Sector Landscape

The country’s industrial sector comprises construction, manufacturing, mining & quarrying, and electricity generation. To sail through the adverse impact of the Covid-19, the government has announced various funding as well as liquidity measures to support the economy as well boost the industrial performance. This has led to a robust demand environment led by an uptick in consumer spending. The government in its budget 2020 announced a massive relief package worth NZ$50 billion which was termed as Covid-19 Response and Recovery Fund. This fund builds on top of an initial $12.1 Billion package, and $12.0 Billion investment fund under New Zealand Upgrade Programme in January 2020. The government is providing funding and pumping liquidity into the system, which augurs well for the long-term growth visibility of the sector.

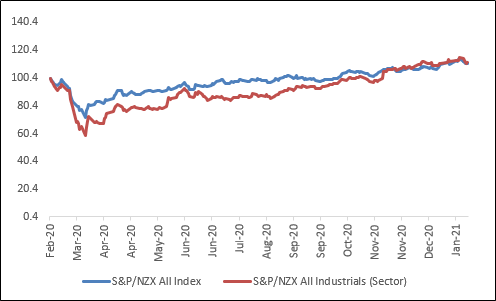

As depicted below, S&P/NZX All Industrials (Sector) outperformed S&P/NZX All Index by 7.34% over the past one year ending 25 February 2021.

Exhibit 1: S&P/NZX All Industrials (Sector) v/s S&P/NZX All Index (One-Year Chart) *

*Till February 25, 2021

Data Source: S&P Dow Jones Indices, Chart Created by Kalkine Group

Key Growth Drivers

Some of the key growth drivers for the Industrial sector have been highlighted below: -

Rebound in Economic Activities

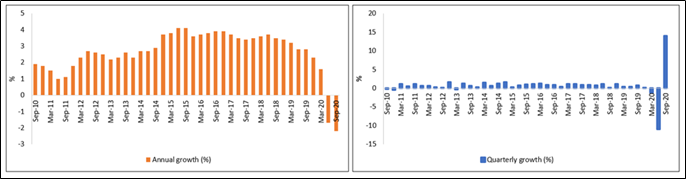

The growth prospects of the economy largely hinge on the growth of the industrial sector . New Zealand Gross domestic product (GDP) witnessed a significant growth of 14% in the September 2020 quarter as compared to a revised 11% decline in GDP in the June 2020 quarter (as the prevailing Covid-19 pandemic has taken a toll on the global economy). The rebound in economic activity in the September quarter can be attributed to the rebound in the manufacturing industry’s performance. After witnessing a sharp decline in activity in the June quarter, industries witnessed larger rebounds in activity in the September 2020 quarter.

Exhibit 2: Gross Domestic Product, Quarterly and Annual Growth Rates

Source: Stats NZ; Chart Created by Kalkine Group

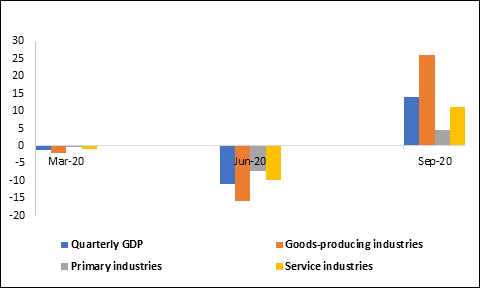

The growth in GDP in the September 2020 quarter was supported by a growth of 11.1% in the service industries which accounted for about two-thirds of the economy. While, goods-producing industries, which contributed about one-fifth of the economy, posted a growth of 26% during the period and primary industries grew 4.6%. The industrial sector accounted for majority of the quarterly growth and this was driven by retail trade and accommodation which registered a growth of 42.8% followed by construction (52.4%) and manufacturing (17.2%).

