Sector Landscape

The software services sector is pretty more diversified and advanced. It is also one of the major sectors which is contributing handsomely towards the country’s economic growth. The sector has gained the reputation of being the fastest growing sector in New Zealand. Owing to sustained focus on innovation driven investments in R&D, the sector has developed expertise in various services which includes wireless infrastructure, health IT, digital content, payments, agricultural technology, etc, and thus placed the sector to compete successfully at the global level.

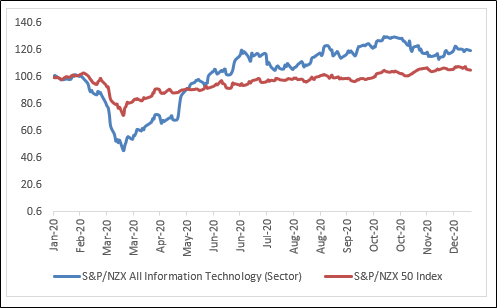

Exhibit 1: S&P/NZX All Information Technology (Sector) v/s S&P/NZX 50 Index (One-Year Chart)*

S&P/NZX All Information Technology (Sector) v/s S&P/NZX 50 Index (Source: S&P Dow Jones Indices)

*Till January 28, 2021

As can be seen from the chart, S&P/NZX All Information Technology (Sector) has outperformed S&P/NZX 50 Index by ~2.25% in the span of past 1 year.

This has also assisted in maintaining the resilient performance of the sector as visible in the Exhibit 2 below. The sector is the 3rd largest export sector of the country and software solutions accounted for one of the highest growth sectors as it logged 20.3% of the country’s overall technology sector growth. Owing to the growing demand of digitisation, this sector has also been one of the major employment generators in the country. It also pays higher wages owing to the requirements of a niche skillset. Thus, the New Zealand software services sector is contributing a pivotal role in the digitisation and diversification of the domestic economy.

Exhibit 2: Performance of The Information Technology Services Sector Stayed Resilient

Data Source: Stats NZ; Chart Created by Kalkine Group

Key Growth Drivers

Some of the key growth drivers for the software services sector have been highlighted below: -

Disruption in FinTech Space

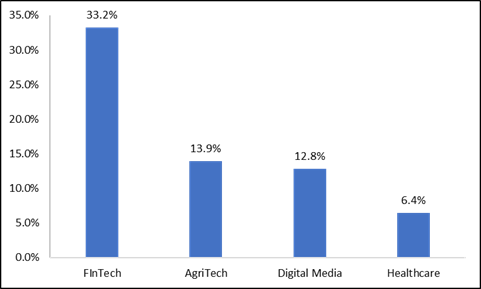

The disruption in New Zealand FinTech’s space is driving the growth of the overall sector of the country as FinTech is the highest growth sector in the technology space . FinTech is powering growth to the country’s overall technology sector with a growth of 33.2%. The acceleration in the FinTech space in the country is primarily driven by heightened investments by the domestic technology companies in order to stay competitive. Further, the supportive regulatory environment of the country which is more business friendly and agile is also powering the growth of the sector as is reflected in Exhibit 3 below.

Exhibit 3: Revenue Growth in Technology Sectors in 2018

Data Source: MBIE; Chart Created by Kalkine Group

To capitalize on the burgeoning opportunities in the FinTech space in the country, the companies in this particular sector remained focus towards constantly redefining the process of financial transactions in the country. This assists in improving the operational efficiencies in the system which helps in staying competitive at the global level.

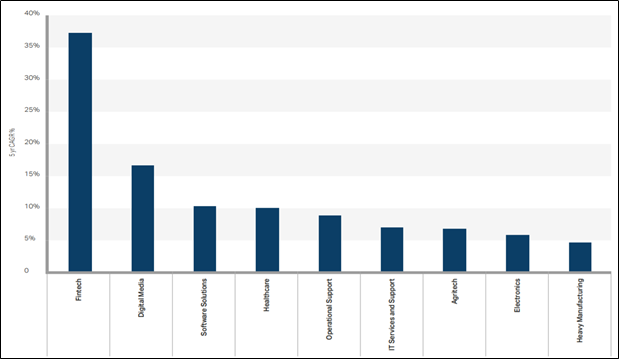

Exhibit 4: Revenue Growth (5 Year 2018 CAGR) of New Zealand's Technology Sectors

Source: MBIE

Supportive Government Strategy

The sustained focus of the government on accelerating the pace of digitisation the flow of government work and services in to become a leading digital nation also powers the demand of software services in the country. In a step towards this direction, the government has outlined a strategy which aimed at attracting better foreign direct investment in areas of competitiveness, encouraging global multinationals to set up R&D hubs in the country by promoting overseas investment in R&D and boosting start-ups. Further, the government has dedicated to increase the spending on R&D to 2% of GDP over 10 years and is also providing tax benefits to technology companies in order to boost a domestic based R&D ecosystem.

