Sector Landscape

The real estate sector is the primary driver of the New Zealand economy. The sector plays a crucial role in driving the country’s financial sector as a whole and also acts as a swaying factor in directing the policies of the government as well as business strategies. New Zealand’s real estate sector is more vast and diverse ranging from residential and commercial property.

The developments in the housing market acts as a cornerstone for the Reserve Bank’s two key policy objectives: price stability and financial stability as it accounts for around half of the assets of New Zealand households.

The stock of New Zealand housing market has a blend of housing types ranging from residential buildings to attached townhouses, apartments, lifestyle blocks (with a dwelling), among others. The country’s commercial property has a mix of property types which include office, retail, industrial buildings, etc. The housing prices in New Zealand continued to remain high over the years due to sustained rise in demand and lower supply of the properties around the country as reflected in Exhibit 1 below.

Exhibit 1: Trend in Housing Prices and Value of Housing Stock

.png)

Key Growth Drivers

Some of the key growth drivers for the Real Estate sector have been highlighted below: -

Traction in Demand

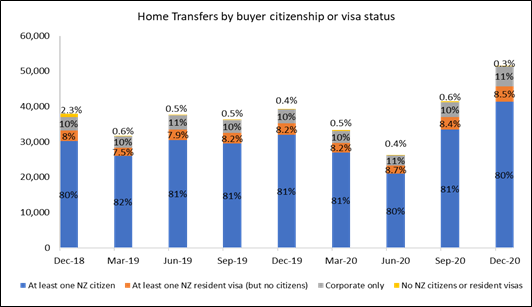

The sector continues to witness sustained traction in demand over the years. In the face of the low supply situation in the country as compared to the robust demand scenario has triggered prices in the real estate market to remain hot. The traction in the demand environment can be better illustrated by the decent property transfer activities in the country in the quarter ended December 2020 with 51,504 property transfers (involving a home) incurred as provided in Exhibit 2 below.

This marked a robust growth of 31% as compared to the December 2019 quarter. The traction in property transfer during the period was driven by the healthy demand of the same from the local residents as out of the overall property transfers 80% accounted for at least one New Zealand citizen. This was followed by corporate entities (New Zealand or overseas owners) with 11% share and New Zealand-resident-visa-holder (but no citizens) accounted for 8.5%. However, no NZ citizens or resident-visa holders accounted for a minuscule 0.3% during the period under consideration.

Exhibit 2: Healthy Momentum in Home Transfers

Source: Stats NZ; Chart Created by Kalkine Group

Low- Interest Rates

The prevailing low-interest rate is also one of key contributing factors to the sustained momentum in the real estate sector as a whole. The prevailing low- interest rates scenario as well as the benefit of affordable borrowing has enticed various first home buyers and investors, thus driving the overall growth of the sector.

The Reserve Bank of New Zealand has consistently maintained its Official Cash Rate (OCR) at a low rate of 0.25% from mid-March 2020 and it is widely believed that the central bank will continue with accommodative policy for considerable period with the objective of stimulating economic growth. Consequently, this has resulted in a reduction in market interest rates, including mortgage interest rates. The standard interest rate on new residential mortgage lending also continued to decline across tenors and the average two-year fixed mortgage interest rate declined to 3.51% in December 2020 from 4.44% in December 2019. However, the floating rate on new standard residential mortgage lending also reduced to 4.51% in December 2020 from 5.45% in December 2019.

The ideal investment environment created in terms of low-interest policy, incentivizing affordable housing, facilitating overseas investment in real estate is not only luring the domestic buyers but also the overseas investors. This is evident from the home transfers to overseas people which remained the highest in districts like in Waitemata and Queenstown-Lakes for the year ended December 2020 as visible in Exhibit 3 below. During the period, these particular districts witnessed maximum home transfers to people without having the status of New Zealand citizenship or resident visas. This includes Waitemata local board saw 195 home transfers while Queenstown-Lakes district observed 57 home transfers. Further, Christchurch city also witnessed 57 home transfers during the period under consideration.