Exhibit 3: Growth by Industry Group, March – September 2020 Quarters (%)

Source: Stats NZ; Analysis by Kalkine Group

Uptick in Household Spending

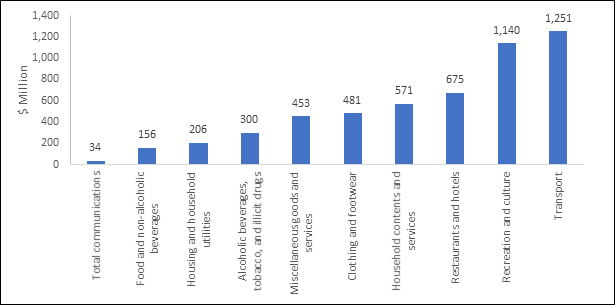

The industrial sector of the country was also driven by the movement in household spending. The country’s household spending showed improvement in the September 2020 quarter as it grew by 14.8% driven by growth across all expenditure categories, paints a rosy picture on the growing visibility of the sector. The momentum in household spending during the quarter was fueled by durables, non-durables, and services industries which accounted for a major share during the quarter. The growth in household spending within the durable goods category was contributed by new and used vehicles and audio-visual equipment. While in the services space the household, spending was driven by a significant acceleration in spending across restaurants and ready-to-eat meals and domestic air passenger services. These services witnessed significant declines in the June 2020 quarter. The uptick in household spending will brighten the growth prospects of the sector, going forward.

Exhibit 4: Change in Household Consumption Expenditure from June 2020 to September 2020 Quarter

Data Source: Stats NZ; Chart Created by Kalkine Group

Rebound in Trading Activities

The growth in the country’s industrial sector has also been driven by the surge in trading activities. The rebound in the trade activities in the country from the adverse impact of the Covid-19 has painted a bright prospect going ahead. This is clear from the uptick in the imports of goods and services in the September 2020 quarter which logged a growth of 10.6% driven by a 16.2% increase in imports of goods. Acceleration in demand for primary fuels and lubricants coupled with higher imports of capital goods and consumption goods have aided to the momentum in import activities during the quarter. Apart from this, the exports of goods and services from the country also recorded an increase of 4.9% in the September 2020 quarter led by a 6.4% rise in goods exports which included metal products, machinery, and equipment; agriculture and fishing primary products; meat products; and forestry primary products.

Besides, the opening of the economy and easing of border restrictions has resulted in the resumption of travel, movement of cargo and global supply chain which augurs well for growth prospects of the sector.

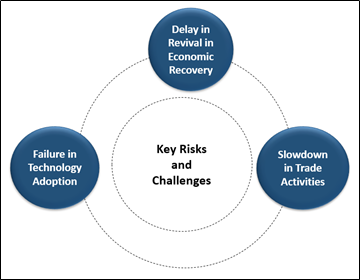

Key Risks and Challenges

Some of the risks attributable to the sector are shown below: -

Exhibit 5: Key Risks and Challenges

Source: Analysis by Kalkine Group

Outlook

The industrial sector of the country was weighed down by the adverse impact of the Covid-19 in 2020 due to dampened business sentiments, increased trade restrictions, and a slowdown in household spending. However, with the rebound in the economy along with easing of restrictions and traction in the household spending, the industrial sector is likely to rebound at a faster pace as these would ultimately result in an uptick in business sentiments and would further propel trade activities. This is evident from the uptick in the country’s exports and imports data in the September 2020 quarter which logged a growth of 4.9% and 10.6% respectively. Besides, the country’s household spending has gathered momentum in the September 2020 quarter as it recorded a growth of 14.8% driven by growth across all expenditure categories. Thus, the long-term outlook of the sector looks buoyant.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

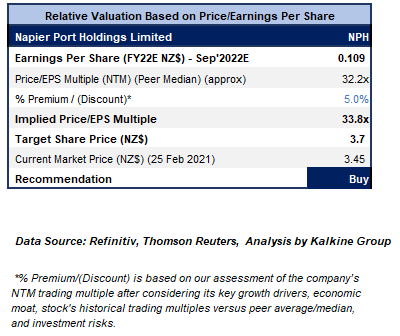

1. Napier Port Holdings Ltd (Recommendation: Buy, Potential Upside: High Single-Digit) (M-Cap: NZ$689.572 million, Gross Dividend Yield: 2.092%)

Business Description:

Napier Port Holdings Ltd (NZX: NPH) is the shipping gateway that connects the centre of NZ with the people as well as markets of the world.

