Sector Landscape and Outlook

Healthcare services in New Zealand is of high quality and it consists of both public as well private healthcare system. While the public healthcare system provides essential healthcare services that spans across emergency care, essential surgery, and hospital care. These services are offered to the citizens of the country at free of cost or at a highly subsidized rate. To access the benefits of the public healthcare system, the citizens are required to get registered themselves with a specialized doctor.

There are various organizations within the country’s healthcare sector viz; District Health Boards (DHBs), Primary Health Organizations (PHOs) and Public Health Units (PHUs), among others, who have their own set of duties and responsibilities. With 20 DHBs in the country which are being funded and guided by the Ministry of Health are engaged in providing or funding the public health services in government hospitals in respective district in the country. While the public health services in the respective regions are carried out by the 12 PHUs, which are owned by DHBs with emphasis on environmental health, containment of communicable disease as well as tobacco and health raise initiatives.

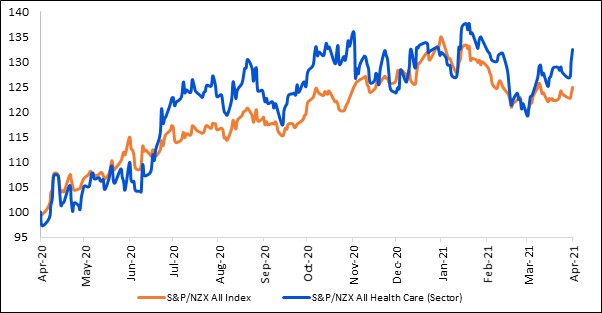

Exhibit 1: S&P/NZX All Health Care (Sector) v/s S&P/NZX All Index (One-Year Chart) *

Source: S&P Global; Chart Created by Kalkine Group

*Till April 8, 2021

The S&P/NZX All Healthcare sector has outperformed the S&P/NZX All Index with a 1-year return (8 April 2020 - 8 April 2021) of 32.42% as against the index’s 1-year return of 24.88%.

Traction in Government Funded Medicines

PHARMAC (Pharmaceutical Management Agency of New Zealand), which was established by the government of New Zealand to see through the range of medicines as well as vaccines and devices to be funded by the government, manages a static budget for the same. This is clearly visible from the $1.04 billion worth spending on medicines being managed by the firm in 2019-20 which was entirely devoted towards new medicines. As of now, PHARMAC funds around 1,000 diverse medicines which are spread over 2,000 different preparations. These medicines are made available to the citizens though hospitals and pharmacies. Around 3.74 million citizens garner the benefits of funded medicines each year.

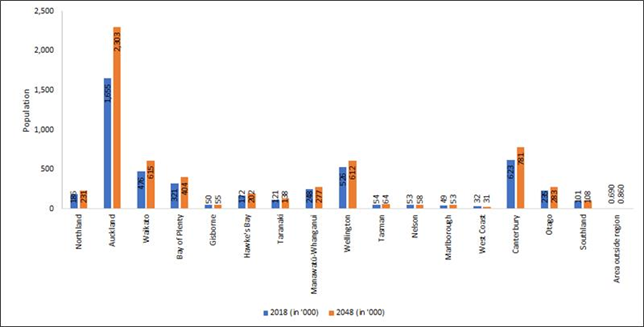

Growing Population Propels Demand

As per Stats NZ, which anticipates an acceleration in the country’s population with fifteen regions to witness increase in population in 2048 as compared to 2018. New Zealand has witnessed a highest pace of growth in its population since 1960s for the year ended June 2020 which stood at 2.3%. Going forward, the population is estimated to grow at an average rate of 1% during 2018 to 2033 (median projection) and from 2033 to 2048, the population is projected to grow at an average rate of 0.6% annually, which will boost the demand prospects for quality healthcare.

