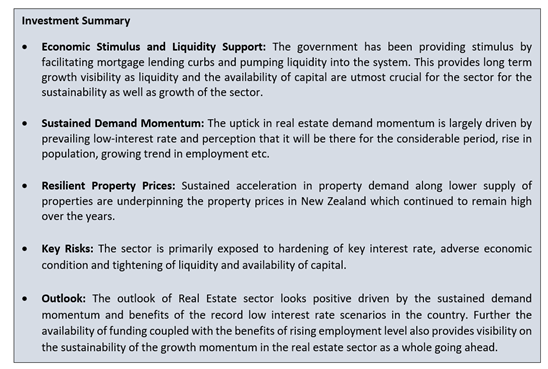

Sector Landscape

The real estate sector is one of the key drivers of the New Zealand economy. New Zealand real estate sector comprises of residential as well as commercial property, among others. The country’s housing sector includes housing types ranging from residential buildings to attached townhouses, apartments, lifestyle blocks (with a dwelling), among others. While, the commercial property encompasses office, retail, industrial buildings, etc. Various key factors have been imbuing momentum in demand in the real estate industry of the country includes; the prevailing low-key interest rates, along with sustained rise in population, growing trend in the employment level in the country, and support from government’s economic stimulus by facilitation of mortgage lending curbs and pumping liquidity into the system.

All these factors are directing the positive trend in the real estate demand in New Zealand. This was underpinned by the property prices in New Zealand which continue to remain at elevated level over the years. Further the lower growth in the supply of properties around the country has also contributed to the higher real estate prices.

Key Growth Drivers

Some of the key growth drivers for the Real Estate sector have been highlighted below: -

Several Government Economic Stimulus and Liquidity Support

The sector has also largely been supported by various economic stimulus measures as well as liquidity support by the government which has resulted in stimulating the economic recovery and consequently the real estate sector as a whole. The government in its budget 2020 announced a massive relief package worth NZ$50 billion which was termed as Covid-19 Response and Recovery Fund. This fund builds on top of the initial $12.1 billion COVID-19 Economic Response Package announced in March 2020, and $12 billion investment fund under New Zealand Upgrade Programme in January 2020. Apart from this the support from the Reserve Bank of the Country in maintaining low key interest rate and providing timely liquidity support to the commercial banks of country also bodes well as Liquidity and availability of capital are of utmost crucial to ensure sustainable growth of the sector.

The surge in the funding and liquidity pumped into the system by the government augurs well for the long-term growth visibility of the sector. Moreover, this has resulted in driving employment generation in the country and in turn buoyed overall demand.

Growing Employment Rate

The growth of the real estate sector in the country has also been largely influenced by the employment level. The rise in employment level directly impacts the income level and consequently contributes to the demand for property in New Zealand. Notably, the December 2020 quarter’s employment figures were encouraging as the seasonally adjusted employment rate increased to 66.8% from 66.4% in the previous quarter. While the number of employed people during the year to December 2020 grew by 19,000. Further, the rebound in the economy along with easing of restrictions in the country and the resumption of business activities have a positive impact on employment generation.

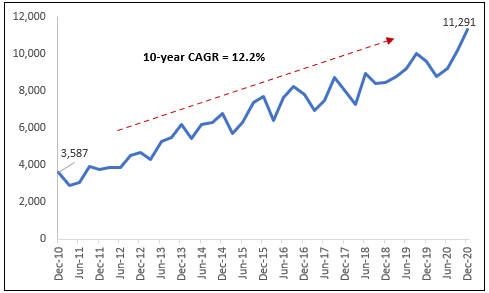

As evidenced below (Exhibit 1), the new homes consented in the December 2020 quarter stood at a record level (11,291). While during the year ended December 2020, the number of new homes consented were 39,420. The spike in new homes consented was powered by new townhouses, flats, and units which accounted for nearly a third of overall figure. They have posted a growth of ~41% in the year ended December 2020 to 11,603 from the year ended December 2019. Moreover, the annual new homes consented for the year ended January 2021 rose 5.8% YoY to reach 39,881.

Exhibit 1: Quarterly Trend in New Homes Consented

Source: Stats NZ; Chart Created by Kalkine Group

While in terms of value, residential consents which accounted for more than 68% of the total value of all consents in 2020 stood at around $16.5 billion during the year ended December 2020. Meanwhile, the consents for multi-unit homes and stand-alone houses witnessed growth of around 11% and 0.5% in value terms in 2020, respectively.

