Company Overview: Oceania Healthcare Limited (NZX: OCA) operates in the New Zealand residential aged care and retirement village sectors. The company at its aged care facilities, provides a full range of residential aged care services including rest homes, hospital, and dementia level care, and under retirement villages, it provides residents villas and apartments. OCA is presently NZ's 3rd largest provider of residential aged care, and 6th largest provider of retirement village business. The company is also an experienced brownfields developer of aged care as well as retirement village facilities across New Zealand.

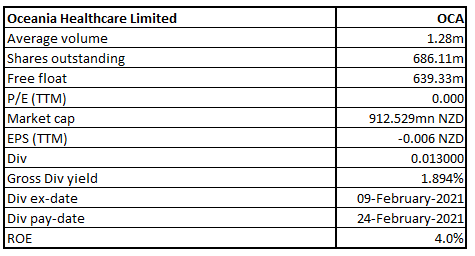

OCA Details

Oceania Healthcare Limited (NZX: OCA) provides Rest Home, Hospital, Dementia, Respite and Palliative/End of Life Care, as well as Independent Retirement Village living, at over 40 New Zealand locations. The company has a market capitalization of ~$912.529 million as on 12th April 2021.

Looking at the historical performance, OCA’s top-line for FY16-20 grew at a CAGR of 3.27%, wherein its total revenue improved from $170.2 million in FY16 to $193.6 million in FY20.

Results Performance (Half-Year ended 30th November 2020)

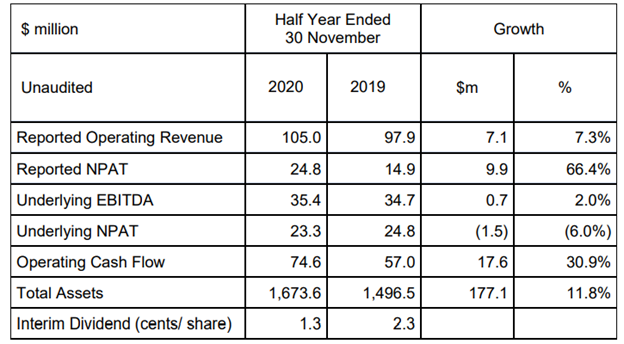

Driven by strong growth in sales volume across new sales and resales over the interim period, the company registered a 7% growth in its revenue to $105.030 million on the pcp. Sales volumes were 44.1% up on the pcp as many new residents have enjoyed the benefit of retirement village living in an uncertain year. The 20.6% increase in resale volumes is particularly pleasing as a key indicator of the quality of Oceania Healthcare’s annuity earnings streams.

Underlying EBITDA for the interim period grew by 2% to $35.410 million on the pcp. However, the underlying NPAT for the period decreased by 6% to $23.3 million compared to $24.8 million in the same period last year. As a result of strong sales volume, operating cash flow for the period increased by 30.9% to $74.6 million whereas significant development Capex resulted in total assets for the period rising by 11.8% to $1.7 billion.

The Board of Directors declared an interim dividend of 1.3 cents per share, with record a date of 10 February 2021 and a payment date of 24 February 2021.

Exhibit 1: Key Financial Numbers

Source: Company Reports

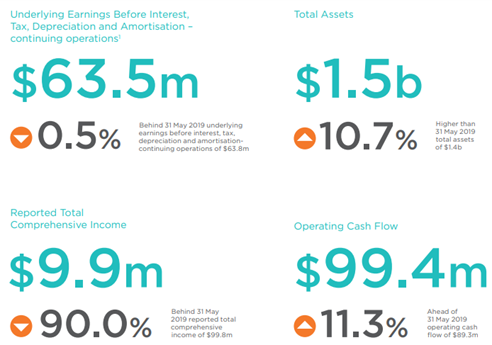

Results Performance (Year ended 31st May 2020)

The company for the full-year FY20 reported underlying EBITDA of $63.5 million which was in line with the pcp. This is despite the inability of the company to sell retirement village units throughout the final quarter of the FY20 because of the lockdown imposed by the Government. However, it reported NPAT for the period at -$13.6 million which includes an unrealized decrease of $21.7 million in the valuation of investment property.

A significant development over Capex and completion of new aged care centres led to an increase in total assets by 10.7% to $1.5 billion. Operating cash flow increased by 11.3% to $99.4 million as a result of sale proceeds from developments completed in the previous financial year.

Exhibit 2: Key Metrics

Source: Company Reports

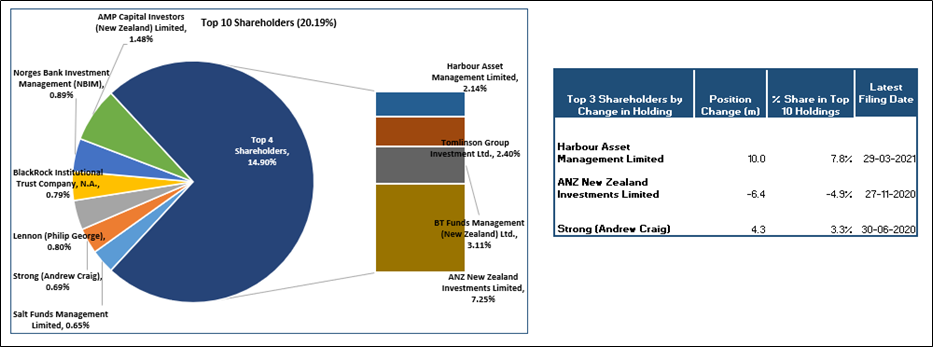

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 20.19% of the total shareholding. ANZ New Zealand Investments Limited and BT Funds Management (New Zealand) Ltd. are holding a maximum stake in the company at 7.25% and 3.11%, respectively, as is evident from the chart provided below:

