Summary

Broader financial sector includes banking and insurance sector. While the banking system can be termed as a backbone of New Zealand economy, the relevance of insurance sector should not be understated.

The insurance sector plays an important role in the financial system by spreading the costs of risk events through time, across the population and, via reinsurance, internationally. A resilient insurance sector facilitates the efficient allocation of resources across the economy through the pricing and redistribution of risk. Banking and insurance in New Zealand is primarily characterized by robust fundamentals, stable business prospects and resilient nature. Key points on banking sector include:

Key Data (Source: RBNZ)

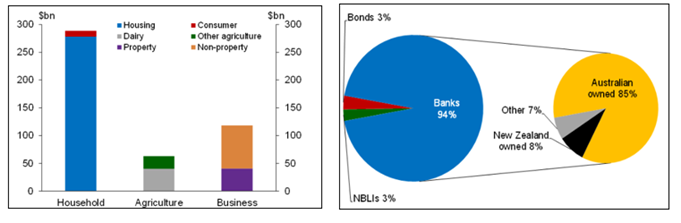

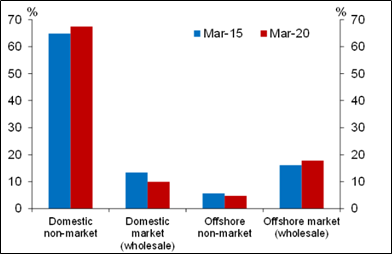

Funding Sources of Banks

According to RBNZ, bank funding is mostly sourced from domestic deposits (non-market) or the domestic wholesale market. However, a small pool of domestic savings create a structural need for the banking system to obtain funding from offshore.

Bank Non-Equity Funding Source (locally incorporated banks) (Source: RBNZ)

History of Life Insurance Industry in New Zealand

In New Zealand, life insurers began their operations in 1854, and the first sector-specific legislation, including a requirement to establish a statutory fund, was enacted in 1873. For the next hundred years or so, the life insurance sector was dominated by branches of large Australian mutuals and by Government Life Insurance, which was established in 1869 with initial capital from the New Zealand colonial government.

The latter half of the twentieth century saw a range of changes in the sector, such as the introduction of unit-linked and group policies. Unit-linked policies allowed policyholders to choose their own investment portfolios and bear the investment risk.

Annual Snapshot (Source: FSC)

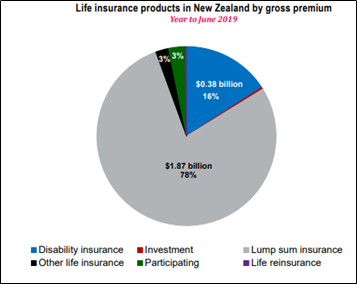

Characteristics of New Zealand’s Life Insurance Sector

According to RBNZ, a relatively narrow range of life insurance products is currently available in New Zealand, with most new life insurance policies only providing personal risk insurance. Lump sum insurance dominates the sector and accounted for 79% of gross premiums in the year ended June 2019.

Gross Premium (Source: RBNZ QIS)

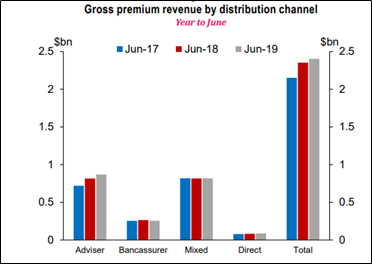

In New Zealand, life insurers generally acquire customers through independent financial advisers or through banking relationships. Bancassurance is normally an arrangement between an insurer and a bank that allows the insurer to offer its life insurance products to the bank’s customer base. Other channels are also used, like online distribution and outbound call centres.

Distribution Channel (Source: RBNZ QIS)

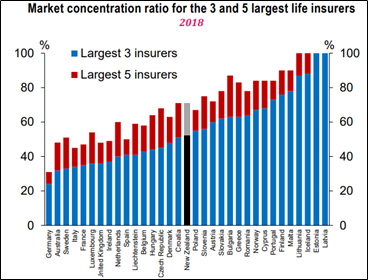

The largest three and the largest five life insurers in the country account for 54 per cent and 72 per cent of the life insurance premiums, respectively. If we consider these two market concentration measures, the life insurance sector in the country is not mainly concentrated and is near to the average. However, the sector is witnessing a few merger and some acquisition activity. It is anticipated that the sector will turn out to be more concentrated.

Market Concentration (Source: RBNZ QIS)

Resilient Nature Might Help NZ’s Banking Space

Given the backdrop that majority of lending to the private sector happens through banking system, it plays a dominant role in promoting economic growth with stability. The banking role has become all the more important as the economy is passing through global economic shock, caused by COVID-19.

Recent Trends in Credit Conditions

Banks have provided that, post lockdown, credit development has been predominantly demand-driven. Banks have experienced demand for loans for working capital from SMEs and corporates to meet fixed expenses. However, demand for credit for capex has fallen. Banks have noted that the low interest rates may support credit demand; however, uncertainty about future demand is causing businesses to review their investment plan. Banks have tightened lending standards to sectors directly exposed to the COVID-19 shock such as tourism, retail and construction. However, for some sectors such as commercial property and dairy, lending is a continuation of trends that precedes COVID-19.

