.png)

I. Sector Landscape and Outlook

As per the Ministry for Primary Industries (MPI), NZ exports food and primary products to over 200 overseas markets and contributes ~80% of NZ’s exported goods. In addition, MPI plays a vital role in monitoring imported ingredients and products from trading countries. Overall export revenue for FY21 continues to be strong, with just 1.1% decline in FY21, primarily driven by strong farmgate milk prices, bumper avocado and kiwifruit crops, and robust Chinese demand for logs. To boost the exports, the government plans to expand NZ’s market opportunities and provide adequate support to exporters by securing high-quality, comprehensive, and inclusive free trade agreements (FTAs).

The Food Price Index Continue to Rise in September 2021

As per Stats.NZ, the food prices increased by 0.5% in September 2021, while after seasonal adjustment, the index was up 0.9%. This rise was contributed by the increase in meat, poultry, and fish prices by 1.8%, followed by non-alcoholic beverage prices by 1.2%. In addition, grocery food prices increased 0.8% (up 0.7% after seasonal adjustment), and restaurant meals and ready-to-eat food prices rose 0.2%. However, fruit and vegetable prices decreased 1.5% in September 2021 (up 2.3% after seasonal adjustment).

Meanwhile, the food prices grew 4.0% in the year ended September 2021, where fruit and vegetable prices grew 9.3%, followed by restaurant meals and ready-to-eat food prices that grew 4.6%. Further, the meat, poultry, and fish prices rose 3.2%, grocery food prices rose 2.9%, and non-alcoholic beverage prices increased 1.1%.

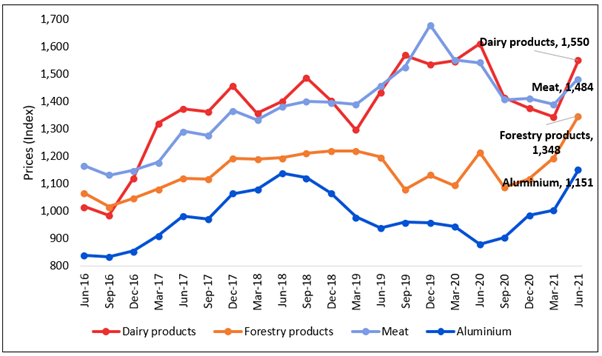

Rising Dairy and Forestry Products Export Prices, Lifts Merchandise Terms of Trade

As per Statst.NZ, the merchandise terms of trade in the June 2021 quarter increased 3.3% QoQ, primarily due to the rise in global commodity prices. Export prices for goods increased 8.3% QoQ, while import prices increased 4.8%. Terms of trade measures NZ’s buying power for import goods, based on the prices it receives for exports. A rise in terms of trade signals that NZ can buy more import goods for the same quantity of exports.

Dairy and forestry products were the prime contributors to increasing goods export prices. Export prices for dairy products rose 15.3% QoQ, while prices for forestry products rose 12.7% QoQ.

Exhibit 1: Selected Exports Price Indexes, June 2016 Quarter – June 2021 Quarter

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Exports Driven by Primary Products in August 2021

As per Stats.NZ, the value of all goods exports stood at $4.4 billion in August 2021, primarily driven by meat and edible offal export, up $109 million (25 %), followed by a rise in logs, wood, and wood articles, up $71 million (18 %). As per MPI, meat and wool export revenue is anticipated to reach $10.4 billion in FY21. However, this revenue target has been revised upward due to higher stock slaughter and export volumes. Further, the forestry export revenue is anticipated to reach $6.3 billion in FY21, up 12.8% YoY, where harvest volumes are expected to reach 36.5 million cubic metres in FY21, up 14.5% YoY.

Exhibit 2: Overseas Merchandise Trade Balance in August 2021

.png)

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

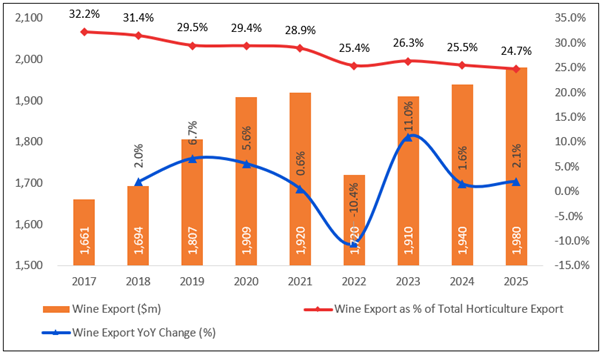

Consumer Demand Expected to Drive Wine Export

As per MPI, the consumer demand for fresh fruit and wine from international markets has retained its winning strength despite COVID-19 related disruptions, which is anticipated to continue further. However, some headwinds are expected in FY22. The top markets for NZ wine are the US (contributing 31% of export), the UK (24%), Australia (21%), the EU-ex UK (11%), and Canada (6%), among others. The export revenue is anticipated to reach $1.9 billion in FY21, up 0.6% YoY. However, poor weather for the 2021 vintage would lead to a significant decline in FY22, with export revenue anticipated to fall 10.4% YoY to $1.7 billion in FY22.

