Company Overview: Oceania Healthcare Limited operates in the New Zealand residential aged care and retirement village sectors. The Company offers residents villas and apartments within its retirement villages. The Company also provides a range of residential aged care services (including rest home, hospital and dementia level care) at its aged care facilities.

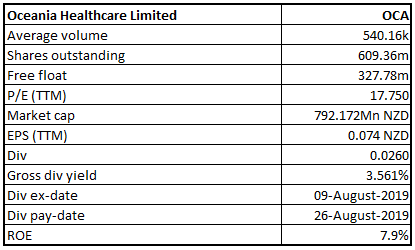

OCA Details

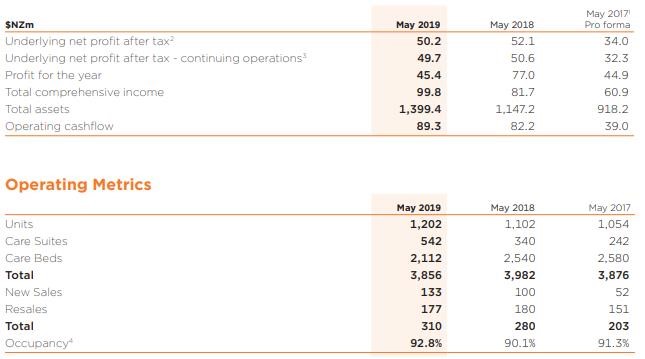

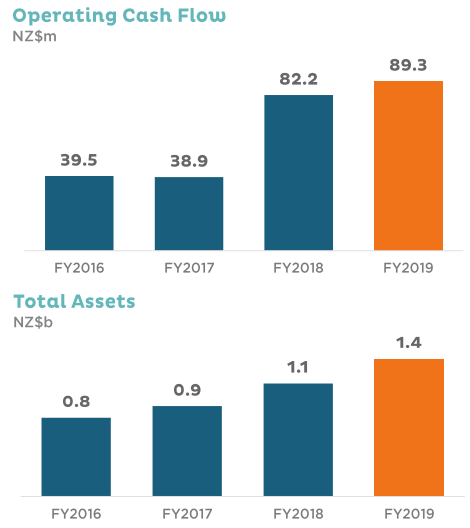

Enjoying Leading Position in the Industry: Oceania Healthcare Limited (NZX: OCA) is one of New Zealand’s largest operators and owners of retirement villages with over 40 locations including 25 villages. The Operating segments include – (a) Care, (b) Village, and (c) Other. The company provides hospital, restroom, respite and end of life care as well as independent retirement village living. The company has a total of 3,856 suites, units and beds located at 46 sites in the South and North Islands. The company has a market capitalisation of ~$792.172 million on 06th January 2020. The company has a decent platform for growth with a substantial development pipeline and proven expertise and experience in managing and delivering construction projects. Net income during FY15-FY19 witnessed a CAGR of 23.7% amounting to $45.4 million in FY19 from $19.4 million in FY15. Total assets also showed a decent performance reaching $1,399.4 million in FY19 from $918.2 million in FY17. Operating cash flow stood at $89.3 million in FY19 from $39 million in FY18, depicting working capital management of the company. The company continues to maintain enough headroom and flexibility to accelerate the execution of development pipeline. FY19 saw a yoy growth of 22.1% in total comprehensive income to $99.8 million. With net debt of $248.2 million in FY19, the gearing remains prudent with net debt to net debt plus equity of 28.9%.

The company has proved its development capability with the completion of The Sands and Meadowbank Stage Four on programme last year, and the completion of Awatere Village ahead of programme in July 2019. With the current developments progressing well, the Management is of the view that the team will continue to deliver in the future. The company is confident enough to deliver increased build rates of 250 units and care suites in FY2021 and 300 units and care suites each year thereafter, starting with 265 units and care suites due for completion in FY2020.

Past Years Financials Snapshot (Source: Company Reports)

