.png)

Banking and Financial Services Sector Landscape

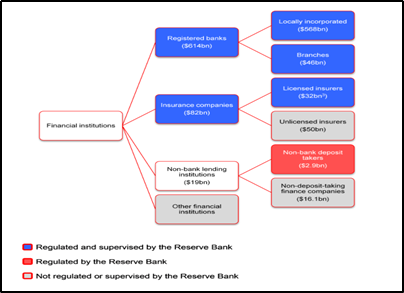

The financial system of New Zealand is broadly categorized into registered banks, insurance companies, non-bank lending institutions and other financial institutions as visible in the Figure 1 below. Registered banks dominate the overall financial system assets with a huge asset base (Figure 1). It also accounts for the major chunk of lending to the domestic non-financial private sector, while the issuance of corporate bonds and non-bank lending institutions (NBLIs) account for a minuscule 6% of non-financial private sector borrowing. However, capital markets are comparatively smaller in size and less developed in New Zealand, with an overall market capitalisation of around $169 billion at the New Zealand Stock Exchange, while that of country’s bond market is around $145 billion (excluding government debt). Further the managed fund industry is relatively small, with around $160 billion of assets under management.

The New Zealand banking system is highly regional focused with 27 registered banks. However, the country’s banking system is dominated by the four large Australian-owned banks viz; Australia and New Zealand Banking Group (ANZ), ASB Bank (ASB), Bank of New Zealand (BNZ), and Westpac (WBC) accounting for majority of bank lending (85%), while the five country’s owned banks accounts for only 6% of that pie. The New Zealand banking system is comparatively minute as compared to the global standards with the overall assets base of around $614 billion NZD in September 2020, which accounts for approximately 198 percent of GDP and stood at the lower range for OECD countries.

Figure 1: Financial Institutions’ Overall Assets Base (As of 30 September 2020)

Source: Reserve Bank of New Zealand (RBNZ)

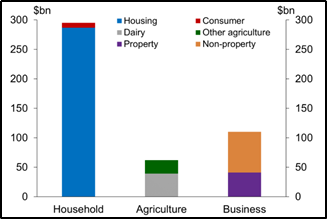

Notably, household borrowings accounts for major pie of lending which stood at 63% of overall bank lending followed by business sector lending (24%) and agriculture sector (13%).Of the total business lending, property related lending accounts for 37% as reflected in Figure 2 below.

Figure 2: Sectoral Banking System Assets (as of 30 September 2020)

Source: RBNZ

Key Growth Drivers

Some of the key growth drivers for Banking and Financial Sector which act as a catalyst for growth of the sector have been highlighted below: -

Signs of Revival in Economy

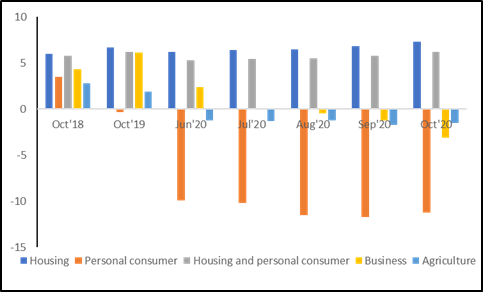

Although the financial services industry reeled under the impact of Covid-19 crisis, it is gradually returning to normalcy with the economy showing signs of improvement and business activities are picking up post lifting of restrictions. This augurs well for the sector, going forward. This is clearly manifested by the sector lending data by registered banks and non-bank lending institutions, which showed which showed household borrowings witnessing steady growth during July 2020 to October 2020 averaging at 6.75% annual growth as visible in Figure 3 below. Moreover, with the government focus on uplifting the economy from the adverse impact of Covid-19 crisis by stimulating demand and supporting the business environment by providing funding for lending along with lowering interest rates further and supporting the supply of credit to the economy. This will provide impetus to the rebound in the business’s capex cycle as well as boost the investment programmes at large. This in-turn will provide a further fillip to the sector altogether.

Figure 3: Sector lending (registered banks and non-bank lending institutions) Annual Growth Rate (%)

Source: RBNZ

Digital Disruption

It is helping the bank to evolve from the traditional way of transactions to ‘customer facing’ transactions with customers and remain connected. With the growing customers demand for more accessible, convenient and smarter transactions (using internet and mobile devices) , the banks are now becoming more digitised. The digital way of banking using latest technologies is enabling the banks to enhance the customer services as well as develop innovative products that anticipate customer needs to provide a whole gamut of services on a single platform, thus assisting in cross selling of products. This is aiding in bringing cost efficiency into the system and thereby improved profitability.

