Summary:

Introduction

According to TelSoc, telecommunications industry is growing and changing at a rapid pace. In order to keep up with this high pace along with fast-changing technologies, countries require strong legislation as well as an efficient regulatory system. In NZ, the telecommunications industry is broadly divided into 3 categories: 1) Fixed-line infrastructure, 2) Fixed-line retail, and 3) Mobile. This industry has been rapidly growing, and the growth is not only in terms of volume, but also in terms of technology and changing needs. Moving forward, the growth of broader communication sector is expected to be backed by its resilient nature, robust fundamentals, government support, and increased adoption of technology. Key points to consider include:

The broader communication industry in New Zealand also includes media services that are expected to be supported by the robust fundamentals and stable business prospects. Over the long-term, increased investment, support of government policies, higher demand and inclination towards digital tools are expected to act as key growth catalysts. The negative impacts of COVID-19 on the broader industry is expected to get offset by strong government support. Also, it can be said that the communications industry is on the recovery path because of increased adoption of digital tools and ease in lockdown restrictions.

Key Data (Source: NZ Telecommunications Forum)

Currently, New Zealand has close to five million telecommunication connections which facilitate high quality, reliable banking, communication, education, entertainment and more. Looking at the trend, we can safely assume that the demand for data will continue to rise at a faster pace. Digital natives are growing up with technology at fingertips. The IoT is fast becoming a reality, reinventing how we operate to driverless cars capable of safely navigating.

Coverage and Connectivity: Industry on Path to Implement Innovative Processes

The industry is working towards achieving the Government’s updated policy goal of improved broadband and mobile coverage for 99.8 per cent of the population by 2023. This level of new infrastructure build and investment, combined with the unprecedented demand for new connections, has required the industry to implement innovative processes for delivering rural connectivity.

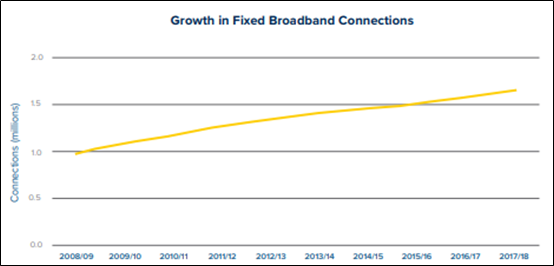

Growth in Fixed Broadband Connections (Source: TCF Annual Reports)

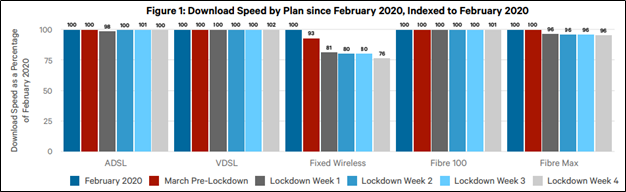

NZ’s Broadband Industry Performed Well During COVID-19 Lockdown

The Commerce Commission’s latest Measuring Broadband New Zealand report shows that, on average, copper and fibre broadband connections experienced no significant decrease in download speeds during the lockdown, despite unprecedented demand on broadband networks.

Download Speed (Source: Commerce Commission New Zealand)

Increased Investment Drives Growth in Telecom Sector

Although the telecommunication sector is privately owned, there are currently large levels of investment from both public and private parties.

However, investment in the telecommunication sector continues to be led by the large investments made by Chorus and Local Fibre Companies. The overall investment in 2019 increased by 2.9% to $1.70 billion.

Government Supports Media Industry Through Tough Times

Government has announced a suite of initiatives valued at $50 million that has been developed with the media industry to help the industry to get through the COVID-19 pandemic.

While media industry has witnessed some negative impacts because of the coronavirus outbreak, the industry is well-positioned on the back of robust business fundamentals, favourable demand scenario and ever-lasting support from the government. As a matter of fact, government is even considering the second support package which might further assist the industry in a speedy recovery.

Key Demand Drivers of Telecommunication Sector: The Road Ahead

The Government has set a goal of improved broadband and mobile coverage for 99.8 percent of the population by 2023. The industry is working towards achieving the Government’s goal by implementing an innovative process for delivering rural connectivity.