Exhibit 2: Value of Building Consents, By Building Type, Rolling Annuals, December 2010–December 2020

.png)

Source: Stats NZ; Chart Created by Kalkine Group

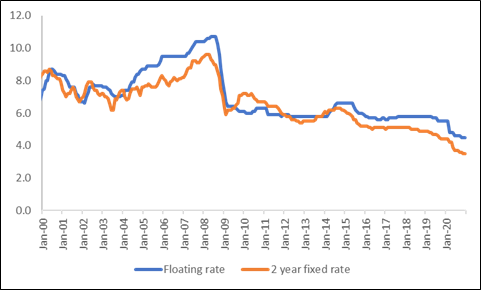

Low Interest Rate Powering Demand

The growth of the real estate sector is also underpinned by the prevailing low interest rate in the country. The Reserve Bank of New Zealand has been maintaining the low Official Cash Rate (OCR) at 0.25% from mid-March 2020. Accordingly, the standard interest rate on new residential mortgage lending also continued to decline across tenors. New Zealand’s floating interest rate on new standard residential mortgage lending also reduced to 4.51% in December 2020 from 5.45% in December 2019. The benefit of low interest rate scenario coupled with the advantage of affordable borrowing is fuelling robust demand scenario in the country which is clearly visible from the decent property transfers activities in the country which stood at 63,999, including 51,504 home transfers in the quarter ended December 2020.

Exhibit 3: Mortgage Rate Trend

Source: RBNZ; Chart Created by Kalkine Group

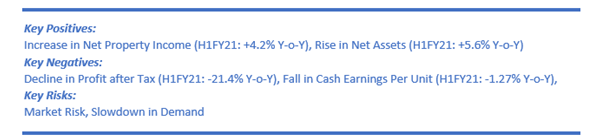

Key Risks and Challenges

Some of the risks attributable to the sector are shown below:-

Exhibit 4: Key Risks and Challenges

Source: Kalkine Group

Outlook

The demand momentum of the real estate sector of the country is largely hinges on numerous factors which comprises of the prevailing record low interest rate scenarios coupled with availability of easy funding as well as increase in population. Apart from this, growing economic growth prospects of the country along with rising employment level also acts as a driving force for the sector altogether. Besides, with the support from government’s economic stimulus by facilitation of mortgage lending curbs and pumping liquidity into the system augurs well for the long-term growth visibility. This opportune scenario has underpinned sustained momentum in demand and has also enticed various first home buyers and investors, thus driving the overall growth of the sector.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

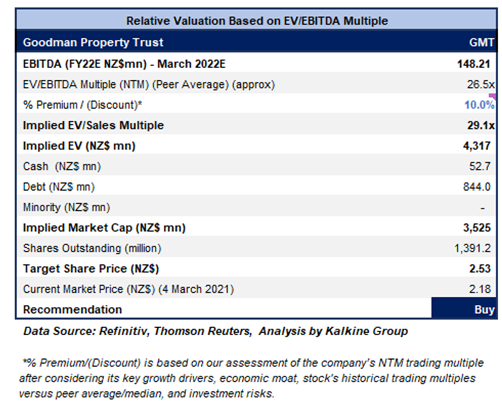

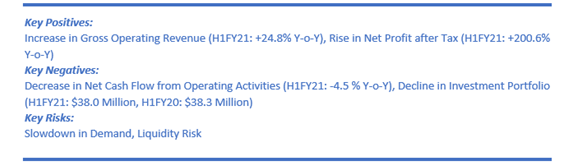

1) Goodman Property Trust (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.026 billion, Gross Dividend Yield: 3.003%)

Business Description:

Goodman Property Trust (NZX: GMT) is engaged in the business of owning, developing, and managing industrial real estate globally which includes logistics facilities, warehouses, and business parks. It has a robust property portfolio of $3.3 billion with 11 properties under management in New Zealand.

Outlook

The company enjoys the benefit of well-capitalised balance sheet which has aided GMT in exploring potential new investment opportunities for growth. Its balance sheet strength was reflected by its loan to value ratio which stood at just 21.5%. Further the benefits of refinancing of bank facility have increased the weighted average debt term to 5.1 years at the end of 30 September 2020 from 4 years as on 31 March 2020. It has also aided in providing $400 million of available funding capacity at the end of 30 September 2020. This will enable the company to tap future investments. Meanwhile, the company expects its FY21 cash earnings per unit to be at least 6.3 cpu on the back of improved favourable economic outlook.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

We have applied an EV/EBITDA multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of double digit (in % terms). We have applied some premium to the peer average EV/EBITDA (NTM Trading Multiple) considering its solid first half operating performance, its well-capitalized balance sheet as well as the strength of its customer relationships and targeted investment strategy.

Considering, the aforesaid facts, current trading levels and upside potential on the stock we give a “Buy” recommendation on the stock at the current price of NZ$2.175 per share, down 1.14% on March 4, 2021.