.png)

The heightened expectation of prevailing low- interest rate scenario to continue in the medium term is providing visibility on the sustainability of the growth momentum, going ahead.

.png)

Rising Employment Levels

The growth of the real estate sector in the country is also fuelled by the high employment level which is in turn, contributing to the demand for property in New Zealand. Further, the support extended by the government in times of Covid-19 pandemic to support the job markets by pouring liquidity into the system as well as providing wage subsidy scheme to businesses helped address probable rise in unemployment concerns to greater extent. This bodes well for the overall sector growth as a whole. The employment level showed signs of improvement in the December 2020 quarter and the seasonally adjusted employment rate increased to 66.8% from 66.4% in the previous quarter provides visibility on the growth prospect of the sector. Additionally, the lifting of the most of the COVID-19 related restrictions in the country and the resumption of business activities have a positive impact on employment generation and for that matter on real estate sector.

Besides, the sector witnessed a record number of new homes consented in the December quarter 2020 which stood at 39,420. This was mainly driven by new townhouses, flats, and units consented that registered a decent growth from 8,208 in the year ended December 2019 to 11,603 in the year ended December 2020. They constitute nearly a third of overall new homes consented. While the value of consents for multi-unit homes grew by around 11% in the year ended December 2020, the value of stand-alone houses rose by 0.5%. Meanwhile, the value of residential consents during the period under consideration stood at around $16.5 billion. This constitutes more than 68% of the total value of all consents in 2020.

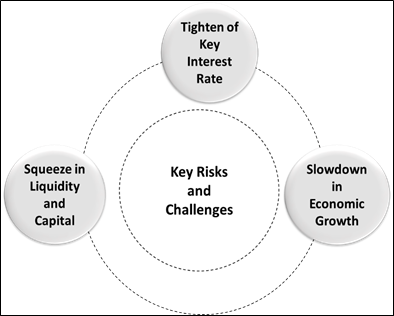

Key Risks and Challenges

Some of the risks attributable to the sector are shown below:-

Exhibit 5: Key Risks and Challenges

Source: Kalkine Group

Outlook

The growth prospect of the sector is largely driven by the sustained demand momentum which largely depends on availability of liquidity, booming job markets and supportive government real estate policy. The government has the realization of this fact and it is expected that it would be ensuring high liquidity at the marketplace by way of maintaining low-interest policy and providing sector-specific stimulus.

Moreover, recent data by Stats NZ indicated strong growth in average earnings in the December 2020 quarter and average ordinary-time hourly earnings in the quarterly employment survey (QES) increased 4.2% to $34.14. Additionally, the average ordinary-time weekly earnings also witnessed a growth of 3.6% annually to $1,289. The increasing income level paints a brighter prospect for the sector going forward. Besides, the Reserve Bank of New Zealand outlined the details of the Funding for Lending Programme (FLP) wherein it will lend funds to eligible counterparties at the Official Cash Rate (OCR) for a term of three years in order to reduce the funding costs of banks also provides sustainable growth visibility of the sector.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Goodman Property Trust (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.1 billion, Gross Dividend Yield: 3.102%)

Business Description:

Goodman Property Trust (NZX: GMT) is engaged in the business of owning, developing and managing industrial real estate globally which includes logistics facilities, warehouses and business parks.

Outlook

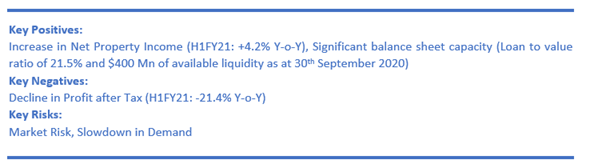

The company enjoys the benefit of well-capitalised balance sheet which has aided GMT in exploring potential new opportunities for growth. Its balance sheet strength was reflected by its loan to value ratio which stood a 21.5%. Notably, refinancing of GMT’s bank facility has been completed, increasing weighted average debt term to 5.1 years as well as providing $400 Mn of the available funding capacity. So, this will enable the company to tap future investments. Meanwhile, the company expects FY21 cash earnings to be at least 6.3 cpu.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

