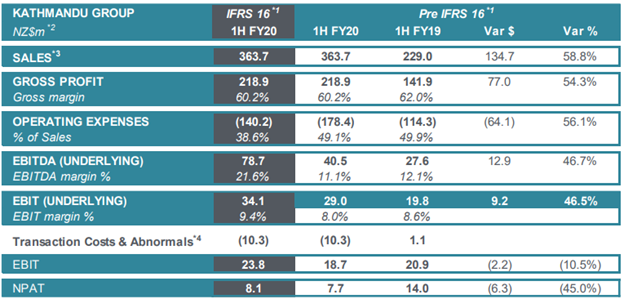

Group total sales for the first half period of FY20 (ended January 31, 2020) increased by 58.8% to $363.7 million, as compared to the previous corresponding period (pcp). Group Underlying EBIT increased by 46.5% (excluding the impact of IFRS 16, and one-off transaction and abnormal costs) to $29.0 million. Statutory NPAT of $8.1 million includes $10.3 million of one-off transaction costs and abnormal costs and $0.4 million from the implementation of the IFRS 16 leasing standard.

Outdoor segment (Kathmandu and Oboz) total sales increased by 0.4% at the constant exchange rates. Kathmandu same-store sales grew by 1.5%, whereas online comparable sales grew by 33.1%. Oboz total sales increased by 10.4% at the constant exchange rate. Surf segment (Rip Curl) total sales increased by 3.7% wherein same-store sales grew by 2.7% while on-line comparable sales grew by 19.5%.

The half period witnessed important developments such as successful completion of the Rip Curl acquisition, creating a more diversified group of three iconic brands across key global markets.

H1FY20 Key Metrics (Source: Company Reports)

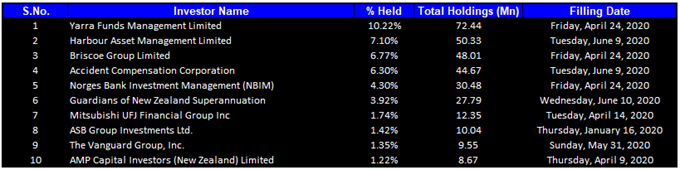

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 44.33% of the total shareholding. Yarra Funds Management Limited and Harbour Asset Management Limited hold maximum interests in the company at 10.22% and 7.10%, respectively.

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

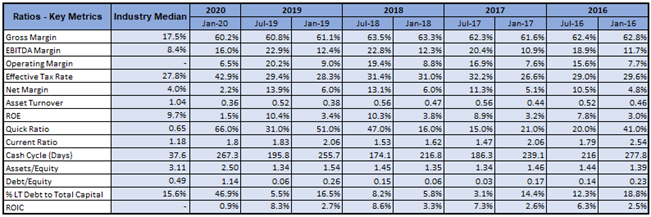

A Quick Look at Key Metrics: Its gross margin and EBITDA margin for H1FY20 stood at ~60.2% and ~16.0%, better than the industry median of ~17.5% and ~8.4%, respectively, implying the company’s ability to rationalize expenditures. Current ratio for H1FY20 stood at ~1.80x, better than the industry median of ~1.18x, implying that the company possesses better capabilities to meet its short-term obligations than its peer group.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Equity Raising Might Provide Support: The group, on April 1, 2020, announced that it successfully completed a fully underwritten NZ$207 million equity raising to strengthen its balance sheet and to ensure that the company remain strongly capitalized through uncertain market conditions caused by Covid-19. The proceeds will be used to deleverage the balance sheet and provide liquidity. In addition to the equity raising, the group continues to implement a series of actions to reduce costs and further strengthen its financial position, such as:

A Look at Recent Updates: The company recently highlighted that, in the month of April, Kathmandu and Rip Curl continued to trade online in all international jurisdictions, with Kathmandu New Zealand selling only essential items online from 3 April 2020. During April, group online sales were 2.5 to 3 times higher than last year, with the highest growth rates in Australia, the group’s largest market. Online sales growth strengthened over April as consumers adapted to online being their only available shopping channel.

What to Expect: As stores begin to reopen in Australia, the full impact of COVID-19 on the group, including its wholesale channel and partners along with the level of consumer demand, would be challenging to forecast before returning to more normal trading conditions in many international jurisdictions in which the group operates.

Key Risks: The company is exposed to a variety of financial risks such as interest rate risk, currency risk, credit risk, and liquidity risk. The company uses derivative instruments such as foreign exchange derivative and interest rate derivative to mitigate these risks.

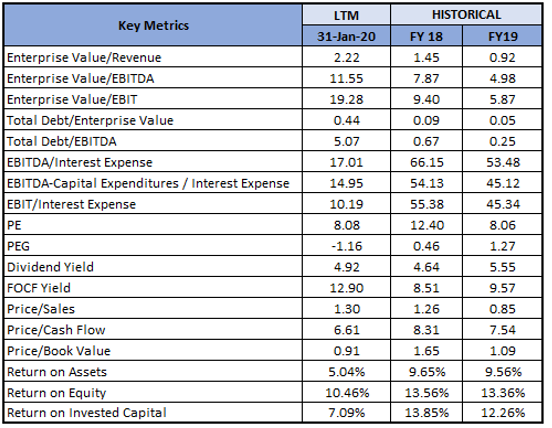

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

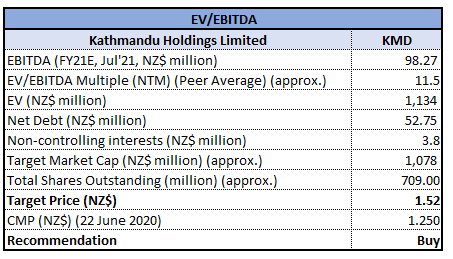

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart -

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

Having experienced sharper fall from its recent high of $2.55, the stock made a low of $0.49. From the low, the stock has retraced up to 50% retracement level of $1.51 but slipped from there to 23.6% retracement level of $0.96. In the previous week, the stock moved up to 38.2% retracement level of $1.26 and gave close around $1.24. On this date of June 22, 2020, the stock has given close around the same price of the previous week thereby exhibiting that bullish trend for the stock remaining intact. Technical indicator RSI with around 47 reading and curve at the end pointing up, suggests bullish momentum for the stock.

Going forward, the stock may have resistance around $1.51 while support could be around $0.96.

Note: Technical analysis as at 3:30 pm, June 22, 2020, Auckland, New Zealand.

Stock Recommendation: The first half financial result shows that the company was in a strong position to deliver next wave of growth on the back of its three global brands, namely Kathmandu, Rip Curl and Oboz. It was the occurrence of COVID-19 that derailed the whole growth process. However, staged re-opening of physical stores following lowering alert levels would attract customers back in stores. In the medium term, consumer demand is expected to be subdued but, with trading returning to more normal conditions in different parts of the world where the company operates in, there could be a rise in opportunities.

The company’s digital infrastructure and supply chain investments made over the last three years have underpinned its ability to rapidly ramp up online trading capabilities and distribution capacity in the face of unprecedented online demand. Moreover, KMD’s successful equity raising strengthens its balance sheet and liquidity position, ensuring it remains well-capitalised to navigate through the current trading uncertainties caused by COVID-19.

Considering the aforesaid facts, we have valued the stock using EV/EBITDA Multiple Based Relative Valuation (on an illustrative basis), and we have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$1.250 per share (New Zealand time: 1:50 pm) on June 22, 2020.

.png)

KMD Daily Technical Chart (Source: Refinitiv (Thomson Reuters)) (New Zealand Time: 1:50 pm)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...