Outlook

NPH has delivered a resilient performance for the full year ended September 2020 as decline in trade volumes was offset by higher average revenue per unit across bulk & containers. The company is maintaining a cautious perspective while it continues to pursue strategic initiatives. It also stated that opportunities in the national supply chain is expected to grow trade volume. Sentiment amongst customers appears to be positive, particularly in meat and forest products sectors.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to P/E multiple (NTM) peer median considering the recovery across the regional primary sector trade base and improvement in regional economic activity.

Considering the expected upside and improvement in EBITDA margin, we give a “Buy” recommendation on the stock at the current market price of NZ$3.45 per share, up by 3.92% on February 25, 2021.

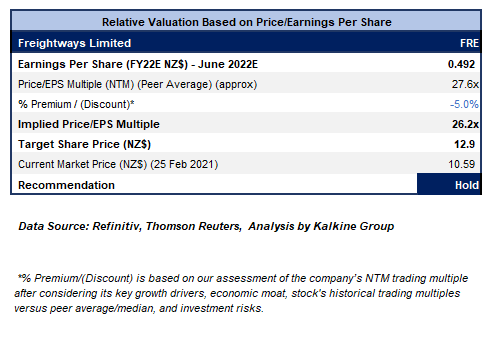

2. Freightways Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.7 billion, Gross Dividend Yield: 1.975%)

Business Description:

Freightways Ltd (NZX: FRE) has expanded from core express package and business mail services into information management, building a diverse selection of digital as well as physical brands in ANZ.

Outlook

The company has delivered strong trade in the express package business while its information management business showed resilient performance in H1FY21. The company has earmarked its FY21 capital expenditure to be spent on IT development projects, replacement of vehicles as well as freight handling equipment. FRE is expecting its capex to stay in a range of $20-22 million in FY21. The company would continue to consider growth or acquisition opportunities which may be complementary to the existing operations as well as capabilities.

Valuation Methodology: P/E Based Relative Valuation (Illustrative)

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/E multiple (NTM) peer average considering that in Express Package, existing B2B volume might be influenced by the macro-economic activity and in information management, activity-based revenue streams would be driven by the number of people returning to office environments, which could be lower than pre-COVID-19.

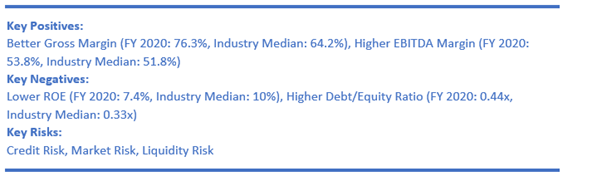

Considering the fall in debt/equity ratio and expected upside, we give a “Hold” recommendation on the stock at the current price of NZ$10.59 per share, 0.38% on February 25, 2021.

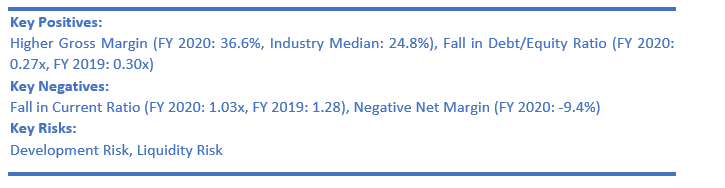

3. Scott Technology Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$165.236 million)

Business Description:

Scott Technology Ltd (NZX: SCT) is engaged in the designing and manufacturing of advanced automation systems.

.png)

Outlook

The company stated that some deferred as well as delayed projects are now coming back online, and demand is gaining traction in some regions as well as sectors.

With the new 5-year strategy, SCT has been able to focus towards the areas of expertise as well as continued innovation in order to drive growth as well as margins while reducing the risk.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

After making ‘Double Top’ at the high of $2.42, the stock has been sliding but with low magnitude. The technical indicator RSI with a reading around 53 and a curve at the end pointing down, suggests the softening of bullish momentum.

Going forward, the stock may have resistance around $2.30 whereas support could be around the 23.6% retracement level of $2.04.

Considering the technical analysis and higher gross margin, we give a “Hold” recommendation on the stock at the current market price of NZ$2.110 per share, up by 0.48% on February 25, 2021.

