Sector Landscape

New Zealand healthcare sector encompasses public, private and voluntary sectors which offer quality care. The country’s healthcare system is diverse and is largely government-funded as it accounts for 83% of the overall healthcare spend in the country and provides highly subsidized healthcare services to the residents of the country through a network of 20 District Health Boards (DHBs). Overall, the country has around 220 hospitals which are spread across regions.

The healthcare sector is one of the major drivers of the country’s gross domestic product (GDP), enabling the government to spend more on the healthcare system which hovers around 10% of GDP and is marginally higher than the OECD average. As per the data from Statista, the New Zealand healthcare and social assistance industry witnessed a steady rise since 2014 and it accounted for around NZ$14.8 billion of GDP for the year ended March 2020.

New Zealand’s healthcare system offers various job opportunities for healthcare professionals in various disciplines. The public healthcare system offers essential healthcare services that include emergency care, essential surgery, and hospital care free of costs not only to the residents of the country but also to the people staying on a work visa valid for two years or longer. However, costs on a private visit to the general practitioners (family doctors) are to be borne by the individuals. Private healthcare provides services like recuperative care, elective procedures, and a range of general surgical procedures (excluding Accident and Emergency care) in private hospitals. Private healthcare also indulges in offering private radiology clinics and testing laboratories.

Exhibit 1: S&P/NZX All Health Care (Sector) v/s S&P/NZX All Index (One-Year Chart)

.png)

Key Growth Drivers

Some of the key growth drivers for the Healthcare sector have been highlighted below: -

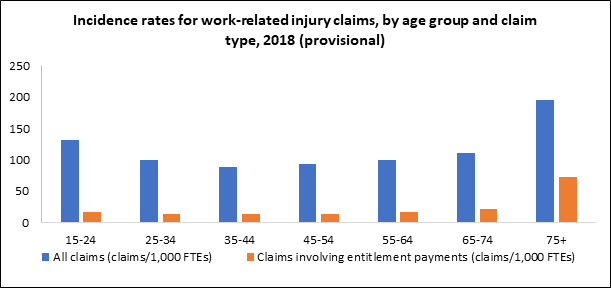

Exhibit 2: Incidence Rates for Work-Related Injury Claims

Source: Stats NZ; Chart Created by Kalkine Group

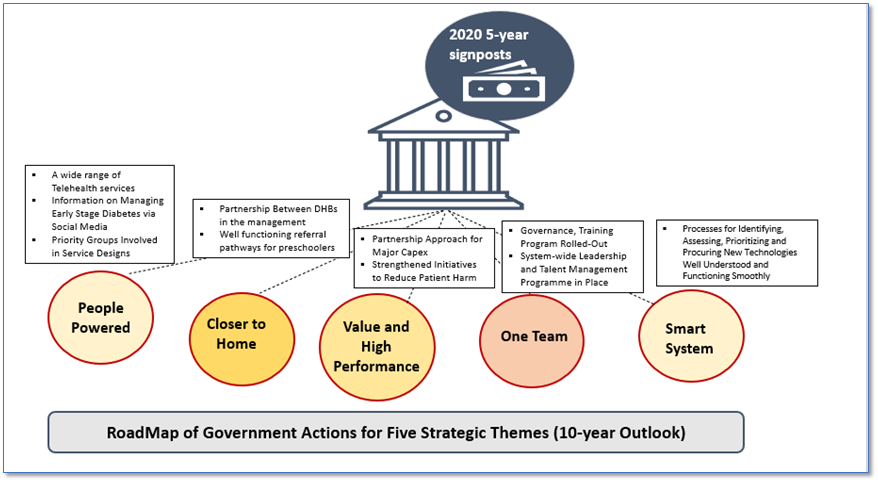

The Government’s roadmap includes the five strategic themes that are bought into action for Future Direction and focus areas over the next five years. The exhibit below indicates some of the expected results from such actions.

Exhibit 3: Possible Results From Implementation of Government’s RoadMap of Actions Over Time

Source: Health.gov.nz; Chart Created by Kalkine Group

Growing Demand of Digital Health Technology

New Zealand government continues to pursue the strategy of leveraging the potential of technologies for healthcare to meet changing needs and to support a strong, equitable public health and disability system. The government has developed a Digital Health Strategic Framework which emphasizes on usage of digital technologies and data to provide better healthcare services . It also helps in boosting the performance of the public health system, assists in making informed decisions , among others. Further, digital health aid in boosting or maintaining the value of the services delivered by the healthcare service providers within available public health funding.