Exhibit 2: Region Wise Population Medium Projection 2018 and 2048

Source: stats.govt.nz; Chart Created by Kalkine Group

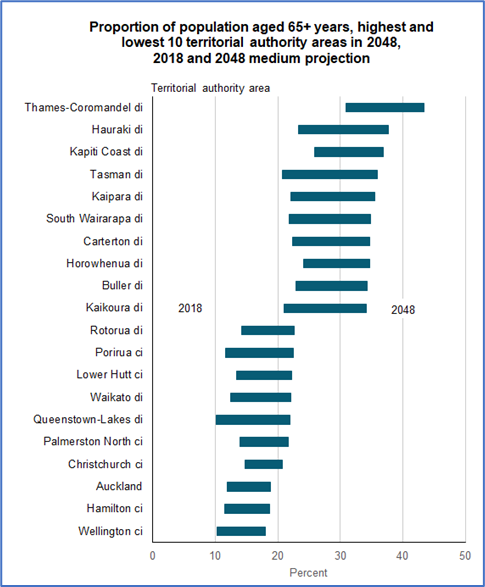

Expected Acceleration in Aged Demography

As per Stats NZ, the proportion of old age people is expected to grow across territorial authority (TA) areas of the country. The National population projections indicate that the number of aged people with age more than 65 years is likely to reach 1.36–1.51 million in 2048 and to 1.61–2.22 million in 2073 as compared to 0.79 million in 2020. The proportion of people with age over 65 years is expected to rise between 21–26% by 2048 and between 24–34% by 2073 from current level of 16% in 2020. This propels demand for healthcare services considering the rising incidence of long-term as well as chronic conditions prevailing among ageing population.

Exhibit 3: Projection of Proportion of Population with Age Over 65 Years Across TA Areas

Source: stats.govt.nz

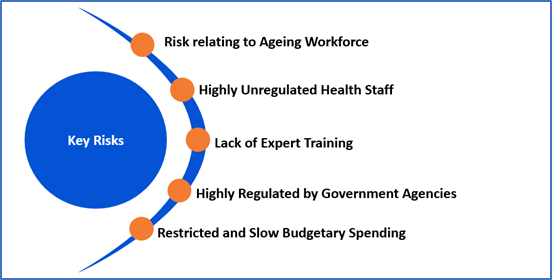

Key Risks and Challenges:

Besides, the other broad risks include the country’s ageing and a highly unregulated health workforce . The country has 40% of doctors and 45% of nurses with age more than 50 years. Moreover, majority of its health workforce have gained experience or are trained abroad. Thus, it is utmost crucial to provide sustained necessary training to its health workforce to cater to the desired skills set required. As the New Zealand healthcare sector enjoys a unique benefit of public health system which is entirely funded or highly subsidized, any restriction in budget spending towards healthcare services by the government would adversely affect the sector’s growth.

Exhibit 4: Key Risks in Healthcare Sector:

Source: Analysis by Kalkine Group

Outlook

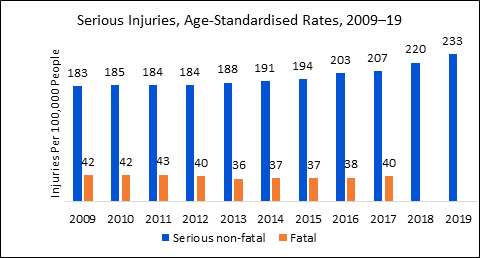

The country has been witnessing a sustained rise in serious injuries which includes both fatal as well as non-fatal injuries since 2012. As per the provisional data from Stats NZ, the proportion of serious non-fatal injuries per 100,000 people in the country has been on a consistent rise since 2012 reach 233.4 in 2019. This marked the highest serious non-fatal injuries rate since the series started in 2000.

Exhibit 5: Increasing Rate of Serious Injuries Since 2012

Source: stats.govt.nz; Chart Created by Kalkine Group

Besides, the increase in the country’s average earnings enlightens the demand for quality healthcare services. As per Stats NZ, in the quarterly employment survey, the average ordinary-time hourly earnings improved 4.2% in the December 2020 quarter to $34.14. While the average ordinary-time weekly earnings rose 3.6% annually to $1,289. Considering, projected acceleration in the country’s population coupled with estimates of higher life expectancy of more than 80 years for new-born boys and girls and increasing health awareness among citizens, the prospects of the healthcare care sector looks bright.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1. AFT Pharmaceuticals Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$446.57 million, Gross Dividend Yield: 0.000%)

Business Description:

AFT Pharmaceuticals Ltd (NZX: AFT) is engaged in developing, licensing, and selling pharmaceutical products in Australasia and around the world. Its product line across Australasia has increased to over 130 prescription and non-prescription products.