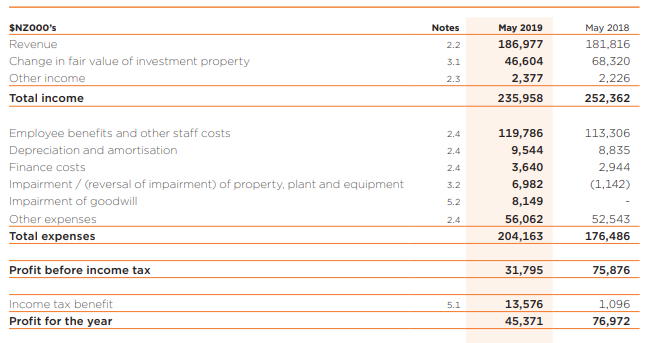

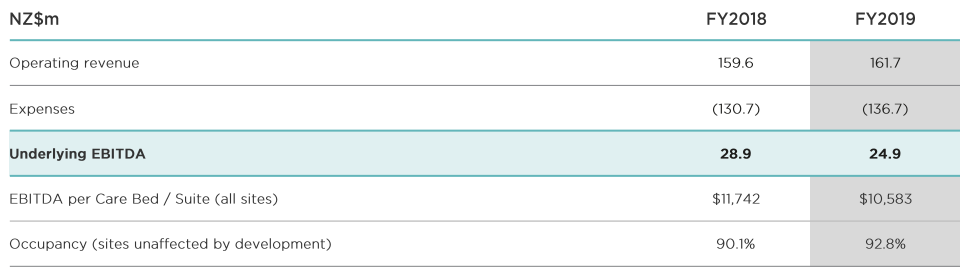

Key Highlights of FY19: The year saw a decent top-line growth the both new sites since year-end. In only three months since completion, the company sold 7 care suites and 27 retirement village apartments at The Sands. At Meadowbank, the company sold 16 retirement village apartments and 9 care suites. The company reported net profit after tax of $45.4 million which is below last year’s reported profit as a result of the valuation of existing villages remaining constant in FY19 when compared with FY18. The underlying net profit after tax from continuing operations decreased by 1.8% to $49.7 million due to increases in interest expenses to support new developments, increase of minimum wage costs for care staff and higher support office costs to commission four new care centres. The company has declared a final dividend of 2.6 cents per share, which takes full year dividends (non-imputed) to 4.7 cents per share and represents 57% of underlying net profit after tax.

Financial Summary (Source: Company Reports)

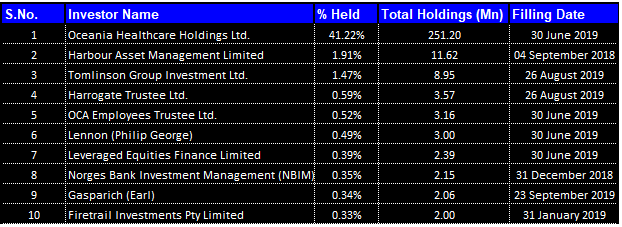

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in the Company:

Top 10 Shareholders (Source: Thomson Reuters)

Decent Balance Sheet: In FY19, the company’s total assets stood at $1.4 billion, which is a 22% increase over the previous year and reflects finished aged care and retirement village developments, as well as new land, acquired together with existing sites at a number of Auckland locations during the year. The company’s total net debt stood at $248.2 million as on 31st May 2019, which signifies a gearing level of 28.9%, compared with 22% as on previous year.

Financial position of the Company (Source: Company Reports)

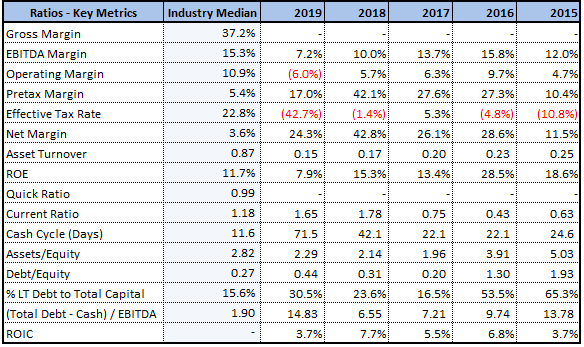

Overview of Key Metrics: In FY19, the company’s net margin stood at 24.3%, which is above the industry median of 3.6%. This represents that the company is better than its peers in converting its top line to bottom line. The company’s current ratio stood at 1.65x in FY19, above the industry median of 1.18x. The company is in a better position to meet its short-term obligations and enable the company to deploy the surplus fund towards more productive activities.

Key Metrics (Source: Thomson Reuters)

Resilient to Slow Down in the Residential Property Market: In the recent times, the growth in the residential property market has slowed down and, in some markets, there has been slight easing in prices. However, there has been a significant gap in most regions between the average house price and the asking price for independent living units. The company is not immune to the effects of the slowing property market; however, it is more resilient than other businesses because of its Care business, which can be described as need based. This means that the decision to move into the company’s aged care site by an incoming care resident is not motivated by what the property market is doing, it is led by their need for care, which is often vital.

Overview of Care Segment Business: As the company is the market leader in providing the highest levels of clinical care, aged care business is one of the main contributors to the company’s top line. As compared to the other operators, the company has a higher mix of hospital-level care beds in their portfolio. Also, the company is continually renewing in both service delivery and product offering. 38% of the company’s portfolio consists of premium beds and units at the end of May 2019, and it is likely to increase to 50% by FY20. A significant transformation in the portfolio will be achieved once the company completes the renovation of its brownfield’s development pipeline. That mix will be 70% premium and 30% standard rooms.