The world of technology has been advancing at a rapid pace which affects operating environment of several sectors. The healthcare services in New Zealand are also following the global trend of embracing emerging technologies which could act as a catalyst to rapid growth in the sector. Increased government support and advanced technological ecosystem could be of great help in this direction. Notably, usage of the technology optimises people’s navigation of the collaborative care system as well as the choices they make. Technology and real-time data helps in driving rapid improvement and change.

Rising Health Awareness Driving Demand for Smart Care

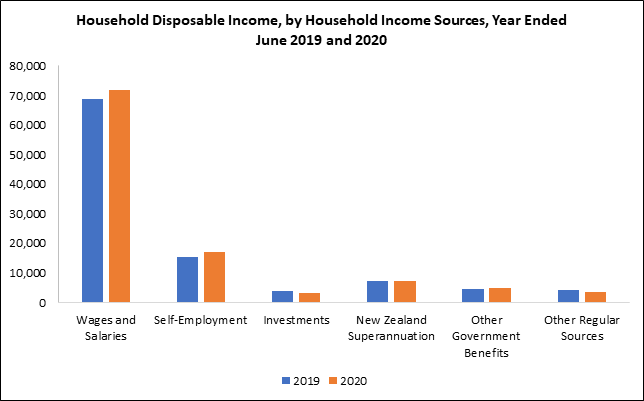

The healthcare sector in NZ is experiencing rapid growth on the back of increased health-consciousness, rising disposable income, and growing population. The improvement in economic growth prospects of the country will further aid in buoyancy for better healthcare services demand. This was further evidenced by the uptick in New Zealand’s Real gross national disposable income (RGNDI), which measures the real purchasing power of the country which registered a growth of 13.9% in the September 2020 quarter.

The below mentioned chart reflects the household disposable income of New Zealand Population.

Exhibit 4: Household Disposable Income Trend

Source: Stats NZ; Chart Created by Kalkine Group

Ageing Population

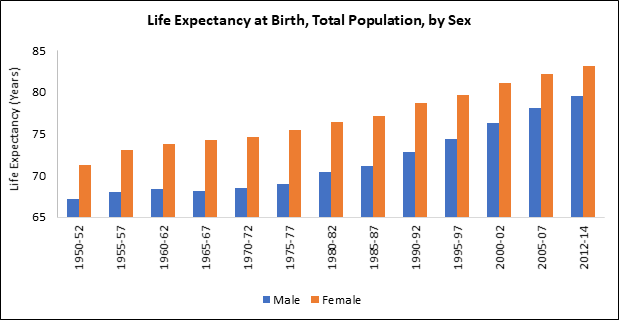

The healthcare sector of the country is also largely driven by ageing population as the New Zealanders are living longer with aged over 65 years. This mandates higher quality healthcare system which caters to the needs of the ageing population as they are more vulnerable to illness. Further, the growing incidence chronic disease among ageing population and the need to deal with these conditions requires a health system that can provide affordable services and assist the older persons to stay healthy and live longer.

Exhibit 5: Life Expectancy Statistics

Source: Stats NZ; Chart Created by Kalkine Group

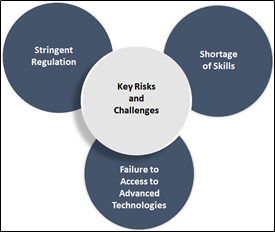

Key Risks and Challenges

Some of the risks attributable to the sector are shown below:-

Exhibit 6: Key Risks and Challenges

Source: Kalkine Group

Outlook

A diverse healthcare system which is universal in nature and is more inclined towards primary care and wellness reflects on the strength of the country’s healthcare sector. The benefits of the country’s unique public health and no-fault accident compensation system, which covers the whole demography through-out their lifespan, also provides visibility on the sustainability of the growth momentum of the sector. Moreover, the government has been pursuing the strategy of leveraging the potential of technologies in healthcare. The government has developed a Digital Health Strategic Framework which emphasizes on usage of digital technologies and data.