Long Term Outlook of Capital Market Investment Remain Robust

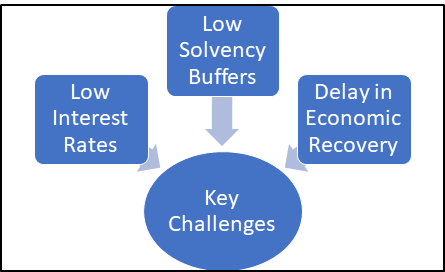

Key Risks and Challenges

Source: Kalkine Group

Prolonged Low Long-term Interest Rate

The Reserve Bank of New Zealand has consistently maintained its reduction its Official Cash Rate (OCR) at 0.25%. Although the low interest rate bodes well for the economic growth at large, however it acts as a detrimental to the earnings of the banks. With the low interest rate scenario is expected to prevail for a prolonged period across the world, so this could lead excess leverage and overheated asset prices.

Delay in Economic Recovery, Globally

New Zealand economy relies mostly on global demand of in-house products and the country’s financial system sources funds from international financial markets. The persistent slowdown in most global economies has cast a shadow on economic recovery of the country. . Further prolonged slowdown in the domestic economy would lead to rise in stressed borrowers and in-turn will lead to banks experiencing operating loss. . Any further delay in the rebound of the global economies from the adverse impact of Covid-19 pandemic and continuing world trade uncertainty, will further weigh on the growth prospect of the country and for that matter of sector, going forward. However, in the longer run, given governments globally injecting funds into the financial system to revive their respective economies, it is expected give rise to credit off-take resulting into economic recovery and eventually growth in financial sector.

Low Solvency Buffers of Insurers

Minimum solvency requirements mandated by the Reserve Bank required insurers to preserve sufficient capital and reinsurance coverage which allow them to cater to their future obligations towards policyholders with a high degree of certainty. However, it has been observed by the Reserve Bank that the solvency ratios for certain general and life insurers have fallen from the minimum required level, thus leaving a low buffer for them. Further the decline in the long-term interest rates in the recent times are also weighing on the insurers as this will create an asset liability mismatch and will negatively hurt earnings. With these insurers planning to improve their solvency and the Reserve Bank of New Zealand quick to address this issue and has increased supervisory engagement with the affected insurers would provide some relief.

Operational Risks

With the rise in dependence on technologies, especially in a system with high foreign ownership such as New Zealand’s financial institutions owned by foreign parents may expose to systemic consequences of operational disruptions during times of stress. The banking system in New Zealand is dominated by five large banks, which together accounts for 85% of all assets held in the banking system. These banks are owned by foreign countries with four being owned by Australian parent banks and one by UK parent bank.

Outlook

Although the financial sector at large is overburdened with higher regulatory framework, low interest rate environment and economic uncertainty, however, the Reserve Bank of New Zealand is bringing more effort to ensure long term viability of the sector. Further, the bank has implemented various liquidity measures to help stimulate the economy and the financial sector. The bank has extended the implementation of increased capital requirements for banks by 12 months to 1 July 2021. This will aid in banking sector to boost additional lending up to around $47 billion to the households as well to the businesses. Further it has also enacted a $100 billion government bond purchase programme. Meanwhile, the country’s financial system remains buoyant to face the adverse economic conditions with significant capital buffers and liquidity which enables banks to absorb losses and continue operating in these tough times.

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the financial sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Harmoney Corp Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$277.510 Million)

Business Description:

Harmoney Corp Limited (NZX: HMY) provides online direct personal lending services throughout New Zealand and Australia. It provides unsecured personal loans that are easy to access, competitively priced and accessed 100% online.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Outlook:

The IPO was helped by the range of institutional as well as retail investors throughout ANZ. Australia happens to be the substantial opportunity for the company as total addressable personal lending market is ~A$150 billion. It was mentioned that key structural drivers of growth include a shift in consumer preferences towards online services as well as ongoing technological innovation. The company is financed by numerous sources including the two “Big-4” bank warehouse programs throughout ANZ.

Considering the technical analysis, key structural drivers of growth and decent outlook, we give a “Buy” recommendation on the stock at the current price of NZ$2.750 per share on December 17, 2020.

2) Westpac Banking Corporation (NZX: WBC) (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$77.86 Billion, Gross Dividend Yield: 1.523%)

Business Description

Westpac Banking Corporation is one of the leading banks of Australia and also one of the largest banks in New Zealand. It is engaged in providing wide spectrum of banking and financial services, including consumer, business and institutional banking and wealth management services.