Aged Care Underlying EBITDA (Source: Company Reports)

Key Development During the Year: During FY19, the company delivered all 272 retirement village units and aged care bed at Meadowbank Stage Four, The Sand and The BayView. These are attracting strong demand and are a high-quality product in the markets in which the company operates. The company invested $135 million in construction capital expenditure in FY19, up $56 million over the previous-year investment of $79 million. These investments are playing a critical role in driving company’s growth through the renovation of brownfields locations, along with improving longer-term trail income flows and near-term growth margins through aged care earnings and deferred management fees.

The Company Receives Major Resource Consent: The company has acquired another substantial resource permission from Auckland Council for the renovation of its Elmwood Village in The Gardens, Manurewa, Auckland. The company has previously resource permission to build a new 142 room aged care centre on land nearby to the site that was acquired in 2016. This new permission allows the company to construct five new buildings. This new permission comprises of 229 new independent living apartments and a new community centre.

The Company Appoints New General Manager: The company has appointed Dr Frances Hughes as General Manager Nursing & Clinical Strategy and she has more than 30 years of nursing experience and has also held senior management and nursing positions on a global level. Most importantly, she was the Chief Executive of the International Council of Nurses, based in Geneva. She also worked for the WHO in the Pacific region, providing on WHO agenda for mental health from 2005 to 2011.

The Company Receives Major Resource Consent for Waimarie Street Development: The company has acquired resource permission from Auckland Council for the development at Waimarie Street in St Heliers, Auckland. Initially, the company acquired 8,945 m2 of land in Waimarie Street in March 2018 and after the company purchased adjacent properties in the second half of 2018, which expanded the company’s total holdings to 13,464m2.

What to expect from OCA Moving forward:: The company has a significant development pipeline that goes well beyond the FY20. The company has enough land to build 1,903 new units and care suites and out of those 1,903 new units, the company has even now obtained permits for 1,362 units and care suites. This represents 71% plus of that pipeline. The company is also about to start the construction of 49 new apartments in the next month. The company will start the redevelopment of Lady Allum Village in Milford, later in the year. The first stage of which is anticipated to be finished in FY22.

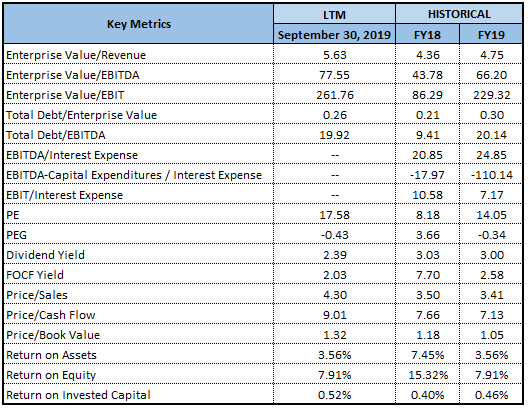

Key Valuation Metrics (Source: Thomson Reuters)

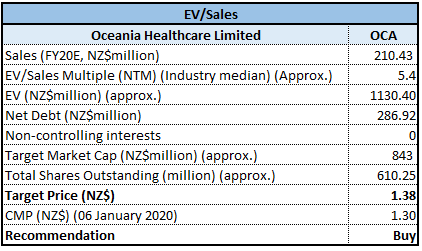

Valuation Methodology: EV/Sales Approach

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Technical Overview:

Monthly Chart:

Monthly Chart (Source: Thomson Reuters)

Weekly Chart:

Weekly Chart (Source: Thomson Reuters)

Note: Yellow colour lines represent retracements levels. Yellow colour upward slopping line is trend line.

The stock in the recent past has experienced a sharp rise in its price. In the process, it has brought stock in highly overbought zone which is reflected from RSI reading of 81.70 on weekly chart and 72.02 on monthly chart. Traders seem to be encashing this situation by part off-loading their holdings which has resulted into moderate fall in price. This fall should be interpreted as technical correction and not reversal of trend. We believe that the stock might take support around $1.1911 and from there it would move up wherein it may witness initial resistance around $1.3941. Hence, the uptrend in stock seems still intact.

Stock Recommendation: In the time period of FY15 to FY19, the company has registered a CAGR growth of 23.7% in net income. The stock is currently trading above the average of 52-week low high of $0.99 and $1.39, respectively and has given total returns of ~20.18% and ~27.18% in the past one month and three months, respectively. Considering the aforesaid facts, we have valued the stock using a relative valuation method, i.e., EV/Sales based approach, and arrived at a target price of higher single-digit upside (in % terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $1.300, down by 1.52% on 06 January 2020.

OCA Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...