Besides, new regulations that will aid the growth in sector and also ensure smooth functioning for patients include the extension of the transitional medicinal cannabis by six months to 30 September 2021, driven by COVID-19, to make sure the regular supply, as per the Health Minister Andrew Little as on March 11, 2021. The government has developed robust plans for COVID-19 vaccination with a strong focus on protecting Māorias per the Associate Minister for Health (Māori) Hon Peeni Henare. Moreover, the strong government support is also visible from the fact that the Ministry of Health funds $8.7 million for 86 cochlear implants each year, while also provides around $25million fund each year to support over 23,000 people to access hearing aids.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

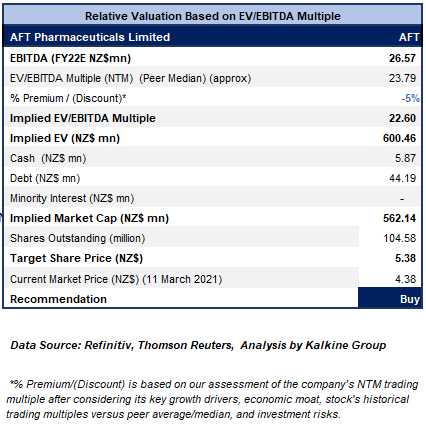

1) AFT Pharmaceuticals Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$458.077 million)

Business Description: AFT Pharmaceuticals Ltd (NZX: AFT) happens to be a growing multinational pharmaceutical company that is engaged in developing, marketing and distributing a broad portfolio of the pharmaceutical products throughout a wide range of therapeutic categories that are distributed throughout all the major pharmaceutical distribution channels: over-the-counter, prescription and hospital.

Outlook

AFT has delivered a decent performance in the face of challenging market conditions. The performance was further aided by its strategy not only to augment its presence in the key markets of Australia, New Zealand and Asia but also to enhance its international revenues through the out licensing of the intellectual property. Additionally, the refinancing of the debt and the $12 million in new capital raise have reinforced the company’s position to continue to grow shareholder value.

The revenue growth momentum is expected to increase with the recent signing of agreements and distribution deals, launching of new products and the great efficacy that the Crystawash Extend hand sanitiser has displayed.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

We have applied EV/EBITDA based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to EV/EBITDA multiple (NTM) peer median considering the company's exposure to changes in foreign exchange rates on assets and liabilities of subsidiaries, as well as USD denominated borrowings.

Considering the expected upside and rise in operating revenue, we give a “Buy” at NZ$4.38 per share, up by 0.69% on March 11, 2021.

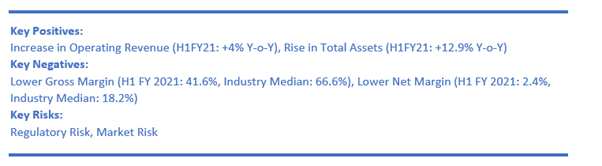

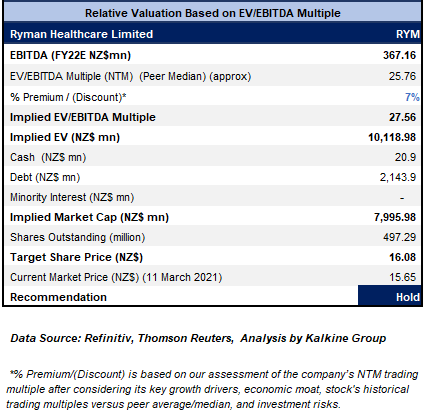

2) Ryman Healthcare Ltd (Recommendation: Hold, Potential Upside: Low Single-Digit) (M-Cap: NZ$7.8 billion, Gross Dividend Yield: 1.393%)

Business Description:

Ryman Healthcare Ltd (NZX: RYM) happens to be the largest provider of retirement living options for the New Zealanders.

Outlook

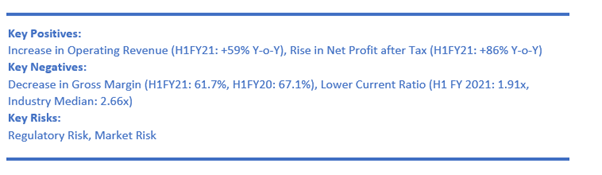

It continued to witness strong demand for aged care in New Zealand and Victoria with mature care occupancy at 97%. RYM anticipates cash collections of $275 million from new sales in the second half, up from $118 million in the second half of last year.s The company is witnessing lot of pent-up demand in the housing market and it is in a good position to continue to invest heavily in new homes and jobs.

