Company Overview: Oceania Healthcare Limited operates in the New Zealand residential aged care and retirement village sectors. The Company offers residents villas and apartments within its retirement villages. The Company also provides a range of residential aged care services (including rest home, hospital and dementia level care) at its aged care facilities.

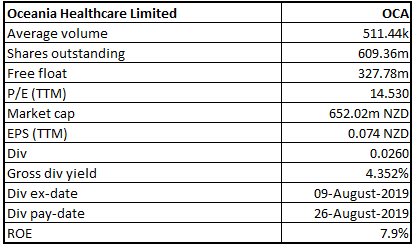

OCA Details

Strong Sales from Key Development Sites: Oceania Healthcare Limited (NZX: OCA) owns and operates various care centres and retirement villages throughout New Zealand. FY19 proved to be a period of strong sales rate and pricing at the recently completed development sites. Operating revenue for the period amounted to $5.4 million, backed by increased aged care occupancy, increased income from retirement village operations and higher income from premium rooms. Operating cash flow for the period stood at $89.3 million, representing an increase of 8.6% on prior corresponding period. The period was marked by significant development capital expenditure, greenfield acquisitions and revaluations, increasing the total assets by 22% on prior corresponding period. Overall, the company successfully executed its strategy of developing its brownfield sites in major cities and upgrading the other aged care sites throughout New Zealand during the year. Although, underlying net profit after tax was consistent in comparison to the prior year, the result was primarily affected by the timing for completion of two key development sites, including Meadowbank Stage Four and The Sands. The period saw strong sales from both the sites.

Over the coming year, the company expects its key development sites to deliver strong sales. Going forward, the company is looking to execute on its strategy to transform its product portfolio and focus on delivering services beyond the residents’ expectations.

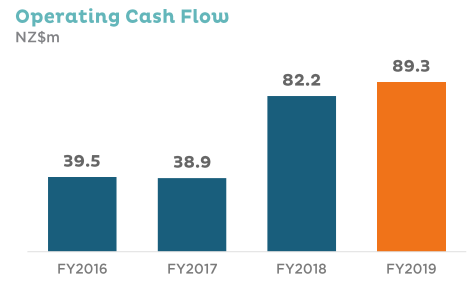

Over a period of 4 years covering FY16 to FY19, the company reported an operating cash flow CAGR of 31.2%, with FY16 and FY19 cash flow amounting to $39.5 million and $89.30 million, respectively. Growth in FY19 was primarily due to a contribution worth $75.5 million from sale proceeds out of previously completed developments. With an increase of 8.6% in operating cash flow, the company continued to maintain enough headroom and flexibility to accelerate the execution of its development pipeline.

Operating Cash Flow (Source: Company Reports)

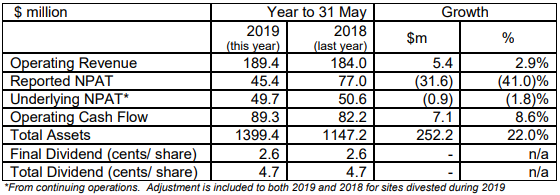

FY19 Results Highlights: During the year ended 31 May 2019, the company reported operating revenue amounting to $189.4 million, representing an increase of 2.9% on prior corresponding period operating revenue of $184.0 million. Reported NPAT for the period came in at $45.4 million, down 41% on prior year’s NPAT of $77.0 million, primarily due to existing village valuations remaining stable. Underlying NPAT came in at $49.7 million, down 1.8% on the previous year. While the profit was positively impacted by improved development margins, increased costs to improve care earnings in future years and interest costs to fund development activity overshadowed the benefits. The company declared a final dividend of 2.6 cents per share, maintaining full year dividends in line with the previous year at 4.7 cents per share. Corporate overheads for the year increased by 17%, due to additional staffing requirement to commencement of operations at four new care centres at The Bayview, The Sands, Meadowbank Stage 4 and Awatere.

FY19 Financial Summary (Source: Company Reports)

Balance Sheet: Total assets for the year came in at $1.4 billion, representing an increase of 22% over prior corresponding year, reflecting the completed aged care and retirement village developments as well as new land acquired adjacent to existing sites at a number of Auckland locations during the year. Net debt for the period stood at $248.2 million, with a prudent gearing of 28.9%. On 6 July 2018, the company entered into an agreement with a bank syndicate to increase total debt facility limits from $235 million to $350 million. General corporate facility limit and development facility limit have been increased to $135 million and $215 million, as compared to the previous limits of $75 million and $160 million, respectively.

Key Updates:

Oceania Healthcare Receives Major Resource Consent: The company recently announced that it has received a significant resource consent from Auckland Council for the redevelopment of its Elmwood Village in The Gardens, Manurewa. Prior to this, the company already had resource consent to construct a new 142 room aged care centre on the land adjacent to the site. After the recent announcement regarding the new consent, the company will now be able to construct five new buildings, comprising 229 new independent living apartments and a new community centre, as a part of redevelopment. After receival of the consent, the proportion of the company’s development pipeline, including units and beds currently under construction, increased to 83.6%.

Appointment of GM Nursing & Clinical Strategy: As per another recent announcement, the company notified about the appointment of Frances Hughes as the General Manager, Nursing & Clinical Strategy. He holds an extensive experience of over 30 years in nursing and has held senior management and nursing positions on a global level.

