Summary

As per New Zealand Export Market Guide 2018, New Zealand is dependent on the primary sector with food and agricultural products accounting for approximately 55 percent of total exports. The figure increases to 65 percent when forestry and seafood are included. An estimated 80 to 90 percent of New Zealand’s primary production is exported. As per the release by Stats NZ on June 29, 2020, profits for Māori authority farming businesses reached $97 million in 2018, almost double of 2017 figures. More than 200, or around one-sixth, of Māori authorities are in agriculture. Broader primary sector is divided into agriculture and fishing sectors, and both the sectors have been playing a key role in boosting the overall growth of the NZ economy.

New Zealand’s aquaculture industry is one of the most efficient and most sustainable forms of protein production on the planet. The New Zealand aquaculture industry has evolved from a group of innovative pioneers to a professional, specialized and quality food production sector concentrating on environmental sustainability, food safety and value-added marketing. Seafood makes a significant contribution to the national economy owing to its linkages with other industries.

The sector is dominated by inshore and offshore marine capture fisheries which represent about 80% of production with the remaining 20% coming from the aquaculture sector.

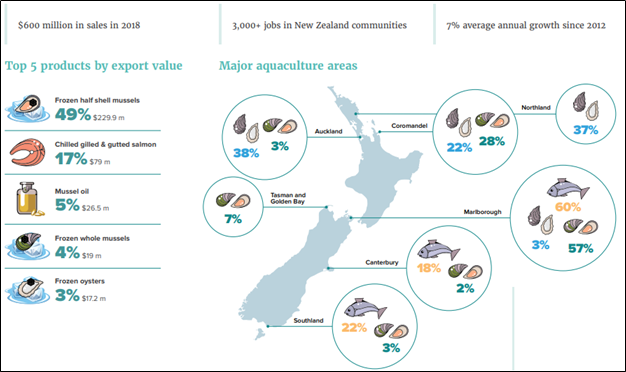

Industry At A Glance (Source: Fisheries New Zealand)

Increased Government Support Might Help Aquaculture and Farming Industry

The Government is backing a $27 million project which is aimed at boosting sustainable horticulture production and NZ’s COVID-19 recovery efforts. The country’s horticulture sector has been one of the export star performers, and this sector has contributed around $6 billion a year to the economy. The Government of New Zealand has decided to work alongside the aquaculture industry to deliver economic growth and jobs for the regions as part of an ambitious goal for it to become a $3 billion industry by 2035.

Alongside the $3 billion goal, the New Zealand Aquaculture Strategy focuses on:

Seafood Exports Heavily Impacted by Lockdown

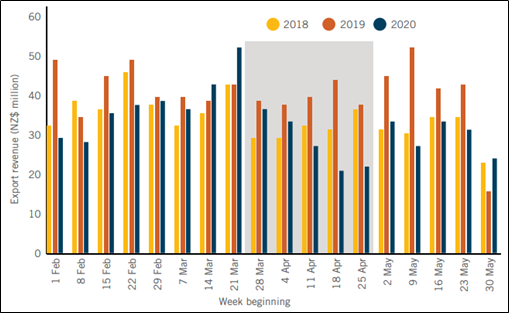

According to the provisional trade data provided by Stats NZ, New Zealand’s seafood export revenue tracked down 27 percent in February, up 7 percent in March, and down 44 percent in April relative to the prior year. Trade in February was heavily impacted by China’s lockdown, and April was impacted by the capacity restrictions due to New Zealand’s lockdown.

Total weekly seafood exports 2018-2020 (Source: Stats NZ and MPI)

Exports of seafood continued to slow through Level 4, finishing 23 percent down, driven largely by the 38 percent drop in revenue from China over the period. With 35 percent of seafood exports going to China, fresh seafood was affected by COVID-19 earlier than other industries, culminating in 68 percent lower export revenue to China in February, driven mostly by declines in airfreighted rock lobster.

As per the report by Ministry for Primary Industries (MPI), forestry export revenue fell 23% in February, 29% in March, and 62% in April as compared to the same period in 2019. Much of the decline in February and March is because of China’s lockdown. However, a portion of this is also because of significantly lower prices as compared to the previous year.

A major constraint is being faced by the country is limited potential from wild harvest fisheries. Despite the good size of fisheries water, they are not as productive as in other parts of the world. This limits the extent to which companies can invest in wild harvest fisheries. Besides, the industry is heavily reliant on exports for its major revenues. The sector has been affected by falling profitability from the reduced catch, increasing fuel prices, and strengthening of NZ Dollar value.

Demand Drivers of Future Growth: The Road Ahead

According to the statement made by Stuart Nash, Fisheries Minister on June 14, 2018, aquaculture export earnings are forecast to reach nearly $600 million in 2022. Aquaculture is set to be the main driver for the forecast growth, mainly due to increased mussel harvests, and higher prices as demand continue to grow in key markets. As global population grows and gets wealthier, global middle class is growing. Paired with heightened consumer awareness as well as connectivity, demand for healthy, sustainable and ethically produced seafood has been increasing.

