.png)

I. Sector Landscape and Outlook

The financial system has been tightening monetary circulation in the past couple of months due to expectations to increase the central bank policy rates in NZ and overseas. Robust global and domestic statistics have increased confidence that economic conditions look upon higher interest rates in the coming years. Interest rate swap rates have also grown, mainly due to higher expectations for short-term interest rates. Swap rates are currently at their highest levels since 2018. The 2-year swap rate is over 200 bps higher than its low earlier this year. Further, the market expects the official cash rate to reach at least 2% by August next year, 100 basis points higher than previous expectations.

Robust Financial System Supporting Financial Institutions to Accelerate

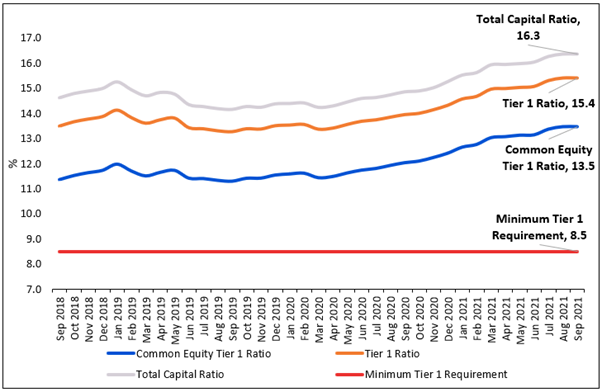

As per the Reserve Bank of New Zealand (RBNZ), the financial system in the country has been resilient throughout the pandemic and regularly supports households and businesses. The banking system’s earnings have grown over the year, primarily driven by dividend restrictions and lower risk-weighted asset growth that accelerated banks’ capital ratios to their highest levels. As a result, the banks are better placed to meet the higher requirements despite Alert Level restrictions. In addition, the non-bank deposit taker (NBDT), insurance, and financial market infrastructure (FMI) sectors have also shown signs of resilience and remained comparatively stable. Insurers’ profitability has been moderate, and capital structure was supportive due to lower dividend payments.

Exhibit 1: Trend in Capital Ratios of Local Banks in NZ

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Sound Financial Position of Businesses Indicating Strong Economic Recovery

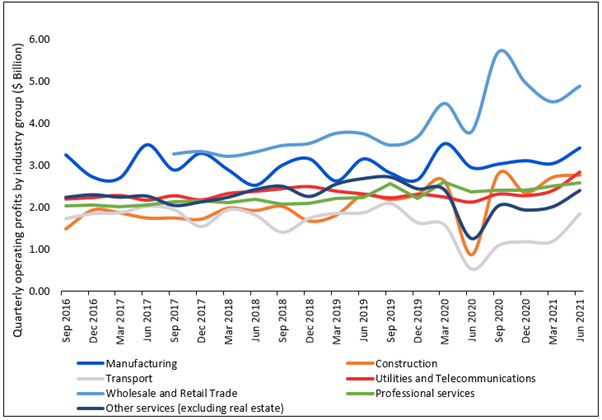

As per RBNZ, the balance sheets of industries are resilient, with stable debt as a share of GDP since 2010. Also, debt servicing costs is at minimal levels as interest rates have reduced significantly. Real GDP in the June quarter was higher than the pre-pandemic level. In multiple cases, the growth of economic activity was reflected by business incomes gradually rising to pre-pandemic levels. Besides, increased export prices have seen the dairy industry deleveraging. Also, the banks have extended to diversify their agricultural lending towards horticulture. However, the residential property development sector is at the risk of increasing debt servicing costs and decreasing profit margins.

Exhibit 2: Growing Operating Profits by Industry Group

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Foreign Exchange Turnover Rebounded in October 2021

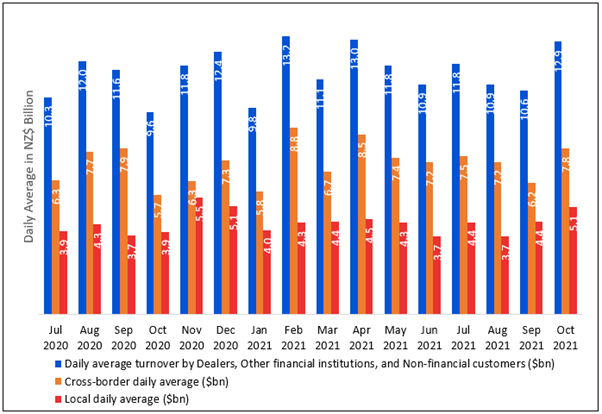

As per the RBNZ, the average daily foreign exchange transactions from Dealers, Other financial institutions, and Non-Financial Customers in October 2021 stood at $12,903 million, against $9,573 million in the same month last year. This reflects an increase in offshore capital investment into NZ and the associated higher global profile of the NZ dollar. As a result, foreign exchange trading in NZ has also increased, mainly in line with global trends.

Exhibit 3: Daily Average Foreign Exchange Turnover Trend since July 2020 to October 2021

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Financials Index generated a 1-year return of ~29.75% versus ~-0.46% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~30.21% in 1-year.

Exhibit 4: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

Key Risks and Challenges:

The international economy continues to face challenges due to COVID-19 related circumstances. Ongoing supply chain disruptions are creating additional costs for businesses, thereby resulting in higher inflation. Further, higher global interest rates could impact asset prices.

Robust demand for housing is resulting in price pressure. As a result, the buyers are borrowing more relative to their income. Loan-to-value ratio (LVR) restrictions are the crucial tool to address risks related to the housing market. Further, climate change indicates both long-term risks and opportunities to financial institutions. Therefore, gauging and managing climate-related circumstances is required to strengthen the ongoing financial stability.

