Sector Landscape and Outlook

New Zealand’s food and beverage sector plays an important role in the country’s economy. It is a mix of businesses that produce, process, and move goods around New Zealand and export to countries around the world. The country is a major food and beverage exporter and the sector accounts for 46% of all goods and services exports. These exports earn billions of dollars each year. Exports are growing at rapid pace and it has emerged as the largest exporter of dairy products and lamb, and a major exporter of beef, kiwifruit, apples, and seafood in the world. While the country is a major food and beverage exporter, it has a significant untapped capacity to export more. Over the years, the country’s wine, honey, aquaculture, and avocados have all emerged from nothing into leading export items.

The sector offers significant employment opportunity. With little training provided, a significant workforce can be absorbed in this sector. With this objective in mind, the Government of New Zealand has proposed to invest $19.3 million in a range of initiatives including training New Zealanders.

As can be seen from the above chart, S&P/NZX Primary Sector Equity Index has outperformed S&P/NZX All Index by ~11% in the span of past 5 years.

Exhibit 1: S&P/NZX Primary Sector Equity Index v/s S&P/NZX All Index (5-Year Chart)*

S&P/NZX Primary Sector Equity Index v/s S&P/NZX All Index (Source: S&P Dow Jones Indices)

*Till December 3, 2020.

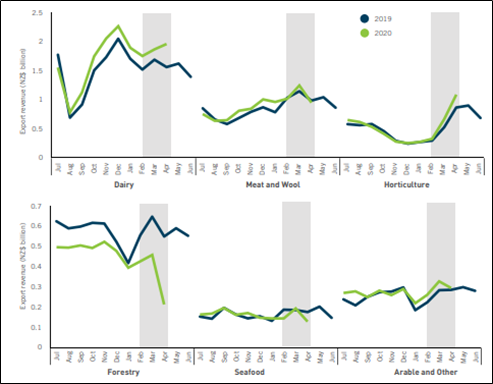

The sector has performed better than the other sectors of the New Zealand economy through the lockdown. For 2019/20, the country’s primary sector exports continue to surpass expectations with revenue up $1.6 billion Y-o-Y, reaching a record of $48 billion.

Exhibit 2: Monthly Export Revenue

Source: MPI, Stats NZ

Growing Popularity of E-commerce; Probable Rise in Disposable Income Bodes Well for Growth

The covid-19 pandemic has given rise to the growing popularity of digitization. Increasing penetration of digital technology for trade will not only aid the sector in provide scalability but also enables to reach out to each and every customer at every nook and corner of the country with their niche offerings, thus enabling the sector to target a large audience.

Apart from this, liquidity measures provided by the New Zealand government in terms of subsidies and funding to limit the economic weakness will also provide a silver lining for the sector in the long run. Among the few measures implemented by New Zealand includes a wage subsidy scheme where the employers and traders can avail of loan ranging from $350-$585.80 for two weeks. Further interest-free loans of a maximum of $11,800 to sole traders and $100,000 to organizations have also been sanctioned if the loan is repaid under the tenure of 2 years, while a lower interest rate of 3% is charged on loans of repayment tenure more than 2 years. This will provide a fillip to the disposable income of consumers and will aid in discretionary spending and resultantly buoyed consumer demand.

Resilient Export Revenue Performance Despite COVID-19 Restrictions

During the months of February and March, the country’s primary industry exports displayed signs of slowdown, as the impact of COVID-19 disrupted global supply chains and decreased demand. The two sectors that were majorly impacted during this period were forestry, which suffered from a slowdown in demand as China’s ports struggled to clear freight, and seafood, mainly live rock lobster exports to China, as the food service industry closed there.

The major impact during the two-month period was felt in the log exports, which declined by 43 percent over the same period in 2019.