Fishing industry is one of the most important export industries of New Zealand and is renowned all over the world for its quality products and safety standards. New harvesting and distribution methods are being tried out to maximize productivity and quality. The industry is also focused on creating new added-value products. Ways to create higher-value products such as dietary supplements and pharmaceuticals are being researched.

Since we now have a broad idea, let us now have a look at the performance of some companies operating in fishing and farming space (NZK, PGW, SAN, LIC)

1. New Zealand King Salmon Investments Limited (NZX: NZK) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$259.90 Million, Gross Dividend Yield: 3.754%)

Business Description: New Zealand King Salmon Investment Limited (NZX: NZK) is the world’s biggest aquaculture producer of the premium King salmon species.

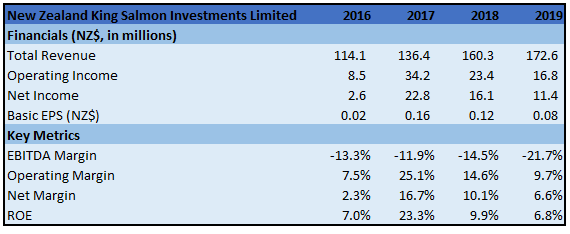

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: As a farmer and processor of King salmon, the company operates within the primary industry food producer category, which was included in the Government’s list of essential services. The company has affirmed previous guidance that expected FY 2020 Pro-Forma Operating EBITDA would be between $25.0 million and $28.5 million. FY20 forecast sales volume is expected to be 6,300-6,400 tonnes.

Key Risks: The company is exposed to financial risks relating to the production of salmon stock including increasing climate change volatility, climatic events, disease, and contamination of water space.

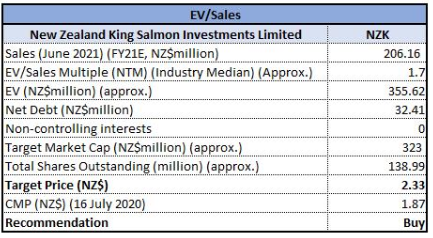

Valuation: We have applied EV/Sales Based Relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit growth (in % terms). Thus, we give a “Buy” recommendation at the price of NZ$1.870 per share.

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

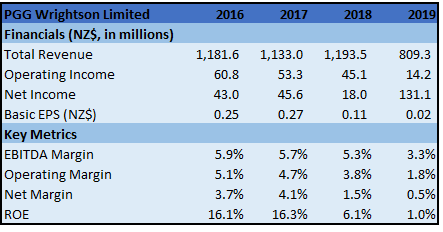

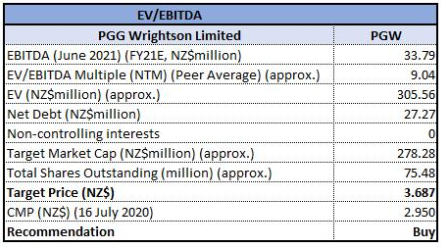

2. PGG Wrightson Limited (NZX: PGW) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$222.67 Million, Gross Dividend Yield: 7.639%)

Business Description: PGG Wrightson Limited (NZX: PGW) offers a wide range of products and services that allows it to be one of the key suppliers to the agricultural sector in New Zealand.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: In the month of February, the company forecasted operating EBITDA guidance of about $30 million for the financial year to 30 June 2020. However, due to the unprecedented events, the company has decided to withdraw the current guidance and place this under review until such time that the impact on earnings can be more accurately assessed.

Key Risks: The company undertakes transactions denominated in foreign currencies and exposure to movements in foreign currency arises from these activities. The company uses forward, spot foreign exchange contracts and foreign exchange options to manage these exposures.

Valuation: The company is well placed to come through a challenging period positively. In terms of fundamentals, the company has a strong balance sheet and has recorded a solid first half result. We have applied EV/EBITDA based relative valuation (on an illustrative basis), and the target price reflects lower double-digit growth (in % terms). Thus, we give a “Buy” recommendation at the current market price of NZ$2.950 per share.

EV/EBITDA Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

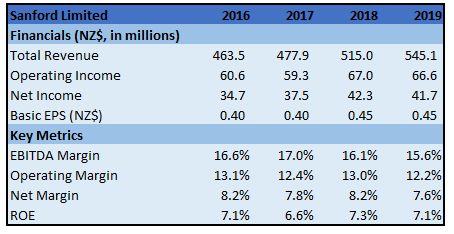

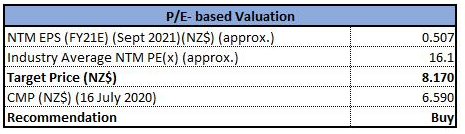

3. Sanford Limited (NZX: SAN) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$616.20 Million, Gross Dividend Yield: 4.023%)

Business Description: The resources of Sanford Limited (NZX: SAN) are committed almost entirely to inshore as well as deep-water fisheries of New Zealand, and allied operations of coolstores, shipbuilding, engineering and aquaculture.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company came under New Zealand’s primary industry sector and was classified as a provider of an essential service, and it continued to operate, when New Zealand moved to an Alert Level 4. The company’s robust balance sheet supports deployments next year to accelerate the progress with its innovation strategy, specifically with the marine extracts as well as its asset rejuvenation strategy.