Outlook

AFT has delivered a decent performance in the face of challenging market conditions. The performance was further aided by its strategy of not only to augment its presence in the key markets of Australia, New Zealand and Asia but also to enhance its international revenues through the out licensing of its intellectual property. Additionally, the refinancing of its debt and healthy capital base (following the raising of additional capital worth $12 million) has better positioned the company in taping future growth opportunities.

Apart from this, the recent signing of licensing deal for Maxigesic® IV has not only expanded Maxigesic IV’s footprint across Europe but also increased the market for the medicine thereby improving the revenue growth outlook.The revenue growth is expected to increase with the recent signing of agreements and distribution deals, launching of new products and the great efficacy that the Crystawash sanitiser has exhibited.

Meanwhile, the company on 1 April 2021 has guided that it expects revenue of ~$110 million in FY21, an improvement from FY20’s revenue of $105.6 million. Further it expects to achieve operating profit in the range of $9 million to $11 million in FY21, compared with $11.4 million in FY20.

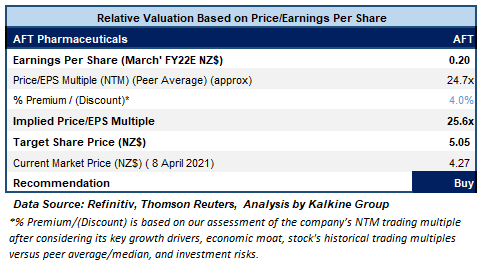

Valuation Methodology: Price/Earnings Based Relative Valuation (Illustrative)

We have applied Price/Earnings based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to Price/Earnings Multiple (NTM) (Peer Average) considering its continued focus towards augmenting its in-licensed portfolio which provides long term revenue visibility. Also, to drive growth in its Australian market, it has added new medicines to its in-licensed portfolio which is likely to boost sales significantly going forward. For this purpose, we have taken peers like Fisher & Paykel Healthcare Corporation Ltd (FPH.NZ), EBOS Group Ltd (EBO.NZ), Ryman Healthcare Ltd (RYM.NZ), to name a few.

Given its sustained investment plans along with a pipeline of development opportunities, decent outlook, and sales growth potential, we give a “Buy” recommendation on the stock at the current market price of $4.27 per share, on 8th April 2021.

2. Arvida Group Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$895.1 million, Gross Dividend Yield: 3.193%)

Business Description:

Arvida Group Ltd (NZX: ARV) is one of the leading operators of the aged care facilities as well as retirement villages in New Zealand. The company has 32 retirement communities spread across New Zealand, with a range of living options to cater the specific requirements.

Outlook

ARV is on an expansion mode driven by continued sales momentum. ARV is on track to complete 247 units/beds in FY21. Of which 29 apartments and 55 care suites of the new Copper Crest care suite centre in Tauranga are to be delivered in Q4FY21. Further the new care and apartments wing at St Albans in Christchurch is scheduled to be delivered in Q4FY21. Moreover, it is eyeing to deliver more than 200 units in FY22, reflecting continued strong sales activity. Besides the company is also looking at continued acquisition opportunities, including well located greenfield properties and other opportunities. Further, continued buoyancy in the property market, high care occupancy and an underlying positive organisational culture, bodes well for future growth.

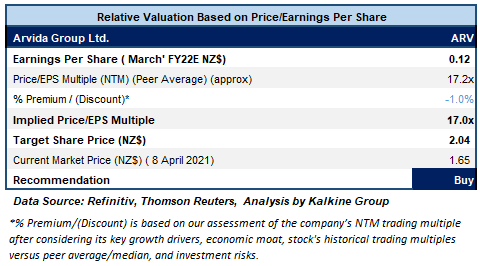

Valuation Methodology: Price/Earnings Based Relative Valuation (Illustrative)

We have applied Price/Earnings based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to Price/Earnings Multiple (NTM) (Peer Average) considering its pressure on earnings in H1FY21, higher debt level and the associated risks. Meanwhile, its total asset base of $2 billion remained strong with value of investment property of $1.7 billion. Moreover, total portfolio embedded value stood -at $410 million driven by 5% YoY rise in FY21. For this purpose, we have taken peers like Summerset Group Holdings Ltd (SUM.NZ), EBOS Group Ltd (EBO.NZ), AFT Pharmaceuticals Ltd (AFT.NZ), to name a few.