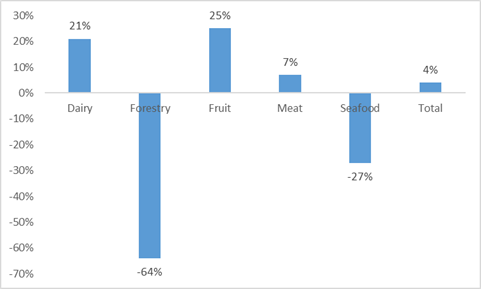

However, these falls were largely offset by gains led by good prices in dairy (excluding butter), up 12.9 percent overall, rise in gold kiwifruit production up 128 percent, and strong demand for beef outside of China up 9 percent resulting in overall exports up by 4% YoY during 26th March – 27th April 2020.

Exhibit 3: Export revenue during Level 4 restrictions (26th March – 27th April 2020) vs same period last year

Source: MPI, Kalkine Group

Government’s Budget for Primary Sector

As per Agriculture Minister Damien O’Connor, Budget 2020 makes major investments in the primary sector to support more than 10,000 people into jobs. New Zealand’s farmers, growers and producers are expected to play a critical role in the country’s economic recovery and therefore the government has decided to invest $232 million to boost jobs and opportunities in the primary sector and rural New Zealand.

In addition, $6.8 million has been earmarked to provide secured greenhouse units for new imported plant varieties and breeding material. As per the Budget 2020, the Government plans to invest $5.4 million over four years to boost regional support for animal welfare around New Zealand. This builds on investment of $20.8 million in Budget 2019.

The Government has also committed $20.2 million to help rural and fishing communities recover from COVID-19, to boost access to rural support services and community hubs.

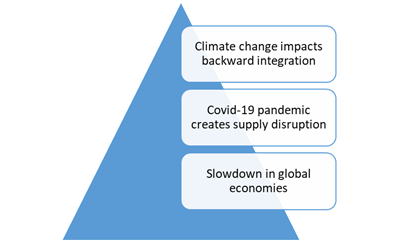

Key Challenges

Exhibit 4: Key Challenges Faced by Primary Sector

Source: Kalkine Group

Climate change impacts backward integration: For backward integration starting from procurement of raw materials, availability of farming land and availability of natural resources is under stress. Further adverse weather conditions are also posing a greater challenge for the sector. With the increasing focus on reducing emissions and the increasing use of advanced techniques in agriculture like lessening the usage of water for farming and forest land will ease pressure on backward integration.

Covid-19 pandemic creates supply disruption: Covid-19 has dealt additional setback to the sector which is already feeling the pinch of slowing discretionary demand and slowdown in the economy. This has brought uncertainty in consumer spending in the near term. This pandemic has also created a supply disruption in the global supply chain as several countries have kept the food products for their captive use only.

Slowdown in global economies: The country’s food and beverages sector rely heavily on exports and the ongoing slowdown has adversely impacted the export earnings. Further, increasing trade barriers and competition in some countries is also creating supply side risk. However, in the longer run, with the rebound in the global economies supply disruptions may get auto- corrected and export opportunities may arise in other regions of the world thereby reducing dependence on few regions for exports.

Longer term outlook remains positive

The food and beverages sector is one of the mainstays of the economic growth in New Zealand. The prevailing global pandemic (Covid-19) has adversely impacted the global economy and New Zealand’s economy is no exception with the GDP forecasted to decline sharply by 7.2% in 2020 (as per the estimates from IMF in April this year).

In the recent times, rebound in business activities has been witnessed post easing of restrictions. Border restrictions are also being gradually eased out which may lead to a sharp recovery in the food and beverage sector which has largely been dependent on tourists’ movements. The investors and business sentiments have been lifted with the news of successful testing of Corona Virus vaccine and ongoing fiscal and monetary stimulus. Thus, the huge liquidity created at the marketplace and improvement in business and consumer sentiments is likely to drive economic growth resulting in increased employment and increased disposable income which will eventually be driving discretionary spending. Thus, the medium-term to the long-term outlook appears to be bright.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in food and beverage sector.This report covers insights on the past performance of these companies and potential for growth to be delivered by them in the near to medium term.

1) New Zealand King Salmon Investments Limited (NZX: NZK) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: NZ$226.54 Million, Gross Dividend Yield: 1.694%)

About the Company

New Zealand King Salmon Investments Limited is the world’s biggest aquaculture producer of the premium King salmon species. The company has been growing as well as selling salmon to consumers for more than 30 years.