Exhibit 5. Key Risks in Financial Sector:

Sources: Analysis by Kalkine Group

Outlook:

The RBNZ is working with Pacific Island Central Banks and International Businesses to make remittances to the Pacific simpler, safe, and cost-effective. Resultantly, this will maintain financial corridors and services to enable Pacific countries’ recovery and growth, which will support the stability and prosperity of the domestic economy.

RBNZ plans to progressively increase the capital requirements for banks from 1 July 2022 to ensure the banking system is resilient to overcome economic risks. In doing so, the banking system have already made strong progress on this, as profitability recovered over the past year while dividend restrictions have remained in place. In addition, RBNZ plans to increase the minimum core funding ratio (CFR) requirement to its previous level of 75% from 1 January 2022, subject to no significant worsening in economic conditions.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Australia and New Zealand Banking Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$78.54 billion, Gross Dividend Yield: 5.962%)

Business Description:

Australia and New Zealand Banking Group Limited (NZX: ANZ) offers banking and financial products and services to more than 8.7 million retail and business clients and operates across 32 markets.

Outlook:

The bank has transformed itself as per the modern requirement and policies. It has been deployed towards group-wide automation, cloud migration, and digitisation to enable low-cost, sustainable customer growth. In Australia, the bank has been building growth-oriented retail and small business propositions, which are centred around delivering compelling digital offerings that would improve the financial well-being of the customers and drive long-term customer and revenue growth.

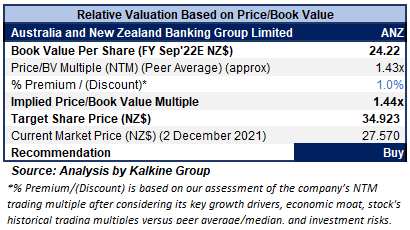

Valuation Methodology: Price/Book Value Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using Price/Book Value Per Share multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). In addition, a slight premium has been assigned to Price/Book Value Per Share Multiple (NTM) (Peer Average), considering solid areas of interest like supporting the electrification of the transport supply chain, commercialisation of hydrogen, financing energy-efficient buildings and assisting customers in establishing and developing their transition plans.

Considering the facts above, we give a “Buy” recommendation on the stock at the current market price of $27.57 per share as of 2nd December 2021 (New Zealand Time: 12:27 PM (GMT +12).

2) Kingfish Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$619.93 million, Gross Dividend Yield: 7.631%)

Business Description:

Kingfish Limited (NZX: KFL) is an investment company with a focus on growing investors' capital through portfolio management and offering regular dividends.

.png)

Outlook

During the first six months of FY22, some of the most extensive portfolio positions significantly outperformed the market. The strategy is to handpick a concentrated portfolio of high-quality companies delivering robust performance. However, the valuations are now a little elevated, which suggests lower investment returns generally, prompting companies for active decision making.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the facts above, we give a “Buy” recommendation on the stock at the current market price of $1.94 per share as of 2nd December 2021 (New Zealand Time: 12:35 PM (GMT +12).

3) NZX Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$491.21 million, Gross Dividend Yield: 4.707%)

Business Description:

NZX Limited (NZX: NZX) operates New Zealand’s equity, debt, derivatives, and energy markets. It also provides clearing, trading, depository, settlement, and data services.

Outlook

The interim results of the company reflect strength across businesses. The increase in volume and turnover heightened the interest of investors across different forms of investment and asset classes. With both retail and institutional investors looking for a broader range of investment opportunities, the company's earnings are expected to increase in the upcoming years. As a result, the company expects its FY21 operating earnings to be in the range of $32.0-$35.5 million, subject to market outcomes.

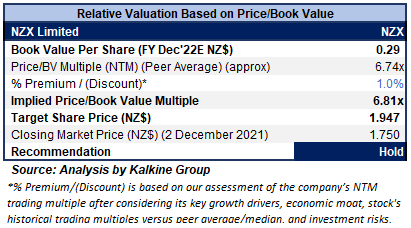

Valuation Methodology: Price/Book Value Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using Price/Book Value Per Share multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been assigned to Price/Book Value Per Share Multiple (NTM) (Peer Average), considering the decline in the debt to equity to 0.65x in H1FY21 versus 0.73x in H1FY20 and improved guidance for FY21.

Considering the facts above, we give a “Hold” recommendation on the stock at the closing market price of $1.75 per share, down 2.78% as of 2nd December 2021.

4) Tower Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$290.94 million, Gross Dividend Yield: 3.677%)

Business Description:

Tower Limited (NZX: TWR) is a New Zealand-based insurance company that operates across New Zealand and the Pacific Islands. It is engaged in providing insurance for houses, cars, content, businesses, and more.

Outlook

The company will continue to build customer relationships through partnerships and lucrative product sets. In addition, it plans to offer an advanced digital experience on one platform for all customers across NZ and the Pacific. In FY22, underlying NPAT excluding large events will be between $35.4-$39.4 million, underlying NPAT will be between $21-$25 million, large events after tax (before tax) will be $14.4 million ($20 million), respectively, and Dividend will be 5 cents per share.

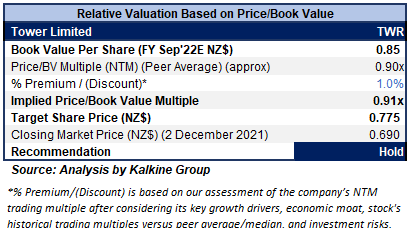

Valuation Methodology: Price/Book Value Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

The stock has been valued using Price/Book Value Per Share multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been assigned to Price/Book Value Per Share Multiple (NTM) (Peer Average), considering the decent performance in FY21 and strong outlook for FY22 driven by modern technological upgradations.

Considering the facts above and the current trading level, we give a “Hold” recommendation on the stock at the closing market price of $0.69 per share, up 1.47% as of 2nd December 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...