Considering its continued sales momentum and robust growth plans, we give a “Buy” recommendation on the stock at the current market price of $1.650 per share, down by 0.60% on 8th April 2021.

3. Rua Bioscience Ltd (Recommendation: Speculative Buy), (M-Cap: NZ$57.5 million, Gross Dividend Yield: 0.000%)

Based in New Zealand, Rua Bioscience Ltd (NZX: RUA) is engaged in pharmaceutical business and is targeting to be a leading producer of cannabinoid derived medicines for both domestic as well as export markets.

Outlook:

The company focuses on executing on its export-led strategy to deliver sustainable revenue. With the securing of binding sales agreement with one of Germany’s leading distributors of medicinal cannabis - Nimbus Health, the company is focusing on export led strategy and it expects its first wholesale export of dried cannabis flower to happen by the end of 2021. On 22 October 2020, the company was listed on NZX main board. The IPO to the tune of $20 million was oversubscribed. Funds received from IPO has been deployed across strategic priority areas that supports achieving initial sales and revenue targets.

In a major milestone, the company has commenced export of a sample of medicinal cannabis flower to Germany.

Technical Overview

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: The purple color line in the chart shows RSI (14-period) and the yellow color line represents trend line. The red color line represents 21-period SMA.

On the daily chart, the RUA prices are moving in a falling channel formation from past 4-month and now prices are facing resistance near the upper band of the pattern at NZD 0.43 level. However, the momentum oscillator RSI (14-period) is trading in an oversold territory at ~31 level and formed a positive divergence, a rebound from here may push the price higher towards the resistance level at NZD 0.43. An important support level for the stock, is placed at NZD 0.398, while key resistance level is placed at NZD 0.43.

Considering its competitive edge in New Zealand to cultivate cannabis for research purpose along with its strong liquidity profile and decent outlook, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.41 per share, down by 1.2% on 8th April 2021.

4. Pacific Edge Ltd (Recommendation: Hold, Potential Upside: High Single-Digit) (M-Cap: NZ$720.5 million, Gross Dividend Yield: 0.000%)

Pacific Edge Ltd (NZX: PEB) is a cancer diagnostics company and is engaged in the business of doing discovery and commercialisation of diagnostic and prognostic tests for better detection and management of cancer.

Outlook

To further strengthen its balance sheet, the company during the period has successfully completed $22 million placement to ANZ Investments. This will further aid the company in delivering extra growth capital which can be utilised to fast-track global growth initiatives. The company’s sustained focus on tapping growth opportunities is further evidenced by scaling its commercial operations in the US through expansion of its executive and sales teams to leverage and deliver on the Cxbladder’s existing set-up. Moreover, the company is anticipating acceleration in the commercial test volume from CMS and Kaiser Permanente which will fortify robust revenue and operating cashflow growth.

Besides, the company continues to witness adoption and increasing of test use by New Zealand public healthcare providers which is driving growth.

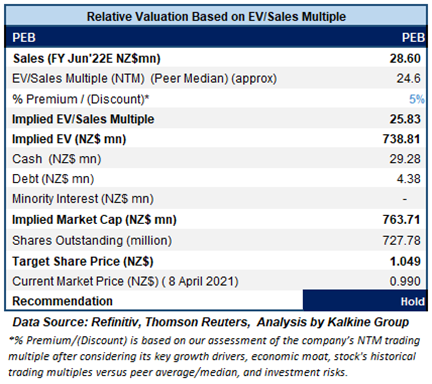

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

We have applied EV/Sales based relative valuation (on an illustrative basis) and the target price reflects a rise of high single-digit (in % terms). We have applied a slight premium to EV/Sales Multiple (NTM) (Peer Average) considering its solid liquidity position with net cash, while cash equivalents and short-term deposits rose to $29.3 million at the end of 30 September 2020.

Considering its growth strategies, scaling up of the business operations in the US, commercial agreement with Kaiser Permanente, healthy H1FY21 performance and decent outlook, we give a “Hold” recommendation on the stock at the current market price of $0.99 per share, up by 1.02% on 8th April 2021.

Comparative Price Chart (Source: Thomson (Refinitiv Reuters))

Note: Investment decision should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...