Company Overview: OceanaGold Corporation (ASX: OGC) is a mid-tier, high-margin, multinational gold mining company with a significant pipeline of organic growth and exploration opportunities in Australasia and the Americas. OCG’s exploration assets are located in New Zealand, Philippines, and the United States. OGC is focused on delivering strong returns to shareholders and enhancing profitability while remaining disciplined in allocating capital. The company is listed on the Australian Securities Exchange (ASX) as well as on the Toronto Stock Exchange (TSX). OGC’s mission is to double the value of its business by 2024..png)

OGC Details.png)

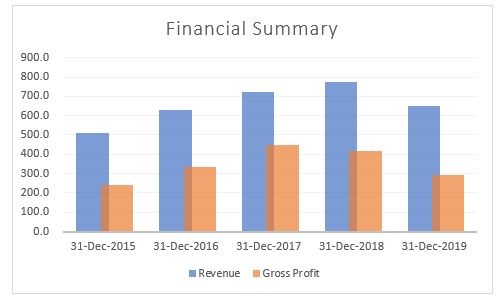

Continues to Invest in Organic Growth Initiatives: OceanaGold Corporation (ASX: OGC) is a multinational gold mining company with assets located in New Zealand, Philippines and the United States. The company’s operating assets include- the Didipio Gold-Copper Mine in the Philippines; the Waihi Gold Mine and the Macraes Goldfield Mine in New Zealand; and Haile Gold Mine in the US. Since 2015, the company is focused on investing in organic growth initiatives including exploration. These investments have worked in favor of the company and have yielded strong results, including the growth of Mineral Resources at the Martha Underground at Waihi, the Horseshoe Underground at Haile, and the discovery of additional resources at Wharekirauponga (WKP) in New Zealand. From 2015-2019, the company’s total revenue has increased at a CAGR of 6.41%.

Amid the current Covid-19 crisis, the company is managing near-term risks while planning for the long-term. Going forward, the company intends to take prudent measures to make sure that its operating cash flow matches and supports the critical timelines associated with its growth projects. On the operational front, the company expects improvements at its Haile mine with an approximately 25% increase in production in FY20 and a lower AISC relative. With a significant pipeline of organic growth and exploration opportunities in the Americas and Australasia regions, the company is progressing to double the value of its business in the next 4-years, in-line with its mission statement.

Revenue and Gross Profit Trend (Source: Thomson Reuters)

FY19 Performance Highlights: In the financial year 2019 or the year ended 31 December 2019, the company produced 470,601 ounces of gold and 10,255 tonnes of copper. In the fourth quarter alone, OGC produced 108,151 ounces of gold, 20% higher than the previous quarter with strong production from Haile and Macraes mines. All-in Sustaining Costs (AISC) for FY19 stood at US$1,061/ounce, up 38% on FY18, primarily due to lower gold sales.

In the fourth quarter, AISC was at US$980 per ounce, demonstrating a decline of 13% from the previous quarter, driven by improved cash costs. Subsequent to the end of 2019, the company announced increased mineral resources at the Martha Underground, which includes 824,000 ounces in Indicated Resources and 614,000 ounces in Inferred Resources.

For the full year, the company reported revenue of US$651.2 million and EBITDA of US$214.2 million. In Q4FY20, the revenue increased by 14% on QoQ basis, to US$152.1 million, driven by the increased sales volume from New Zealand and a higher average gold price received. As at December 31, 2019, the Company’s cash balance stood at US$49.0 million, with total liquidity of US$99.0 million and net debt of US$179.4 million..png)

Financial Summary (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 3.33%. Vanguard Investments Australia Ltd. and Quaero Capital LLP hold the maximum interest in the company at 1.52% and 0.36%, respectively.

.png)

Appointment of New CEO: On 6th April 2020, the company announced that it has appointed a highly experienced mining engineer, Michael Holmes, to the permanent role of President and Chief Executive Officer (CEO) of OGC. Mr. Holmes has been working with OGC since 2012 as Chief Operating Officer and before that he was a General Manager of Glencore’s Alumbrera operation in Argentina.

78.5 Million Gold Prepayment Arrangement: On 27 February 2020, OGC announced that it has entered into a forward gold sale arrangement, whereby it has received a pre-payment of US$78.5 million, in exchange for delivering 48,000 gold ounces between September and December 2020. This presale of future gold production will help the company in advancing its key organic growth projects as the Martha Underground project and Haile expansion whilst also managing the ongoing uncertainty around Didipio.

A Quick Look at Key Margins: For FY19, the company reported a gross margin of 44.6%, higher than the industry median of 38.9%. For the same time period, OGC reported EBITDA margin of 35.5%, higher than the industry median of 28.7%. OGC has a debt to equity ratio of 0.15x, in-line with the industry median..png)

Key Metrics (Source: Thomson Reuters)

What to expect: OGC is focused on delivering strong returns to shareholders and enhancing profitability while remaining disciplined in allocating capital. In the financial year 2020 (FY20), OGC expects gold production from Haile to increase by 25% on 2019, which will offset the year-on-year decline in production at Waihi. At Haile, the company intends to further enhance the open pit operations and increase mine productivity which will help mine to gain operational flexibility, allowing the company to revisit the Horseshoe underground mine plan.

At Macraes, OGC intends to advance its organic growth opportunities, particularly the Golden Point underground study which is expected to be completed in the H2 2020 and at Waihi, OGC expects its FY20 production to be in between 18,000 and 20,000 ounces with cash costs ranging from US$700 to US$750 per ounce sold and site AISC ranging from US$715 to US$765 per ounce sold.

At Didipio Gold Copper Mine, OGC continues to progress with FTAA renewal process. When operations resume at Didipio, the company expects trucking to resume within a week and once fully ramped up, OGC expects Didipio to produce around 10koz of gold and 1,000 tonnes of copper per month at a site AISC of between US$700 and US$750 per ounce sold.

Overall, OGC expects its gold production in FY20 to be in the range of 360,000-380,000 ounces at a consolidated AISC ranging from US$1,075- US$1,125 per ounce. The company expects its annual gold production to be stronger in the H1FY20, particularly at Haile where it expects two-thirds of the gold output from the operation in the second half of 2020..png)

2020 Gold Production (Source: Company Reports)

Covid-19 Update: As per the company’s announcement released on 26 March 2020, till now OGC has not had any confirmed cases of Covid-19 among any of its employees or contractors. Further, the company has not witnessed any material delays with orders for supplies at any operation due to Covid-19. The company has assured that, at the operational level, it follows strict protocols which include medical screening and assessment prior to attending work, and enhanced workplace hygiene and social distancing. Till now, the company has maintained its FY2020 production guidance..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation .png)

EV/Sales Multiple Approach (Source: Thomson Reuters) *1USD = 1.58 AUD as at 21 April 2020

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company’s current balance sheet is well funded to manage near-term risks and long-term initiatives. As at 26 March 2020, the company had a cash balance of US$183 million. The stock of OGC has corrected by 40% and 23.36% in the past six and three months, respectively. The stock is currently inclined towards its 52-week low of A$1.455. We have valued the stock using EV to Sales multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like St Barbara Ltd (ASX: SBM), Regis Resources Ltd (ASX: RRL), Silver Lake Resources Ltd (ASX: SLR), etc. Considering, the company’s decent balance sheet position, FY20 outlook, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of A$2.170, up by 3.333% on 21 April 2020.

OGC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...