A Brief Overview of Asset and Wealth Management Industry

2020 has been a challenging year for the policymakers and general public at large. COVID-19 has been an extraordinary event affecting millions of people across the world, pushing governments to take rigorous actions like enforcing lockdowns, closing borders and trade in an attempt to restrict the spread of the virus.

The policymakers launched sizeable stimulus packages, which included fiscal as well as monetary policy initiatives. Massive liquidity has been pumped into the system by Central Banks across the globe.

Since markets have recovered from the lows recorded in March, it also implies that assets under management of investment managers have recovered, providing a relatively better base for fee revenues and fund flows improving with confidence back amongst the investor community.

Figure 1: Performance of Global Indices

Source: Refinitiv (Thomson Reuters))

As shown above, the global equity markets have significantly recovered from the lows witnessed in March 2020 due to COVID-19 pandemic.

Generally, wealth managers’ focus revolves around preserving clients’ financial well-being by offering insurance and retirement products, while asset managers focus on producing tangible returns on the investments. Asset Management Companies (AMCs) mobilize money from investors to invest in various markets and securities, in line with the mutual investment objectives decided between the AMCs and the investors.

The prime role of an asset management company is to help investors generate income or building their wealth by investing their funds in securities, commodities and real estate markets. It is possible for AMCs to construct a scheme for different types of investment objectives. Thus, the AMC structure, through its numerous schemes, makes it feasible to tap a large amount of money from investors with diverse goals and objectives.

Surge in Investment Activities; Long-term Fundamentals Remain Intact

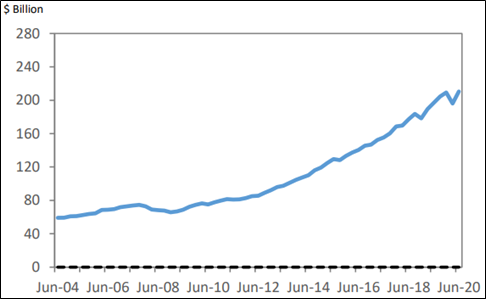

For the quarter ended 30 June 2020, total funds under management (FUM) increased by 7.3% during the quarter to $210 billion. This was the largest quarterly increase in FUM on record and was followed by the rise in financial markets after exceptional fiscal and monetary action as a result of the COVID-19 pandemic.

Figure 2: Funds Under Management

Source: RBNZ

Rise in KiwiSaver and Superannuation Funds

For the quarter to June 30, 2020, KiwiSaver net assets increased $5.5 billion to $69.0 billion, implying an increase of 8.7%. This is 5.4% higher than pre-pandemic high which was witnessed in Q4 FY 2019. Other Superannuation also increased by $1.6 billion to $29.9 billion, a 5.8% increase for the quarter.

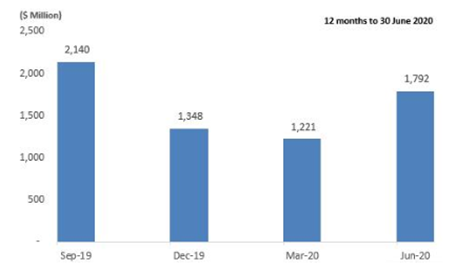

As shown below, KiwiSaver contributions have increased from $1,221 million as on March 2020 to $1,792 million as on June 2020, reflecting a rise of 46.76%.

Figure 3: KiwiSaver Contributions

Data Source: Financial Services Council, Image Source: Kalkine

Significant Rise in Holding of Shares

During the quarter, total industry holdings of listed shares increased substantially from $72.3 billion to $84.8 billion, a rise of 17.3%, which is almost back to pre-pandemic levels. Short term debt securities rose by 23.0% and long-term debt securities witnessed a marginal increase, growing 2.0%. However, cash fell during the quarter, decreasing 10.1%.

We expect the asset and wealth management companies to continue to witness the fund flows moving northwards since the global equity markets are back on track as evident from swift recovery from March lows, driven by recommencement of economic activities, easing of COVID-19 restrictions, aggressive fiscal and monetary measures by the Central Banks across the globe and severe COVID-19 containment measures by the government.

The asset management and wealth management companies are gaining traction and may continue to perform well as investors are hopeful about further stimulus package announcements. Although, the outlook for corporate earnings remains soft, equity markets across the globe witnessed a significant surge in trading and investment activities since the advent of the pandemic. This enabled most of the investment banks to increase capital market revenues in the first half of 2020, a trend that is likely to continue during the rest of the year 2020 and early 2021.

Risks in Asset and Wealth Management Companies

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the asset and wealth management sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term (TCL, AMP, HFL, GFL).