The company stated that only 1.9% of the retirement village portfolio was available for the resale at 30th September. Besides, it has a robust balance sheet which will aid in tapping growth opportunities.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

Considering the expected upside and rise in total assets, we give a “Hold” rating at NZ$15.65 per share, up by 1.36% on March 11, 2021.

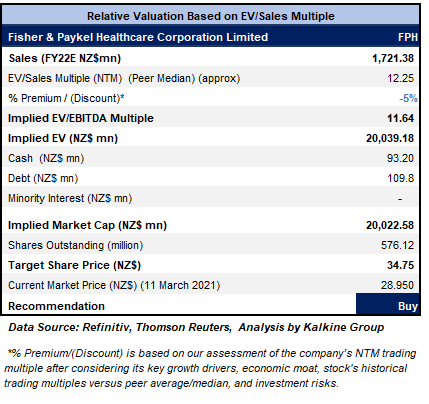

3) Fisher & Paykel Healthcare Corporation Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$16.6 billion, Gross Dividend Yield: 1.502%)

Business Description:

Fisher & Paykel Healthcare Corporation Limited (NZX: FPH) is the global leader in medical devices as well as systems for usage in respiratory care and acute care, as well as in the treatment of obstructive sleep apnea.

Outlook:

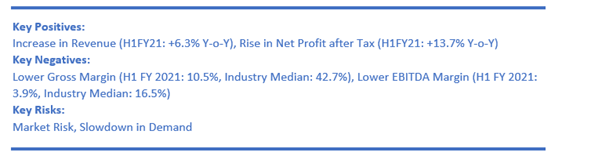

The company has commenced planning for its third manufacturing facility in Mexico, which is anticipated to be commissioned within the span of next 2 years.

The company’s hospital hardware sales continued to gain traction driven by the elevated hospitalisation rates for COVID-19. Meanwhile, the company is presently anticipating that revenue as well as net profit after tax for the 2021 financial year is expected to be higher than implied by the prior assumptions.

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

We have applied EV/Sales based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to EV/Sales multiple (NTM) peer median considering impact on gross margins because of increased usage of air freight as well as elevated costs associated with it.

Considering the expected upside and rise in NPAT, we give a “Buy” at NZ$28.950 per share, down by 0.58% on March 11, 2021.

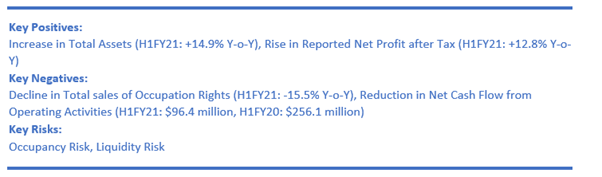

4) EBOS Group Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$4.6 billion, Gross Dividend Yield: 3.176%)

Business Description:

EBOS Group Limited (NZX: EBO) is engaged in the business of marketing, wholesaling and distributing healthcare, medical and pharmaceutical products. The company is also a major player in the marketing and distributing of recognised consumer products and animal care brands.

Outlook

The company stated that first half operating cash flow stood at $98.7 million, reflecting a 33.0% increase on the pcp. Notably, the cash performance implies the robust earnings growth as well as continued working capital management discipline.

Further, it has maintained the industry leading cash conversion cycle of 16 days. In line with the strategy of investing for growth, the company has completed two acquisitions during H1FY21. The Cryomed acquisition in the medical devices sector as well as the acquisition of CH2’s vet distribution business each strengthen the existing presence in those sectors and they are EPS accretive to the shareholders of EBOS.

The company is well placed in terms of its scale and market leading positions in stable industries along with its robust balance sheet.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

.png)

Considering the expected upside and rise in revenue, we give a “Hold” rating at NZ$28.60 per share, up by 0.35% on March 11, 2021.

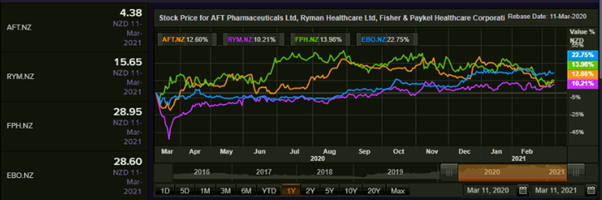

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...