Risks Pertaining to Telecommunication Sector

There is active lobbying going on by the section of population worried about the perceived health impacts of Radio Frequency (RF) electromagnetic energy (EME) emissions. As per the report released in November 2018, the Ministry of Health’s Interagency committee on health effect concluded that the existing standards for RF exposure are sufficient for 5G technology.

However, the sector has its own challenges when it comes to providing 99.8 percent connectivity for New Zealand. In order to deliver the services, the fixed-line and mobile network operators have to deal with the plethora of local and territorial authorities for planning and consents. Moreover, the outbreak of coronavirus has impacted the revenues of the industry and has also increased competition in the global landscape.

Since we now have a fair idea of the telecommunications and media sector, it is time to look at the stocks specific to this space (NZM, CNU, VTL, TLS).

1. NZME Limited (NZX: NZM) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit, M-Cap: ~NZ$58.9 Million)

Business Description: NZME Limited is a New Zealand based integrated media company, with a portfolio of market-leading radio, newspaper, digital and magazine titles, with a customer base of 3.3 million kiwis.

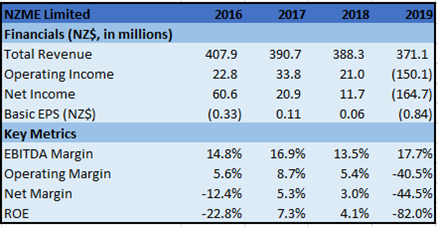

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: While it remains impossible to predict with any accuracy the impact of the pandemic on its full year financial performance, it is anticipated that revenue will be significantly down on the corresponding period in 2019. However, the cost-saving initiatives will partially offset the anticipated revenue declines.

Key Risks: The company is a diversified media company and is subject to different types of risks including, cyber security, legal and regulatory compliance, financial and market, government policy and political, reputation and brand, operational risks, and trading conditions.

Valuation: The company has announced that it has agreed terms to extend the existing debt facilities to July 1, 2023. The new term of bank facilities offers NZM the certainty of funding for next 3 years. In 2019, its net debt fell by $23.6 million to $74.7 million, and the Board is focusing on debt reduction as part of the capital management plan. On TTM basis, EV/Sales multiple stood at 0.6x while industry average is 2.1x. Also, its P/B multiple stood at 0.5x while industry average is 1.9x. Therefore, it looks like the stock is slightly undervalued.

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock in the previous week closed forming Doji candle thereby indicating at indecisiveness on the part of traders. It seems that the on-going week is carrying forward the indecisiveness of the traders which is evident from little to no volatility. On this date of June 25, 2020, the stock has given flattish close. Technical indicator RSI with 50 reading suggests inherent strength in bullish momentum for the stock.

Going forward, the stock is likely to have resistance around $0.35 while support could be around $0.26 as provided by 20 period SMA.

We give a “Speculative Buy” recommendation at the current price of NZ$0.300 per share on June 25, 2020.

2. Chorus Limited (NZX: CNU) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$3.4 Billion, Gross Dividend Yield: 4.306%)

Business Description: Chorus Limited is a provider of phone and broadband services across the network to offer innovative products and services to their customers.

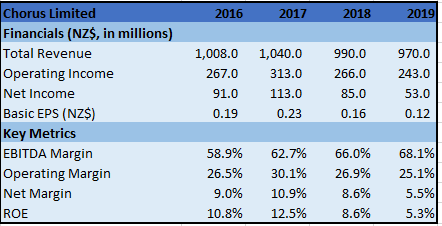

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has increased its FY20 EBITDA guidance to a range of $640 million to $655 million. Earlier, the company provided a range of $625 million to $645 million. The company’s development on improving its business and lowering costs has given it the confidence to raise its FY20 EBITDA guidance. The company has not changed its dividend guidance for FY20 at 24 cents per share.

Key Risks: In the normal course of business, the company is exposed to a variety of financial risks which include the volatility in electricity prices. It has entered into electricity swap contracts to reduce the exposure to electricity spot price movements.