Outlook

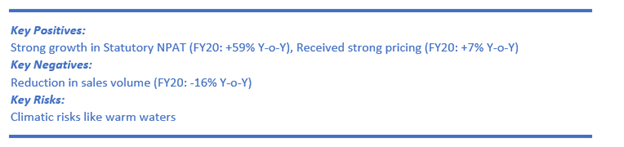

Due to the uncertainty caused by COVID-19 in the global market, the company finds it difficult to predict FY21 numbers, but considering the higher freight costs, it would be difficult for FY 2021 EBITDA to surpass that of FY 2020. However, by FY22, the company expects to again move towards demand exceeding supply, leading to improved earnings.

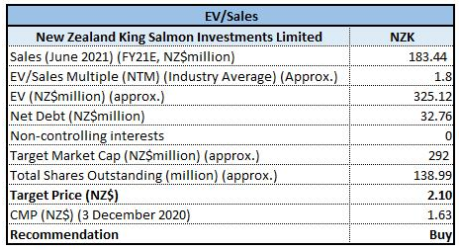

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied EV/Sales Multiple Based Relative Valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering robust growth in statutory NPAT, decent outlook and expected upside, we give a “Buy” recommendation on the stock at the current price of NZ$1.630 per share, down by 0.61% on December 3, 2020.

2) Cooks Global Foods Limited (NZX: CGF) (Recommendation: Speculative Buy, Potential Upside: High Single-Digit) (M-Cap: ~NZ$28.88 Million)

About the Company

Cooks Global Foods Limited owns the intellectual property and master franchising rights to Esquires Coffee Houses worldwide (excluding NZ and Australia). The company currently operates or franchises Esquires Coffee outlets in the United Kingdom, Ireland, Portugal, Bahrain, Kuwait, Syria, Saudi Arabia, Jordan, Pakistan, Indonesia, Canada, and China.

Outlook:

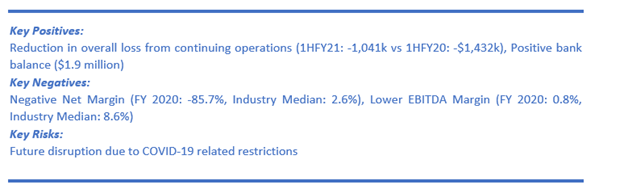

The company is confident about its outlook for FY21. Despite the impact of Covid-19, the company is happy by the resilience witnessed in the post lockdown trading in UK & Ireland through the July – October period when outlets were allowed to open in an almost normal manner. The new corporate overhead cost structure (once implemented) will further reduce the breakeven point significantly. The cost reductions along with enhanced scale from the Triple Two acquisition as well as growth in UK & Ireland would be placing the company in robust position to post positive results in FY 2022. However, this is based on the assumption that coronavirus-related trading patterns return to the more normal pattern from Q2 FY 2021.