Apart from this, continued momentum in embracing the digital technologies viz; IoT and AI technologies, exploiting ICT-enabled opportunities, digital health mission, among others in order to create an integrated or automated government service is also fuelling demand. Resultantly, the supportive government strategy is driving constant innovation in the sector.

Constantly Evolving Disruptive Technologies

In a move to deliver on the government’s vision to become a more productive, sustainable, inclusive, and resilient economy has thrown robust growth potential for the sector. The sector has been witnessing growth momentum in the adoption of digital technologies in the recent past driven by digital disruption due to the rise of advanced technologies viz; the Internet of Things (IoT), artificial intelligence (AI), robotics, among others. This is clear from the decent contribution of the digital technologies to the overall economy as it contributed around $6.5 billion to GDP in 2018. This sector also commands premium wages for the workers as compared to the New Zealand average wage as average pay in the sector stood at $119,442 in 2019 as compared to a country’s average of $59,703.

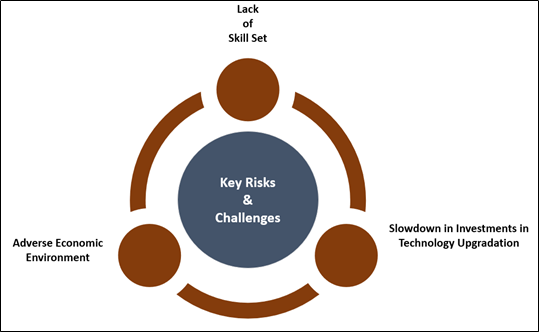

Key Risks and Challenges

Some of the risks attributable to the sector are shown below:-

Exhibit 5: Key Risks and Challenges

Source: Kalkine Group

Lack of Skill Set:

There is a gap in the skill set required in the advanced digital technology space to meet the desired skills required by the industry in the country. In specific, this sector is witnessing a dearth of skills in evolving technology, viz; artificial intelligence (AI). Therefore, the companies in this sector count on immigration to plug the niche skills scarce in the country which poses a greater challenge due to the rapid evolution of advanced technologies. This also increases the cost structure of the companies. However, this can be mitigated by providing relevant advanced digital as well as other technical skills training mandated by the industry at the graduate level. In a step forward, the government has embedded digital technology in its education curriculum since 2019, in an attempt to build the capacity in this space.

Technology Upgradation Mandates Sustained Investments

In order to stay competitive in the global arena, the sector demands constant investment in the digital technology space through R&D by both private players as well as the government. Although, the government is providing investment support through numerous initiatives that include the venture investment fund and the seed co-investment fund, however, the companies in this space often find it difficult in securing investments in order to produce a new wave of opportunities for domestic businesses as New Zealand’s specific early-stage capital markets remained thin. Further, the sustained low availability of venture capital predominantly for Series A and B funding failed to match the demand momentum.

Adverse Economic Environment

The growth of the software services sector of New Zealand is largely hinging on the economic prospects of the country. Adverse macro-economic conditions hinder the investment pipeline of the companies aimed at technology upgradation. So, this will have a contrary impact on the growth momentum of the sector. Resultantly, this will trigger low spending on R&D by technology companies which will hinder in providing a key competitive advantage in the global arena. Constant improvisation of digital technologies through consistent investment on R&D is required to create a niche technology to remain competitive in the world stage.

Outlook

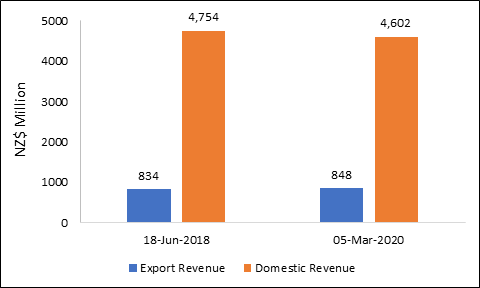

The success of the software services sector has largely been underpinned by the robust technology ecosystem of the country. This entails the benefits of business-friendly environment with a low compliance tax system, the rising level of skilled workforce, healthy start-up environment, support from the government in terms of investments towards R&D to encourage innovation, funding for the creation of required skill set through training, among others. This has led the companies to invest heavily on R&D than any other industry in the country in order to develop niche technology and creation of intellectual property to remain at the edge of innovation. This has resulted in steady growth in the technology export sector of the country which is visible in the Exhibit 6 below.

Going forward, with the economy now gradually recovering from the aftermath of the global pandemic, the usage of accelerated digital technologies is set to play a pivotal role. In addition to this, the advent of 5G technologies also provides robust growth prospects for the sector as a whole as it underpins deeper digital transformation for improvement in virtual reality experiences, driverless cars potential, greater use of robotics and industry automation and internet of things.