4. TIL Logistics Group Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$90.315 million)

Business Description:

TIL is one of NZ’s leading private domestic freight as well as logistics platforms. The company possesses a nationwide network of branches, depots and warehouses.

Outlook:

The company stated that current environment reflected the benefits of scale as well as diversity, with the ability to invest towards health & safety, training, systems and infrastructure. Even though the economic conditions are volatile, private and public investment, as well as consumer demand, is anticipated to drive demand in the certain sectors.

The company would be focusing towards strategic priorities in the H2 FY 2021. The Board has confirmed the earlier guidance that EBITDA for FY 2021 is anticipated to be at least that of the FY 2020 post IFRS-16 result of $57.4 million.

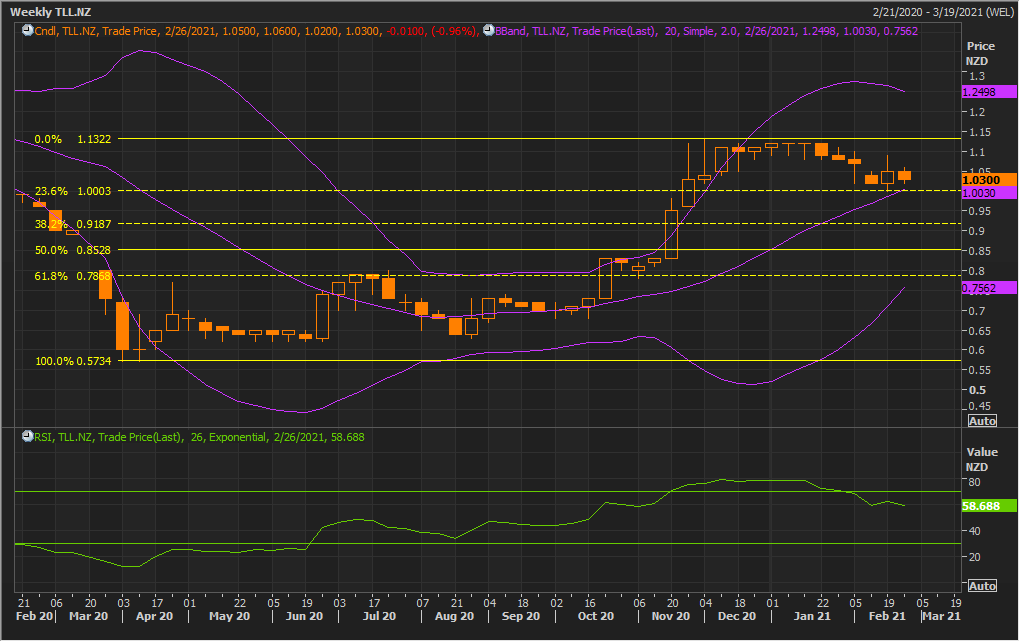

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has largely been consolidating in the range provided by the previous high of $1.13 on the upside and 23.6% retracement level of $1.00 on the downside. The technical indicator RSI with a reading around 59 suggests bullish momentum for the stock.

Going forward, the stock may have resistance around the previous high of $1.13 whereas support could be around the converging point of 23.6% retracement level and 20 periods SMA of $1.00.

Considering the technical analysis and better gross margin, we give a “Hold” recommendation on the stock at the current price of NZ$1.030 per share, down by 0.96% on February 25, 2021.

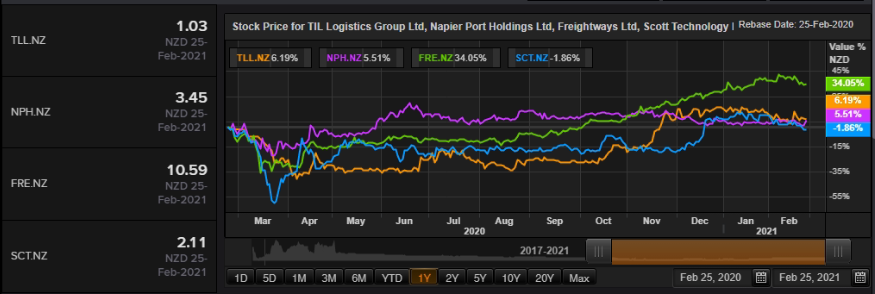

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...