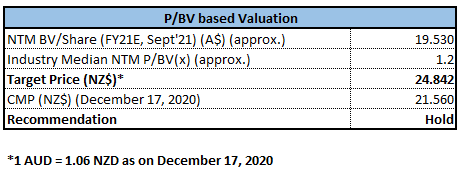

Valuation Methodology: P/BV Based Relative Valuation (Illustrative)

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Outlook

We have applied P/BV multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms).

Considering the increase in customer deposits, rise in liquidity coverage ratio and decent fundamentals, we give a “Hold” recommendation on the stock at the current price of NZ$21.560 per share, up by 0.19% on December 17, 2020.

3) The City of London Investment Trust Plc (NZX: TCL) (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.98 Billion, Gross Dividend Yield: 5.455%)

Business Description

The City of London Investment Trust Plc focuses towards providing long-term growth in income as well as capital, mainly by investment in equities which are listed on London Stock Exchange.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

After making the high of $9.12, the stock came under selling pressure and in the process, it made the low of $6.29. From the low, it has been striving to surpass the 50% retracement level of $7.37 decisively and move beyond but has so far, not been successful. However, for the ongoing week, the stock has given a stronger close with ‘Hammer’ pattern formed on the chart thereby exhibiting strength in uptrend. The technical indicator RSI with a reading around 59 and a curve at the end pointing up, suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around $7.78 where gap on chart exists. However, if stock retraces then it may find good support around the 23.6% retracement level of $6.45.

Outlook

The recent rally in the markets globally and initial signs of improvement could have a positive impact as the fund manager invests in the companies with cash generative businesses. Further, the portfolio is well-diversified and is also biased towards international companies invested in economies likely to witness growth even faster than the UK.

The Board of TCL announced that the 2nd interim dividend of 4.75p per ordinary share of 25p, with regards to the year ending June 30, 2021, would be paid on February 26, 2021.

Considering the technical analysis and decent outlook, we give a “Hold” recommendation on the stock at the current price of NZ$7.090 per share, up by 2.46% on December 17, 2020.

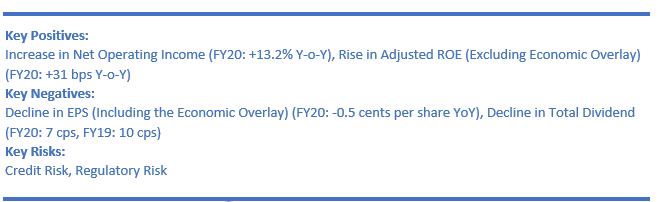

4) Heartland Group Holdings Limited (NZX: HGH) (Recommendation: Hold, Potential Upside: Low Single-Digit) (M-Cap: NZ$962.64 Million, Gross Dividend Yield: 5.965%)

Business Description

Heartland Group Holdings Limited (NZX: HGH) is a financial services group. In New Zealand, Heartland Bank Limited (NZX:HBL) is a registered bank, whereas in Australia, it is a dedicated player of providing reverse mortgage loans and funding to partners in the small business and consumer lending sectors.

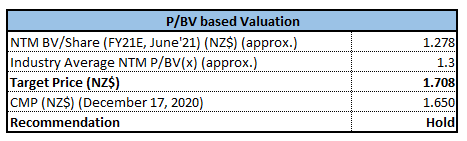

Valuation Methodology: P/BV Based Relative Valuation (Illustrative)

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Outlook:

As at 18 November 2020, 98.6% of consumer loans as well as 99.6% of SME and business loans are on usual (or pre-COVID) repayment schedules or have taken up Heartland Extend. In line with this, HGH is expecting the strong growth momentum to sustain across business and has guided for net profit after tax in the range of $83 million to $85 million for FY21. Notably, the company is increasing further investment towards expanding digital capability.

In Australia, the company has been exploring opportunities for the acquisition as well as organic growth in Consumer and Business markets. In NZ, its core strategic objective revolves around acquiring scale. All these initiatives will help the company to stay competitive and gain scale.

Heartland Seniors Finance is Australia’s leading reverse mortgage provider, and its 12-month market share witnessed a rise from 21% in March 2019 to 26% in March 2020. As per the release, similar trend has been anticipated in the future. In the financial year to June 30, 2020, Heartland’s Australian reverse mortgage receivables rose by $149.1 million (up by 18.4%) to $957.5 million.

We have applied P/BV multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of low single-digit (in % terms).

Considering the expected upside and expectations of strong growth momentum, we give a “Hold” recommendation on the stock at the current price of NZ$1.650 per share, up by 1.23% on December 17, 2020.

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...