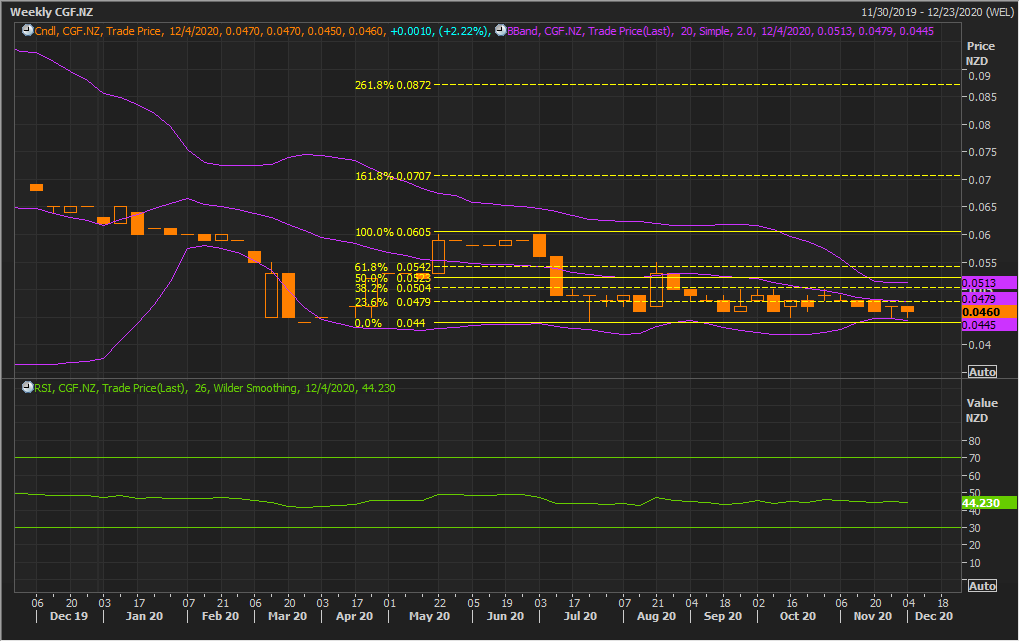

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

In the past two consecutive weeks, the stock having taken support at the lower Bollinger band has given a higher close. This suggests a likely bullish reversal for the stock. The technical indicator RSI with 44 reading indicates neutral momentum for the stock.

Going forward, the stock may have resistance around the upper Bollinger band of $0.05 whereas support could be around the lower Bollinger band of $0.04.

Considering the technical analysis and positive bank balance, we give a “Speculative Buy” recommendation on the stock at the current price of NZ$0.046 per share, up by 2.22% on December 3, 2020.

3) Delegat Group Limited (Recommendation: Hold, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$1.59 billion, Gross Dividend Yield: 1.499%)

About the Company

Delegat Group Limited (NZX: DGL) is NZ's fourth largest wine company (considering litres of wine sold). The company’s strategic goal revolves around building a leading global super premium wine company.

Outlook

The company reported decent performance in FY20. Additionally, the company is on an expansion spree in order to provide long-term potential earnings growth. To achieve this growth, DGL continues to remain capex heavy and has plans of further investment to the tune of $52.2 Mn in 2021. These particular investments are aimed at boosting the sales growth in order to achieve sales of 3,840,000 cases by 2023. There are expectations that expansion plans will better place the company to tap further growth opportunities going ahead.

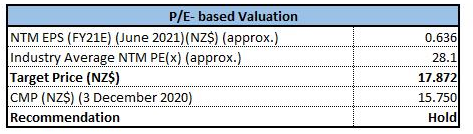

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied P/E Based Multiple Relative Valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

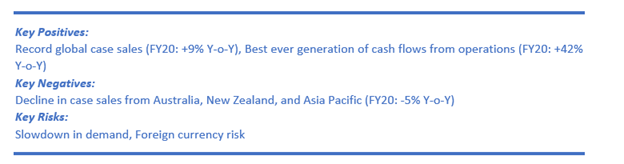

Considering record global case sales, expectations of sales growth and expected upside, we give a “Hold” recommendation on the stock at the current price of NZ$15.750 per share on December 3, 2020.

4) Comvita Limited (NZX: CVT) (Recommendation: Hold, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$231.66 Million)

About the Company

Founded in 1974, Comvita Limited (NZX: CVT) is currently one of the leading players globally of the Mānuka honey category.

Outlook:

Although Covid-19 pandemic has impacted various sectors negatively, however, it proved to be a blessing in disguise for the companies dealing in natural health products as consumers turned more health conscious and flocked towards natural products. Resultantly, the company witnessed robust growth in FY20 both in terms of revenue and profits across its key markets including North America and China. Further, better operating leverage provides scope for future expansion plans for the company.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied EV/Sales Multiple Based Relative Valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

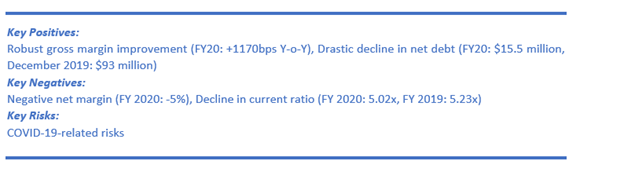

Considering improvement in gross margin and expected upside, we give a “Hold” recommendation on the stock at the current price of NZ$3.320 per share, down by 1.78% on December 3, 2020.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...