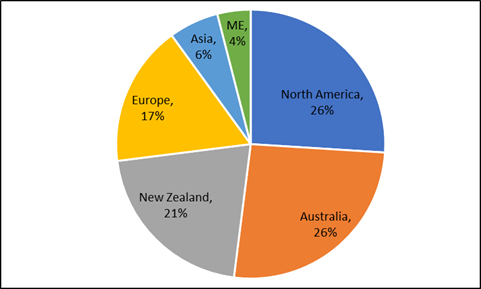

Exhibit 6: Geographical Technology Export Sector’s Growth Percentage in 2018

Data Source: MBIE; Chart Created by Kalkine Group

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

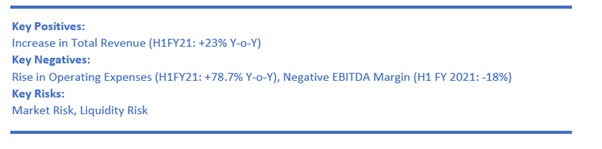

1. Pushpay Holdings Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.7 billion)

Business Description:

Pushpay Holdings Ltd (NZX: PPH) provides a donor management system, including donor tools, finance tools and a custom community app, and a church management system (ChMS) to the faith sector, non-profit organisations and education providers.

Outlook

The company expects further acceleration in revenue growth going forward as it continues to execute on the strategy, achieves better efficiencies as well as enhances further market share in the US faith sector. Driven by healthy liquidity position, the company is exploring additional potential strategic acquisitions that will aid in expanding its current proposition and value to the business. Meanwhile, PPH anticipates EBITDAF for the year ending 31st March 2021 in the range of US$56.0 million and US$60.0 million.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

*% Premium/(Discount) is based on our assessment of the company’s NTM trading multiple after considering its key growth drivers, economic moat, stock's historical trading multiples versus peer average/median, and investment risks.

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied EV/Sales multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to the peer average EV/Sales (NTM Trading multiple) considering the stock's historical discounted trading multiple versus peers, risks associated with higher debt level, stretched valuations of technology sector and higher expenses.

Thus, considering the expected upside and growth in operating revenue, we give a “Buy” rating at the price of $1.580 per share, down by 5.95% on January 28, 2021.

2. Plexure Group Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$193.28 million)

Business Description:

Plexure Group Ltd (NZX: PX1) is engaged in helping brands to build 1:1 relationships with customers at scale.

Technical Overview

Weekly Chart

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock having made a Double Top at $1.60 is on correction path. In the ongoing week, the stock took support around 38.2% retracement level of $1.12. The technical indicator RSI reading of 42 suggests neutral momentum for the stock.

Going forward, the stock may have resistance around the converging point of 23.6% retracement level and 20 periods SMA of $1.30 whereas support could be around the previous low of $1.01.

Outlook

The company is marking significant strides towards new product initiatives and platform updates which will enable it to expand in the key target markets. Besides, the company has provided revenue guidance for FY21 where it expects to garner growth of 14% YoY. However, it expects to post net loss after tax loss of $10 million in FY21. This is due to the impact of investments which the company has undertaken to increase its headcount to support the expansion of its sales and marketing activities, investments targeted towards innovation and upgradation of its platform capacity.

Thus, considering the technical analysis and increase in total revenue, we give a “Buy” rating at the price of NZ$1.120 per share, down by 2.61% on January 28, 2021.

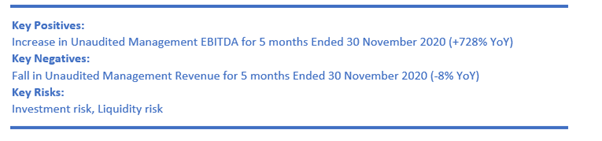

3. Enprise Group Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$16.6 million, Gross Dividend Yield: 1.923%)

Business Description:

Enprise Group Ltd (NZX: ENS) happens to be an investment vehicle for the high-growth tech companies that complement its core ERP capability.