Valuation: The company has also suspended its non-essential field activity to support the Government's objective of eliminating the risks of spreading COVID-19. It has reduced its FY20 gross capital expenditure guidance from a prior range of $660 million to $700 million, to a new range of $610 million to $650 million. We have applied P/CF Based relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms).

P/CF Based Relative Valuation (Illustrative)

.png)

P/CF Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

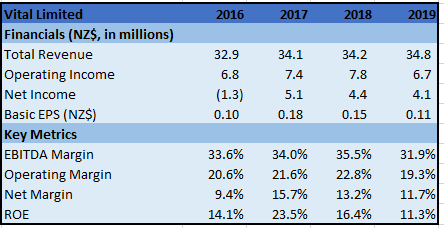

3. Vital Limited (NZX: VTL) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$30.2 Million, Gross Dividend Yield: 5.708%)

Business Description: Vital Limited is the provider of fundamental nationwide infrastructure as well as communication services that are Vital to New Zealand. The company has been offering seamless, connected, integrated communications and coverage in New Zealand’s most remote locations for more than 25 years.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has successfully implemented its Business Continuity Plan and that as a provider of essential services, it was fully operational during the lockdown period. As a provider of critical nationwide communications, the company’s services were essential and were on the list of lifeline utilities. After conducting an immediate assessment of its business, the company has confirmed its EBITDA full-year guidance for FY20 in the range of $14 million to $14.3 million.

Key Risk: The company is exposed to credit risk through the normal trade cycle, advances to third parties and through the use of derivative financial instruments.

Valuation: On TTM basis, EV/Sales multiple stood at 2.1x which is lower than the industry median of 2.3x while its EV/EBITDA multiple stood at 5.8x and the industry median stood at 12.1x. Thus, it can be said that the stock is slightly undervalued at the current juncture.

Technical Analysis:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

In a volatile market condition, the stock has retraced beyond 50% retracement level from its recent low of $0.54. On this date of June 25, 2020, the stock has given flattish at 50% retracement level of $0.73 for the on-going week which suggests that bullish trend for the stock remains intact. Technical indicator RSI with around 49 reading exhibits bullish momentum for the stock.

Going forward, the stock may have resistance around $0.81 while support could be around $0.71 as provided by 20 period SMA. Thus, we give a “Speculative Buy” recommendation at the current price of NZ$0.730 per share on June 25, 2020.

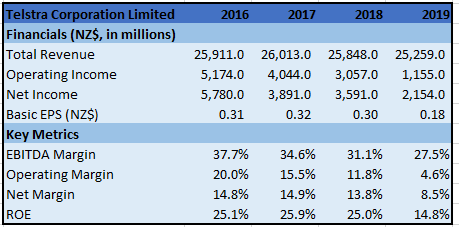

4. Telstra Corporation Limited (NZX: TLS) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$40.2 Billion, Gross Dividend Yield: 4.964%)

Business Description: Telstra Corporation Limited is a telecommunications and technology company that offers a full range of communications services and competing in all telecommunications markets.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: As per the CEO of the company, Mr. Penn, the ultimate impact from COVID-19 on the company difficult to assess at this time. However, based on the information available, the outlook remains within the range of its FY20 guidance. The company’s FY2020 guidance is for up to $500 million growth in the underlying EBITDA (after excluding in-year nbn headwind). The total income is expected to in between $25.3 billion and $27.3 billion.

Key Risks: Telstra operates in an environment that is constantly evolving and facing rapid change. Cyber threats are constantly evolving, including from foreign groups targeting individuals and companies based in Australia and sophisticated phishing scams and cyber-attacks targeting the critical infrastructure that it manages.

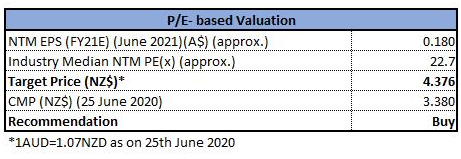

Valuation: The company has also taken certain measures amid COVID-19 pandemic. It has put a hold on any further job reductions. We have applied P/E Based relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms).

P/E Based Relative Valuation (Illustrative)

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...