1. The City of London Investment Trust Plc (NZX: TCL) (Recommendation: Buy, Potential Upside: Low Double-Digit), (M-Cap: ~ NZ$2.679 Billion, Dividend Yield: 5.699%)

Business Description: The City of London Investment Trust Plc aims to provide long-term growth in capital and income, mainly by investment in UK equities.

Outlook

The company mainly emphasises on dividend returns to shareholders but net asset value and share price growth are of equal importance in terms of the company’s objective and investment strategy. On 30 June 2010, the company’s net asset value was £511 million. Ten years later, on 30 June 2020, the net asset value increased to £1.43 billion. In FY20, the company paid dividend of 19.0p per share, up by 2.2% Y-o-Y.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

Picking up positive momentum from the previous week, the stock opened marginally higher for the ongoing week and finally closed marginally above the previous week closing price with a gain of 0.62%. The technical indicator RSI with around 45 reading and curve at the end pointing up, suggests gaining of bullish momentum for the stock.

Going forward, the stock may have resistance around the 38.2% retracement level of $6.98 whereas support could be around the lower Bollinger band of $6.06.

Hence, we give a “Buy” recommendation on the stock at the current price of NZ$6.46 per share, up by 0.62% on October 15, 2020.

2. AMP Limited (NZX: AMP) (Recommendation: Buy, Potential Upside: Low Double-Digit), (M-Cap: ~NZ$5.21 Billion)

Business Description: AMP Limited is a wealth management company with a growing retail banking business and an expanding international investment management business. It provides retail customers with financial advice and superannuation, retirement income, banking, investment products and life insurance.

Outlook: In the second half of 2019, the company launched a three-year transformational strategy, which included a significant cost reduction program. In 2020, the company is focused on execution, and delivery of strategic priorities. It has ceased the plan to divest New Zealand wealth management business and will now focus on developing and growing the business in its existing market. On 1st October 2020, Moody’s lowered its ratings on AMP Group Finance Services Limited and AMP Group Holdings Limited from A3 to Baa2. The rating allocated to AMP Bank by Moody’s has been lowered from A3 to Baa2.

AMP has a strong balance sheet and capital position, with surplus capital of A$1.4 billion on 30 June 2020.

Recent Update:

AMP Capital has recently stated that it has agreed the sale of Axión to Asterion Industrial Partners. Axión happens to be a leading independent broadcasting as well as telecommunications infrastructure provider in Spain. Notably, AMP Capital has owned Axión on behalf of the investors in global infrastructure equity platform since the year 2016.

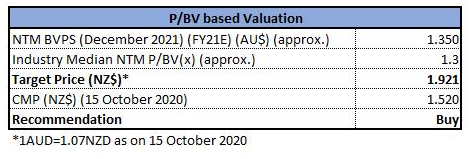

Valuation Methodology: P/BV Based Relative Valuation (Illustrative)

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

We have applied P/BV based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current price of NZ$1.520 per share, up by 0.66% on October 15, 2020.

3. Henderson Far East Income Limited (NZX: HFL) (Recommendation: Buy, Potential Upside: Low Double-Digit), (M-Cap: ~NZ$843.91 Million, Dividend Yield: 7.03%)

Business Description: Henderson Far East Income Limited aims to provide shareholders with a growing total annual dividend per share, as well as capital appreciation from a diversified portfolio of investments from the Asia Pacific region excluding Japan.

Outlook :In the coming future, the pandemic will result in lower dividends. However, in Asia, the dividends are expected to fall less than elsewhere. Asian companies are cash-rich and have room to increase the proportion of profits that they pay out to shareholders.