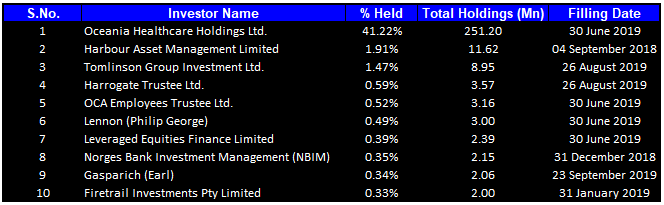

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 47.61% of the total shareholding. Maximum number of shares were held by Oceania Healthcare Holdings Ltd. with a percentage holding of 41.22%, followed by Harbour Asset Management Limited with a holding of 1.91%.

Top Ten Shareholders (Source: Thomson Reuters)

Top Ten Shareholders (Source: Thomson Reuters)

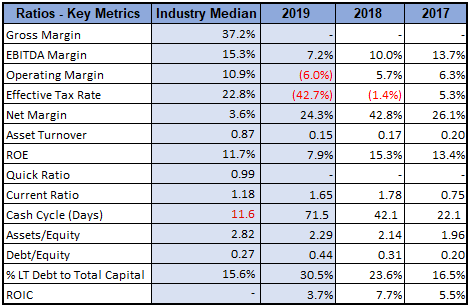

Key Metrics: During the year ended 31 May 2019, the company reported an EBITDA margin of 7.2%. Net margin for the period stood at 24.3%, which is higher than the industry median of 3.6%. Current ratio for the period stood at 1.65x, which was again better than the industry median of 1.18x, representing a better position to address short-term business liabilities as compared to the peer group. Debt-to-Equity ratio for the period was also decent at 0.44x, but slightly above prior corresponding year’s ratio of 0.31x.

Key Metrics (Source: Thomson Reuters)

Update on Aged Care Offering: During the year, aged care occupancy increased to 92.8%, against previous year’s occupancy rate of 90.8%. The increase came in primarily due to investment made in refurbishing the company’s existing portfolio and converting older, standard aged care rooms into its premium care suite product, which is sold under occupation right agreement. The aged care offering generated earnings worth $2.7 million, which was lower than the previous year due to unavailability of rooms during the redevelopment and refurbishment process, start-up costs incurred in opening new aged care sites and the impact of sector-wide wage cost increases. However, the company is now into the process of decommissioning older sites and replacing them with its new, premium offering, to generate fruitful results in the future.

Strong Sales: FY19 was characterised by strong sales across both new sites including, Meadowbank Stage Four and The Sands. By the end of three months since completion of The Sands, the company reported the sale of 27 retirement village apartments and 7 care suites. At Meadowbank, the company reported sales of 16 retirement village apartments and 9 care suites. At The BayView in Tauranga, the company reported the sale of 18 care suites, reflecting all of the rooms available after transfer of residents from the older care centre late last year.

In FY19, three key development projects of the company completed on time. Moreover, the company is on track for completion of its development programme for delivery of 265 beds and units.

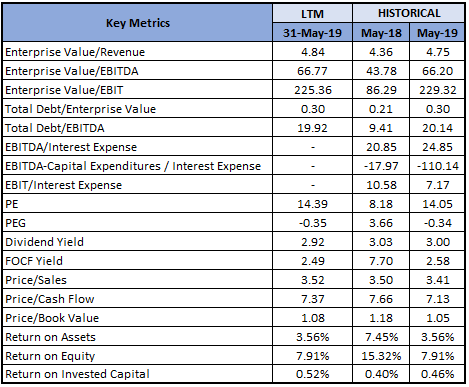

Key Valuation Metrics (Source: Thomson Reuters)

What to Expect: The company is continuously improving on its core competency, i.e., the aged care offering and seems well down the track to execute the strategy for transformation of its portfolio into a higher mix of premium aged care product through its new care suites and conversion of standard rooms to care suites around the country. At the end of FY19, 38% of the company’s portfolio comprised of premium beds and units, which is expected to increase to 50% by the end of the next financial year to May 2020. At Meadowbank, the construction of Stage Five comprising an additional 26 apartments is well underway, that will bring the total number of independent living apartments at the Village to 192. Development of Stage Five is expected to be completed in the second half of FY20. In addition, the company is progressing well on the development at Windemere in Papanui, Christchurch, another key brownfield development site with good demand for aged care. Completion of development at the site is expected in FY21.

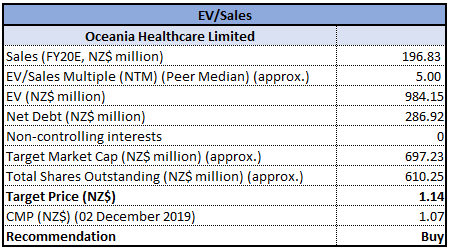

Valuation Methodology: EV/Sales Multiple Approach

EV/Sales Multiple Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company is currently trading close to the average of its 52-weeks trading range of 0.99x – 1.17x. In FY19, the company reported strong sales across its development sites, which is expected to continue in the next financial year. The period was also marked by an increase in operating cash flow, particularly from development proceeds in relation to Meadowbank Stage Three. Moreover, the company is continuously working on improving its core competency, i.e., aged care offering. Investment in construction capital expenditure amounted to $135.0 million, representing an increase of $56 million on previous year. The investment is driving growth in NTA through redevelopment of brownfields locations, as well as enhancing near term development margins and longer-term trail income streams through deferred management fees and aged care earnings. Considering the performance in FY19, particularly strong sales from key development sites; expected sales growth in the future; a significant development pipeline; and current trading levels, we have valued the stock using EV/sales multiple based relative valuation method and arrived at a target price of higher single-digit growth ( in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of $1.070, down 0.93% on 02 December 2019.

OCA Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...