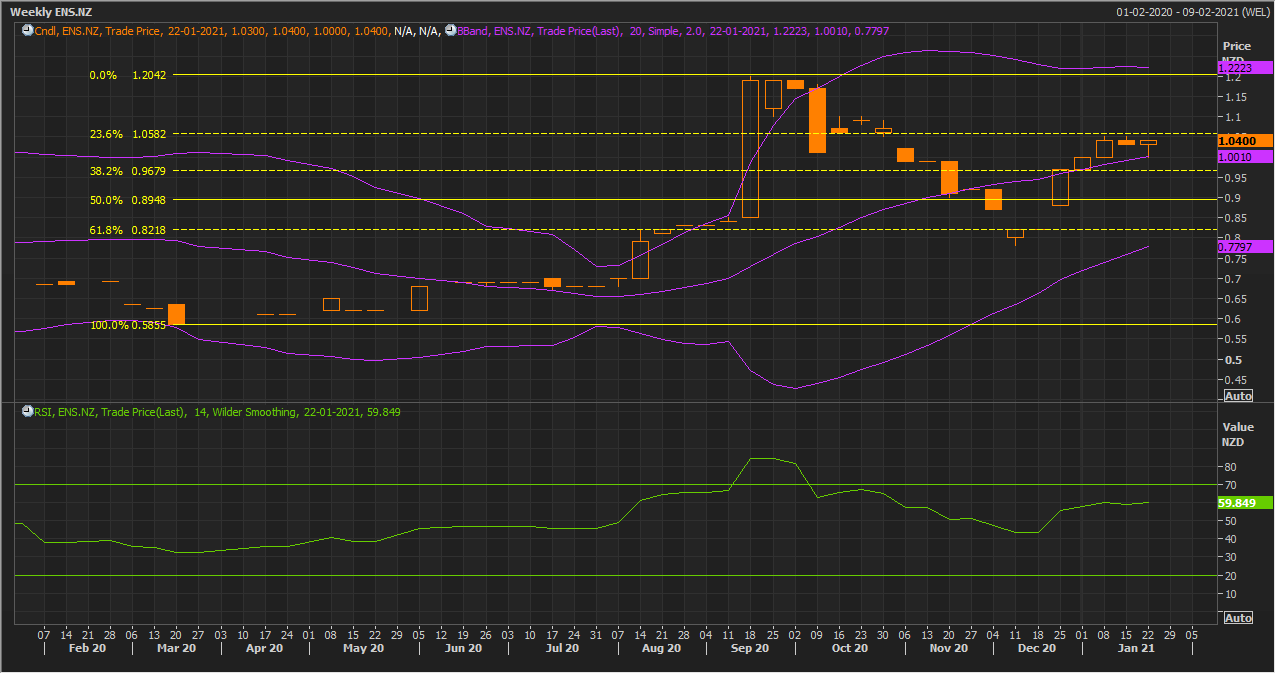

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock having taken support at 20 periods SMA of $1.00, moved up and gave a stronger close at $1.04, forming a ‘Hammer’ on the chart for the ongoing week. The technical indicator RSI with a reading around 60 indicates a strong bullish momentum for the stock.

Going forward, the stock may have resistance around the previous high of $1.20 whereas support could be around $1.00.

Outlook

The company restructured 2 divisions (Enprise Solutions and Kilimanjaro Consulting) into the single Enterprise Division generating cost savings as well as efficiency improvements. Besides, the company has also undertaken a capital raise initiative in May 2020 that resulted in raising $1 million capital which has placed the company in a better position to tap future growth opportunities. As at 30th November 2020, the company had no debt as well as cash reserves of $2.48 million (after increasing the share of iSell from 50 to 67%).

Thus, considering the technical analysis and increase in unaudited management EBITDA for 5 months ended 30 November 2020, we give a “Hold” rating at the price of NZ$1.040 per share on January 28, 2021.

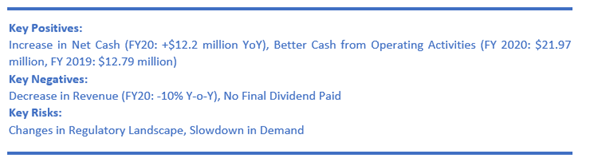

4. Gentrack Group Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$129.22 million)

Business Description:

Gentrack Group Ltd (NZX: GTK) has a history of developing, implementing as well as supporting the specialist software for the energy utilities, water companies as well as airports.

Outlook

Owing to the company’s cost-out programme in March 2020, COVID-19 cost reductions and other savings measures, its costs were down by $3.2 million in H2 FY 2020 (as compared to H1 FY 2020). The robust liquidity position will enable the company to tap better growth opportunities by fast-tracking its technology investment. GTK sees market opportunities as well as it has plans for ongoing investment towards new cloud technology as well as the skills needed to compete.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

.png)

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

*% Premium/(Discount) is based on our assessment of the company’s NTM trading multiple after considering its key growth drivers, economic moat, stock's historical trading multiples versus peer average/median, and investment risks.

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

We have applied EV/Sales multiple Based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to the peer median EV/Sales (NTM Trading multiple) considering the impacts related to COVID-19 as GTK is exposed to the pandemic hit travel sector, while also taking into consideration its historical discounted trading multiple versus peers.

Thus, considering the expected upside and increase in net cash, we give a “Hold” rating at the price of $1.310 per share, up by 0.77% on January 28, 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...