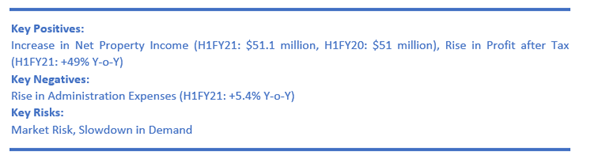

We have applied EV/Revenue multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to the peer average EV/Revenue (NTM Trading multiple) considering its increase in net property income, robust balance sheet capacity and respectable levels of available liquidity.

Thus, considering the expected upside and growth in net property income, we give a “Buy” rating at the price of $2.25 per share, up by 0.45% on February 4, 2021.

2) Argosy Property Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.3 billion, Gross Dividend Yield: 4.467%)

Business Description:

Argosy Property Ltd (NZX: ARG) is one of NZ’s leading listed property companies.

Outlook

ARG is strongly placed on the back of its portfolio of quality investment properties which is having a diverse tenant composition. This provides stability to the cash flows for the company going ahead. Meanwhile, it has guided for providing higher dividend of 6.45 cents per share for FY 2021. This reflects continued delivery of the company’s strategy. The strong execution of strategy as well as delivering on the crucial 2021 focus areas including initiatives of capital management is positioning the company well for the future. It would continue to reap benefits of the strategic acquisitions which have the potential to drive long-term capital growth as well as earnings.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

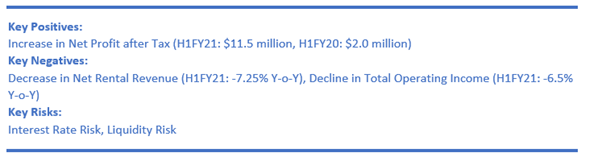

Thus, considering the increase in net property income and PAT, we give a “Hold” rating at the price of $1.555 per share, up by 0.32% on February 4, 2021.

3) Asset Plus Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$126.9 million, Gross Dividend Yield: 6.311%)

Business Description:

Asset Plus Limited (NZX: APL) happens to be a listed property investment management company which manages a property portfolio of commercial as well as industrial buildings in major cities of NZ.

Outlook:

The company is focused towards the 35 Graham Street redevelopment opportunity. Notably, pre-leasing happens to be a critical element to the process. Also, the company continues to search for new opportunities and it is confident in being able to secure these in the near term as APL requires scale to set a stronger platform for the growth.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

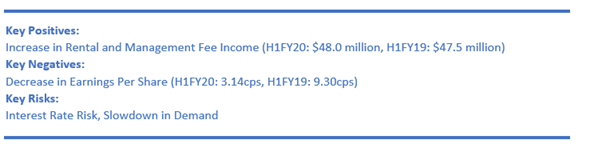

We have applied EV/Sales multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to the peer average EV/Revenue (NTM Trading multiple) considering its growth in NPAT and its search for new opportunities which could help in overall growth.

Thus, considering the expected upside and growth in NPAT, we give a “Hold” rating at the price of $0.35 per share on February 4, 2021.

4) Property for Industry Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.4 billion, Gross Dividend Yield: 3.386%)

Business Description:

Property for Industry Limited (NZX: PFI) is an NZX listed property vehicle specializing in industrial property. It has a nationwide portfolio of 93 properties, valued at over $1.47 billion.

Outlook:

The robust demand for industrial space led by increased e-commerce volumes and businesses looking to create more localized and resilient supply chains are trends that are expected to benefit the company. The company is possessing robust balance sheet which could help the company moving forward. Also, PFI is well-positioned to respond to challenges as well as any opportunities that could arise.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied EV/Sales multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to the peer median EV/Revenue (NTM Trading multiple) considering its decline in EPS, risks related to COVID-19 pandemic and decline in gross and net margins.

Thus, considering the expected upside and robust balance sheet, we give a “Hold” rating at the price of $2.905 per share, down by 0.85% on February 4, 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...