Exhibit 3: Top 10 Shareholders

Data Source: Refinitiv, Thomson Reuters, Analysis by Kalkine Group

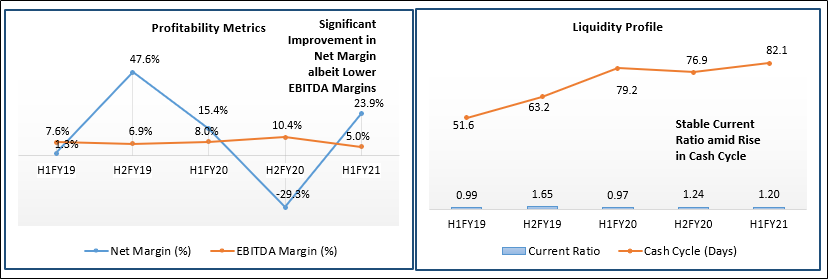

A Quick Look at Key Metrics: The company’s EBITDA margin for H1FY21 stood at 5% whereas net margin for H1FY21 stood at 23.9%, better than the industry median of 3.8%. The current ratio for H1FY21 stood at 1.20x, better than the H1FY20 result of 0.97x, implying a sound liquidity position for the company.

Exhibit 4: Key Financial Ratios

Data Source: Refinitiv, Thomson Reuters, Analysis by Kalkine Group

Outlook:

The company has experienced strong growth in new sales and resales over the interim period and has also been experiencing continued strong demand for its premium care suites across the country. The aged care segment of the company has exhibited incredible resilience which has positively contributed to underlying EBITDA and a corresponding increase in earnings per bed over the interim period. The company currently owns six brownfields’ projects which are underway. Its developments at Stage Two at The BayView, Tauranga (comprising 35 apartments) and Stage One at The Bellevue, Christchurch (comprising 71 care suites and 22 apartments) are all progressing well and are expected to be completed in 2021. Other brownfields projects at Lady Allum, Auckland (113 new care suites), Eden, Auckland (comprising 49 apartments and a new community centre), a further 39 apartments at The BayView, Tauranga, Stage Two at Awatere, Hamilton (63 apartments and a new community centre) and Stage Three at Gracelands, Hastings (18 villas) are also underway and are expected to be completed during FY22.

Industry Outlook:

Like most of the developed world, New Zealand has been confronting with the issue of ageing population. As per the estimates provided by Stats NZ, the number of people aged 65+ doubled between 1988 and 2016 and reached 700,000. This number is projected to double again by 2046.

It is estimated that there is a 90% chance that there will be 1.32–1.42 million people aged 65+ in 2043, and 1.62–2.06 million in 2068. By 2032, it is expected that 20–22% of New Zealanders will be aged 65+, compared with 15% in 2016. By 2050, this proportion is expected to reach 21–27% and 24–33% by 2068. Ageing increases the demand for primary healthcare and long-term care thereby creating business opportunities for the companies operating in aged care and retirement house business. OCA with its size and scale of operation, and credibility of great care facilities provider, is well-positioned to capitalize on the emerging opportunities in the sector.

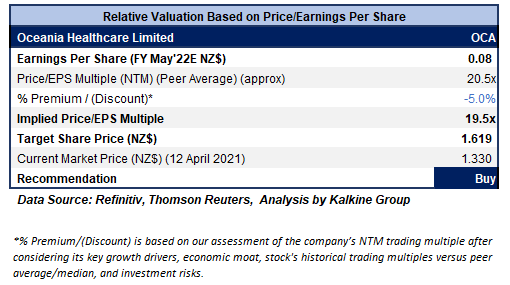

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

Key Risks: The company is exposed to risks related to COVID-19 as NZ government could announce restrictions so that the spread of the virus can be restricted. This could impact the sales of retirement village units. Also, old-age people are more exposed to this deadly virus which presents challenges for the companies operating in the aged care sector.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

While remaining in an underlying uptrend, the stock corrected close to 38.2% retracement level in the week before the previous week. However, in the previous week, it gave a strong close. Following the previous week of strong close, the stock has given a stronger opening and close in the first trading session of the ongoing week at $1.33. The technical indicator RSI with a reading around 48 and a curve at the end pointing up, suggests gaining of bullish momentum for the stock.

Going forward, the stock may have resistance around $1.50 whereas support could be around the converging point of the lower Bollinger band and the 38.2% retracement level of $1.24.

Stock Recommendation:

Despite the pandemic-related restrictions, OCA’s aged care segment has demonstrated incredible resilience this year. There was a record increase of 15.3% in underlying EBITDA from its Care segment and a corresponding increase in earnings per bed over the interim period. Aged care occupancy also increased to 92.1%, compared to 91.6% last year. Moreover, the company opened 61 new care suites at Green Gables in Nelson in September as it continued to successfully execute its aged care strategy through the redevelopment of its brownfield’s sites, and its care suite sales volumes have experienced a fivefold increase over the past three years.

OCA’s stock has given a return of ~37.5% and ~65.00% in the time of nine months and one year, respectively. The stock is currently trading above the average of 52-week high-low range.

Considering the aforesaid facts, we have valued the stock using P/E multiple-based valuation (on an illustrative basis) and have arrived at the target price with the potential of low double-digit growth (in % terms). We have applied a slight discount to Price/EPS Multiple (NTM) (Peer Average) considering the increase in total debt, lower ROE and re-emergence of restrictions related to COVID-19 which could impact the company’s overall operations.

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$1.330 per share, up by 0.76% on April 12, 2021.

OCA Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Note: Investment decision should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...