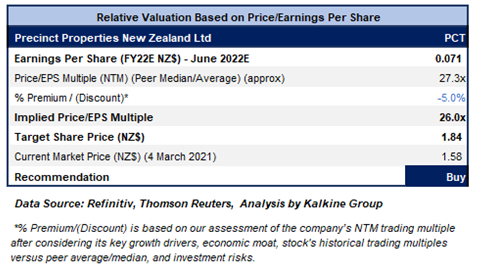

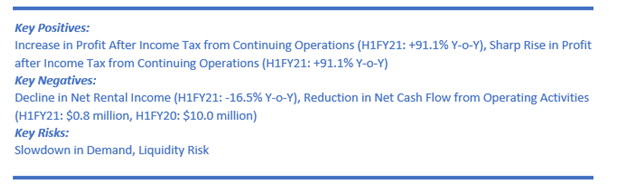

2) Precinct Property Trust (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.075 billion, Gross Dividend Yield: 4.323%)

Business Description:

Precinct Properties New Zealand Ltd (NZX: PCT) is engaged in owning and developing premium inner-city business space in Auckland and Wellington. It holds portfolio value of $3 billion.

Outlook

The company has delivered a strong first half result. Further the balance sheet remained strong with gearing of 29.9% (June 2020: 28.8%). Following the sale of the ANZ Centre for $177 million in the period will aid in reducing the gearing further to around 26%. The management highlighted that the demand is recovering strongly, and outlook is positive. It expects growth to be further driven by its high occupancy levels and a 7.7-year WALT which aids in providing lower leasing costs and incentives. Further, the board has guided to achieve AFFO of 6.50 cps in FY21 and has also provided dividend guidance of 6.50 cps for FY21, an increase of 3.2% YoY.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

We have applied P/E multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of low double digit (in % terms). We have applied a slight discount to the peer average P/E (NTM Trading Multiple) considering uncertainty on AFFO and challenging marketing conditions.

Considering, the aforesaid facts along with decent outlook, current trading levels and upside potential on the stock we give a “Buy” recommendation on the stock at the current price of NZ$1.580 per share, down 1.86% on March 4, 2021.

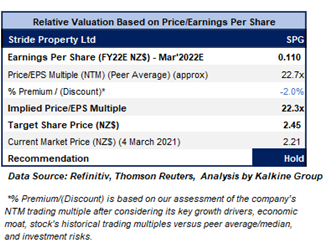

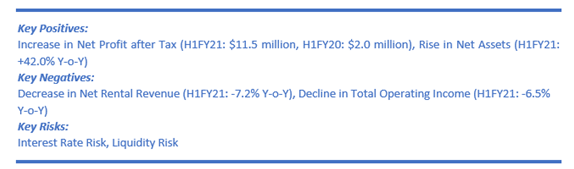

3) Stride Property Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.044 billion, Gross Dividend Yield: 5.553%)

Business Description:

Stride Property Limited (NZX: SPG) comprises of Stride Investment Management Limited (SIML) and Stride Property Limited (SPL). While SPL is engaged in investing in properties across New Zealand, SIML deals in managing real estate investment and is currently managing the properties of SPL, Diversified NZ Property Trust, Investore Property Ltd and in a joint venture company Industre Property Ltd.

Outlook

The company has a healthy cash reserve of $15.6 million at the end of H1FY21. Together with the capital raising initiatives will enable the company in tapping further growth opportunities going ahead. Moreover, it has also managed to secure committed additional 3-year debt facility of $100 million to boost growth. Meanwhile the company is targeting a combined annual cash dividend of 9.91 cents per share for FY21.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

We have applied P/E multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of high double digit (in % terms). We have applied a slight discount to the peer average P/E (NTM Trading Multiple) considering decline in net rental income and increasing cost of debt.

Considering, the robust growth in earnings coupled with healthy liquidity profile, current trading levels and upside potential on the stock we give a “Hold” recommendation on the stock at the current price of NZ$2.210 per share, down 1.78% on March 4, 2021.

4) Asset Plus Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$126.95 million, Gross Dividend Yield: 5.060%)

Business Description:

Asset Plus Limited (NZX: APL) is a listed property investment management company that manages a property portfolio of commercial and industrial buildings in major cities of New Zealand.

Outlook:

The company is focused on the successful execution of the development as well as the leasing of the vacant space of Munroe Lane and 35 Graham Street redevelopment opportunity. The company inked a conditional deed of the lease agreement for the basement and ground floor of 35 Graham Street with Auckland Council for a fixed term from 28 June 2021 to 28 December 2021. Meanwhile the company has received resource consent (for the addition of 3 new levels on the existing office building) for the preferred office development at 35 Graham Street, Auckland CBD. The company is in search for new opportunities as it requires scale to set a stronger platform for growth. In a move towards disposal of non-core assets, the company has recently highlighted the unconditional sale of a non-core asset, the Eastgate Shopping Centre in Christchurch at a price of $43.45 million.

We have applied P/E multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of low double digit (in % terms). We have applied a slight premium to the peer average P/E (NTM Trading Multiple) considering it sustained focus towards tapping growth opportunities and its move towards disposal of non-core assets.

Considering, the stable portfolio occupancy, focus on gaining scale to set a stronger platform for growth, current trading levels, and upside potential on the stock we give a “Hold” recommendation on the stock at the current price of NZ$0.350 per share, up 1.45% on March 4, 2021.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...