Key Risks: A large proportion of the company’s sales are derived from exporting seafood products. Movements in foreign exchange rates have a significant influence on the degree of profitability of the company.

Valuation: The company is planning to improve its margins by reducing and containing fixed costs and recover its investments in sales and marketing. We have valued the stock using P/E based relative valuation (on an illustrative basis) and the target price reflects lower double-digit growth (in % terms). Thus, we give a “Buy” recommendation at the current market price of NZ$6.590 per share.

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

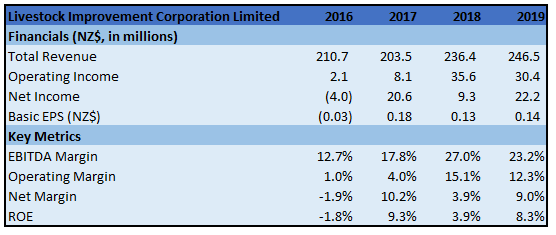

4. Livestock Improvement Corporation Limited (NZX: LIC) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~NZ$92.72 Million, Gross Dividend Yield: 20.326%)

Business Description: Livestock Improvement Corporation Limited (NZX: LIC) is a farmer-owned co-operative that provides a range of services and solutions to improve the productivity and prosperity of farmers.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has confirmed that its underlying earnings guidance for the year ended 31 May 2020 remains unchanged at $21 million to $25 million.

Key Risks: The company’s revenue may be reduced as farmers decrease expenditure as a consequence of reduced returns, availability of cash or an increased cost of production. Volatility of NZ’s milk price would affect returns paid to farmers: as a net exporter of milk, NZ’s milk price is, heavily influenced by reference to the price set by the Global Dairy Trade (or GDT).

Valuation: Based on the impacts of coronavirus on forecast milk price, credit tightening for farmers and increased compliance costs for the next season on NZ dairy farmers and LIC, the Board has updated the market range for the year ended 31 May 2021 to $16 million to $22 million. The stock’s EV/Sales multiple stood at 0.4x as compared to the industry average (Consumer Non-Cyclicals) of 1.5x. Also, EV/EBITDA multiple stood at 1.8x as compared to the industry average of 13.4x. Therefore, it can be said that the stock is slightly undervalued.

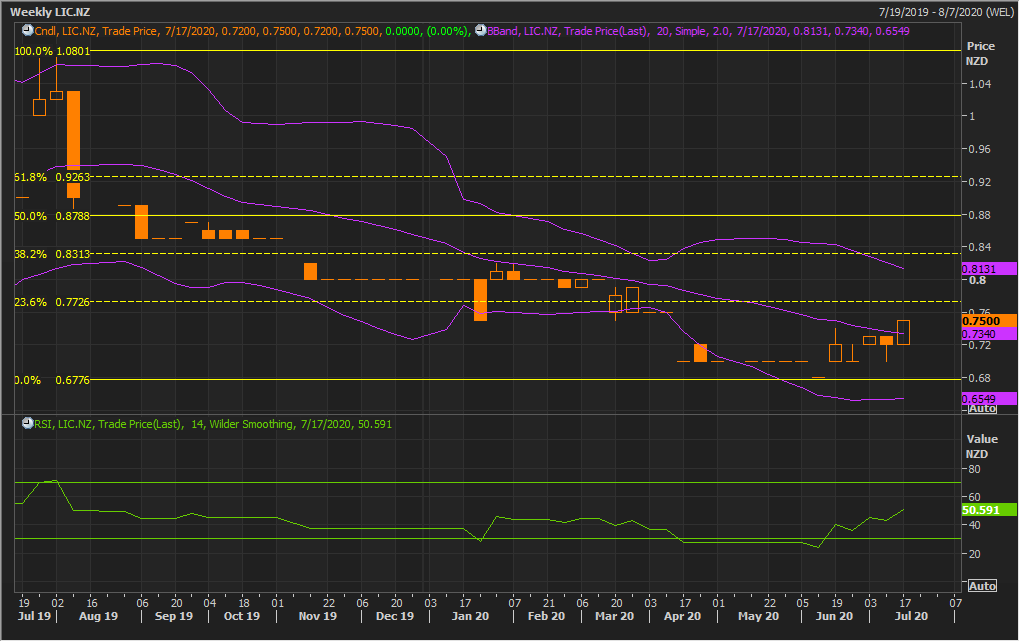

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

The stock has been trending up for the past few weeks including the on-going week. The on-going week has been more resilient. The stock opened at the previous week closing price level of $0.72 which remained low, made the high of $0.75, and closed there. This demonstrates strong positive sentiment on the stock. Technical indicator RSI with around 51 reading and curve at the end pointing up, suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around 38.2% retracement level of $0.83 while support could be around a recent low of $0.70.

Thus, we give a “Speculative Buy” recommendation at the current market price of NZ$0.750 per share.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...