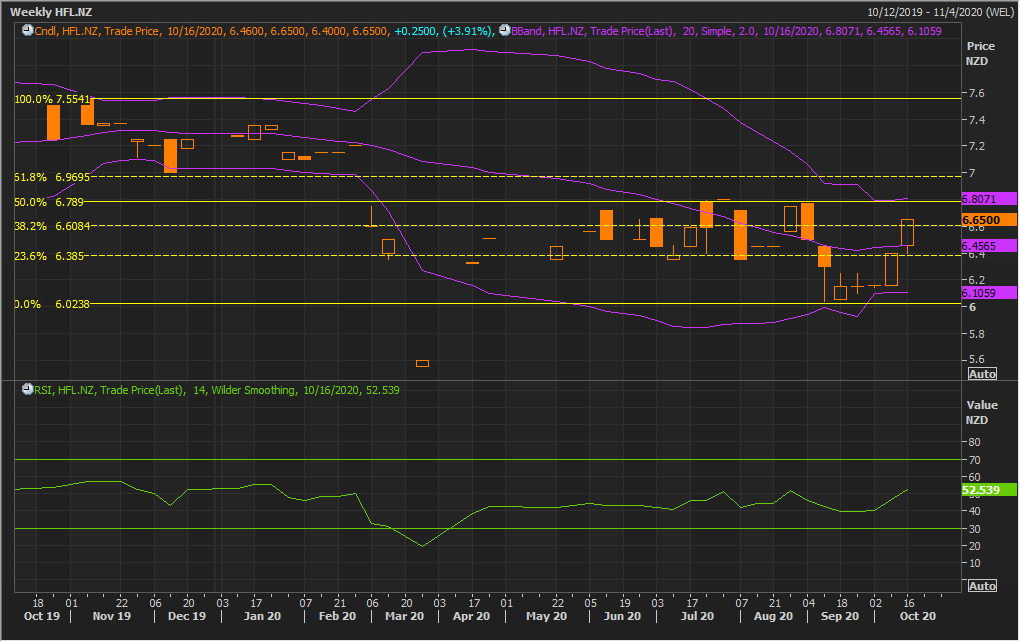

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands* with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

Continuing with the strong bullish momentum of the previous week, the stock has given strong closing for the ongoing week at its peak price of $6.65 thereby reflecting a strong uptrend for the stock. The technical indicator RSI with around 53 reading suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around the 61.8% retracement level of $6.97 whereas support could be around the 23.6% retracement level of $6.38.

Hence, we give a “Buy” recommendation on the stock at the current price of NZ$6.65 per share, up by 3.91% on October 15, 2020.

4. Geneva Finance Limited (NZX: GFL) (Recommendation: Hold, Potential Upside: Higher Single-Digit), (M-Cap: ~NZ$29.90 Million, Dividend Yield: 6.63%)

Business Description: Geneva Finance Limited happens to be a New Zealand-owned finance company which offers finance as well as financial services to the consumer credit and small to medium business markets.

Outlook: FY20 was a difficult year for the company as some operations performed very well while others required restructuring to turn around performance. However, the company is now well positioned to return to sustainable profit as well as revenue growth. The company possesses a robust balance sheet, the receivable ledgers are well provisioned, and the company is ready to take advantage of the opportunities the market will offer.

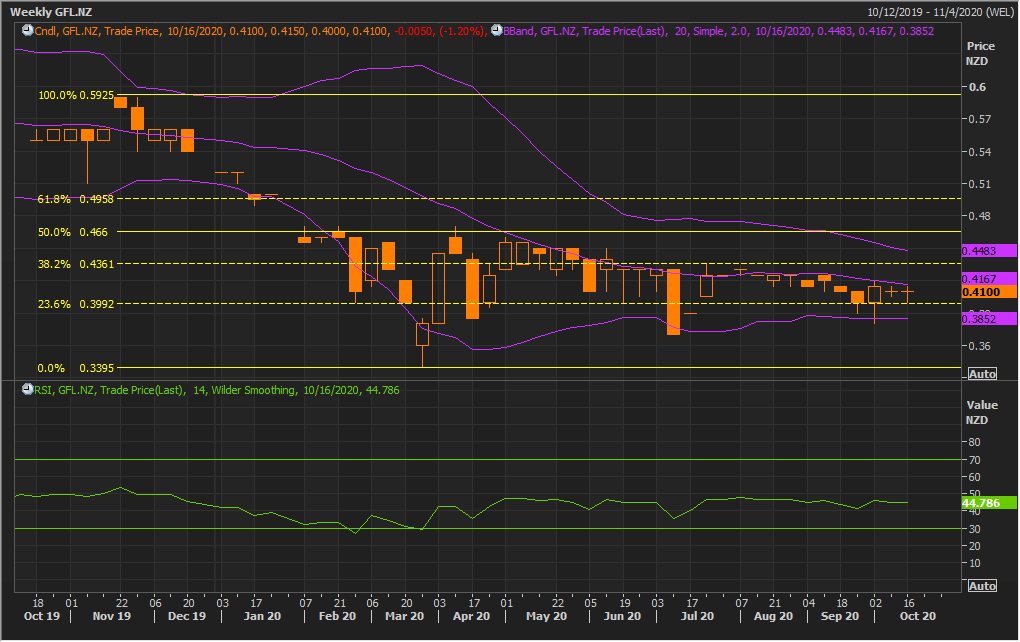

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands* with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock for the ongoing week has given close at $0.41 forming a ‘Doji’ candle. In the prior week also, the stock closed with ‘Doji’ candle formed. This reflects on indecisiveness on the part of traders/investors. The technical indicator RSI with 45 reading and flattish curve at the end suggests neutral to flattish momentum for the stock.

Going forward, the stock may have resistance around the upper Bollinger band of $0.44 whereas support could be around the 23.6% retracement level of $0.39.

Hence, we give a “Hold” recommendation on the stock at the current price of NZ$0.41 per share, down by 1.20% on October 15, 2020.

Comparative Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...