Exhibit 3: Trend in Wine Export Revenue 2017-2025 ($ million)

Data Source: This work is based on/includes the Ministry for Primary Industries data which are licensed under Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 5-year return of ~87.36% versus ~62.82% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~24.54% in 5-year.

Exhibit 4: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

Source: REFINITIV

Key Risks and Challenges:

The primary industry faces the risk of climate change, shortage of migrant workers, intense competition from the international market, food safety, and the overall health benefits of what the buyer purchases and eats. And the premium the buyer pays for the quality of the product in the domestic and international market. Moreover, the global consumers in the high-value segments of markets have rising expectations, putting pressure on producers and suppliers for high-quality products.

The alcohol industry is competing to make its presence in online sales to reach a more extensive consumer base, like other booming online industries. While few alcohol brands have made their presence felt online, others have learned that it needs to create strategic partnerships.

Exhibit 5. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per MPI, the dairy export revenue is anticipated to fall 5.4% to $19.0 billion in FY21 due to COVID-19 related circumstances and an appreciation of the NZ dollar (NZD). Milk production for the FY21 season is anticipated to grow 1.9%, supported by favourable weather conditions and a solid farmgate milk price. Further, the forestry export revenue is expected to hit $6.3 billion in FY21, up 12.8% YoY. Harvest volumes are estimated to hit 36.5 million cubic metres in FY21, up 14.5% YoY. Log export volumes are anticipated to rise 21.4%, reflecting increased demand for export logs.

Further, the horticulture revenue is expected to rise 2.3% in FY21 to $6.6 billion due to larger crops and kiwifruit and avocados export volumes. Overall, the wine industry is expected to continue expanding. Demand in the top four export markets (US, UK, Australia, and the EU), which contribute ~87% of NZ’s wine exports, has increased despite the impacts of the pandemic.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Fonterra Co-operative Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit (M-Cap: NZ$5.11 billion, Gross Dividend Yield: 6.39%)

Business Description:

Fonterra Co-operative Group Limited (NZX: FCG) is a New Zealand-based farmer-owned dairy cooperative company. The dairy ingredients are sold under the NZMP brand. The company also manufactures, markets, and distributes consumer products.

Outlook:

As per the annual report released on 26 August 2021, the company is confident of its sound fundamentals and relevant growth opportunities in core markets. Primarily, it is focused on divesting its integrated investment in Chile, comprising Soprole and Prolesur engaged in sourcing milk and manufacturing products in Southern Chile. Further, the company is also analysing the ownership structure for Fonterra Australia. One option includes an IPO to retain a significant stake.

Moreover, the company has outlined four key value targets to achieve by 2030. (1) An average Farmgate Milk Price range of $6.50-$7.50 per kgMS; (2) A 40-50% rise in operating profit from FY21, decreased interest, followed by 75% increase in earnings, to increase dividends to ~40-45 cents per share by FY30; (3) Return on Capital of 9-10%, up from 6.6% in FY21; (4) An intended return of about $1 billion to shareholders and unitholders by FY24, and around $2 billion of additional capital generation. This is in addition to ~$2 billion to be invested in sustainability and moving the milk into higher-margin products.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

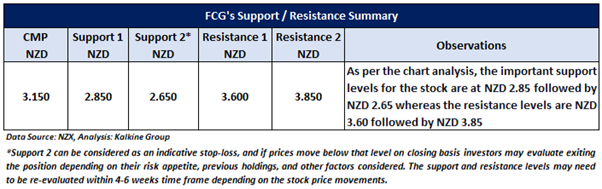

Stock Recommendation

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $3.15 per share (New Zealand Time: 1:23 PM (GMT +12) as of 21st October 2021.

2) Synlait Milk Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$830.61 million)

Business Description:

Synlait Milk Limited (NZX: SML) is a producer and seller of nutritional milk products for its global customers by combining expert farming with state-of-the-art processing.

Outlook

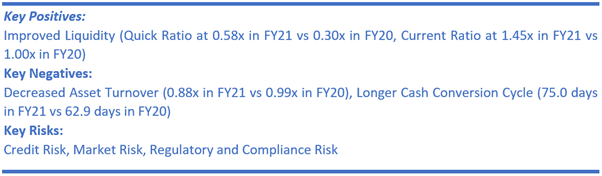

The company forecasts its net profit after tax to rebound in FY22, primarily led by a return to normal trading conditions and robust management of its Ingredient business. In line with this, better infant base powder volumes, higher contribution from its Liquids and Consumer Foods business units, and cost savings from Synlait, Dairyworks and Talbot Forest Cheese. The FY22 will also include a one-off gain on selling ~$17 million of the land and building at Synlait Auckland. Further, its performance will build into FY23 as its new multinational customer at Synlait Pokeno strengthens, and its Liquids and Consumer Foods businesses continue to boom. By the closing of FY23, the company's recovery plan would see Synlait return to similar levels of profitability, operating cash flows, and debt ratios as the years leading into FY21.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

.png)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight discount has been applied to P/E Multiple (NTM) (Peer Average), considering a decrease in gross margin and EBITDA margin at 4.9% and 2.8% in FY21 versus 15.6% and 13.2% in FY20, respectively.

For the purposes of relative valuation, we have taken peers like Sanford Ltd. (SAN.NZ), The a2 Milk Company Ltd. (ATM.NZ), and New Zealand King Salmon Investments Ltd. (NZK.NZ).

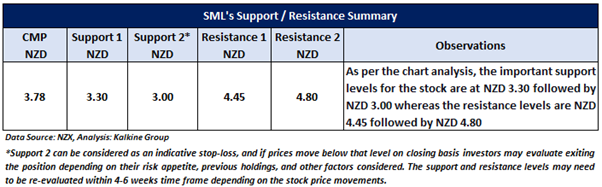

Considering the aforesaid facts, we give a “Speculative Buy” recommendation on the stock at the current market price of $3.78 per share (New Zealand Time: 5:05 PM (GMT +12) as of 21st October 2021.

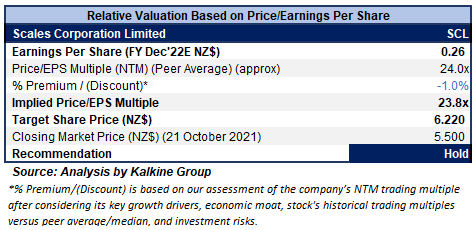

3) Scales Corporation Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$783.17 million, Gross Dividend Yield: 4.807%)

Business Description:

Scales Corporation Limited (NZX: SCL) is engaged in the agri-business. It operates in three divisions that include, horticulture, logistics, and food ingredients, in adjacent primary sectors.

Outlook

The company has upgraded FY21 guidance, primarily driven by H1FY21 solid results. As a result, underlying Net Profit is forecasted to be in the range of $32.0-$37.0 million, implying an Underlying EBITDA in the range of $65.0-$72.0 million. Broadly, the company continues to anticipate disruptions in domestic and international operations, including labour shortage and supply chains due to COVID-19 related circumstances. However, the company is confident in its diversified focus, which would mitigate some limitations due to COVID-19.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight discount has been applied to P/E Multiple (NTM) (Peer Average), considering a lower gross margin at 29.3% in H1FY21 versus the industry median of 38.7% and a reduced fixed asset turnover at 0.97x in H1FY21 vs 1.04x in H1FY20.

For the purposes of relative valuation, we have taken peers like Sanford Ltd. (SAN.NZ), The a2 Milk Company Ltd. (ATM.NZ), and New Zealand King Salmon Investments Ltd. (NZK.NZ).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the closing market price of $5.50 per share, up 0.18%, as of 21st October 2021.

4) Allied Farmers Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$18.44 million, Gross Dividend Yield: 2.564%)

Business Description:

Allied Farmers Limited (NZX: ALF) operates through its subsidiary, NZ Farmers Livestock Ltd, Farmers Meat Export Ltd, and NZ Farmers Livestock Finance Ltd whereby its activities involve the sale of livestock agencies services, the procurement, and processing of calves, and livestock financing.

Outlook

The company plans to deepen its presence domestically, with ongoing digital innovation and relevant further yard accesses. This includes further strengthening livestock transport coordination, effort to decrease the documentation and process requirements in livestock sale and purchase, ongoing strategy to better provide information to prospective purchasers, and app-based access to online client account history.

Moreover, the company reported an audited net profit before tax for FY21 of $2.481 million (FY20 $1.099 million), primarily driven by improved performance from livestock agency business which rebounded from the prior year impacts of Covid and drought.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the closing market price of $0.64 per share, down 1.54% as of 21st October 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...