Risks Faced By Banking and Insurance Sector

There is no denying the fact that the financial system in New Zealand is well-placed to weather out the economic impacts of the pandemic. However, it is exposed to risks of being stressed by failing business and loan default.

Even though there exists considerable uncertainty about the economic outlook, stress tests conducted for banks in New Zealand suggest that banks can withstand adverse scenario.

Since we now have a broad idea of banking and insurance sector in New Zealand, we will now have a quick look at the performance of some companies in the same sector (TWR, AMP, HGH, ANZ).

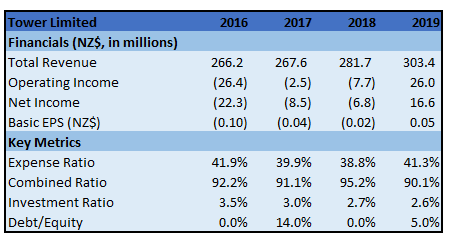

1. Tower Limited (NZX: TWR) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: NZ$255.09 million)

Business Description: Tower Limited (NZX: TWR) is primarily engaged in the provision of general insurance. The company mainly operates in New Zealand with some of its operations based in the Pacific Islands region.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company’s strategy is clearly focused on becoming a digital challenger brand, taking on the big incumbents and challenging outdated industry norms. In the month of March, almost 60% of the business came in through the company’s digital channels.

Key Risks: The financial condition and operating results of the company are affected by a number of key financial and non-financial risks. Financial risks include market risk, credit risk, financing, and liquidity risk. The non-financial risks include insurance risk, compliance risk and operational risk.

Valuation: The company has continued maintenance of robust capital base with solvency ratio of 280%. TWR stated that RBNZ has advised financial sector to protect solvency positions as well as preserve capital in light of COVID-19 disruption as well as uncertain economic outlook.

The company stated that continued growth via digital channels as well as a stabilised claims ratio demonstrate the successful implementation of its strategy. The company has updated its FY20 guidance of underlying NPAT to $25 million to $28 million after considering the Timaru hailstorm, Tropical Cyclone Harold, subdued growth as well as lower expenses.

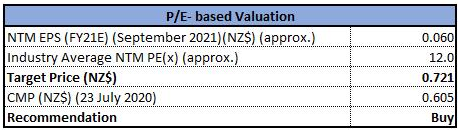

We have applied P/E multiple based relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms). Thus, we give a “Buy” recommendation on the stock at the current price of NZ$0.605 per share, up by 2.54% on July 23, 2020.

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

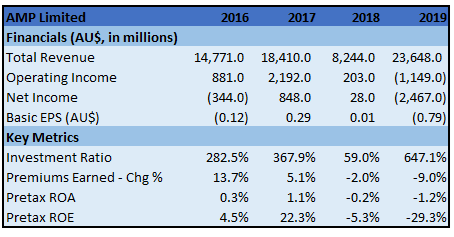

2. AMP Limited (NZX: AMP) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: NZ$6.46 billion)

Business Description: AMP Limited (NZX: AMP) is a wealth management company with a growing retail banking business and an expanding international investment management business. It provides retail customers with financial advice and superannuation, retirement income, banking, and investment products.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: In the second half of 2019, the company launched a three-year transformational strategy, which includes a significant cost reduction program. The company also undertook a capital raising last year to support the turnaround strategy of the company.

Key Risks: The company operates in multiple jurisdictions across the globe, including Australia and New Zealand, and each one of these jurisdictions has its own legislative and regulatory requirements. The financial services industry both globally and in Australia and New Zealand continues to face challenges with a significant level of regulatory change impacting the business.

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

From the past few weeks, the stock has been trading in the range provided by the upper Bollinger band on the upside and 20 periods SMA on the downside. The fact that, the stock is trading above 20 periods SMA and 61.8% retracement level, exhibits strength in uptrend. Technical indicator RSI with reading around 54 suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around $2.12, as provided by the upper Bollinger band while support could be around $1.63, as provided by 20 periods SMA.

Valuation: In 2020, the company is focused on execution and delivery of strategic priorities. It has ceased the plan to divest New Zealand wealth management business and will now focus on developing and growing the business in its existing market. AMP recently announced the completion of sale of its life insurance business, AMP Life, to Resolution Life for the consideration amounting to A$3.0 billion delivering a key priority in transformation strategy.

The company expects that any capital in excess of the target surplus post completion would be first used to finance delivery of the new AMP strategy. Beyond this, AMP would be assessing all capital management options with the intent of returning excess above target surplus to shareholders, subject to unforeseen circumstances as well as current economic and business conditions.

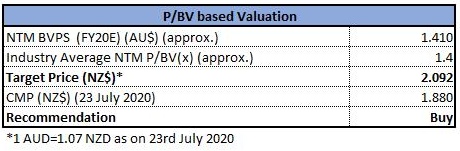

We have applied P/BV based relative valuation (on an illustrative basis) and the target price reflects a rise of lower double-digit (in % terms). Thus, we give a “Buy” recommendation on the stock at the current price of NZ$1.880 per share, up by 2.17% on July 23, 2020.

P/BV based relative valuation (Source: Refinitiv (Thomson Reuters))

3. Heartland Group Holdings Limited (NZX: HGH) (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: NZ$755.27 million, Gross Dividend Yield: 11.843%)

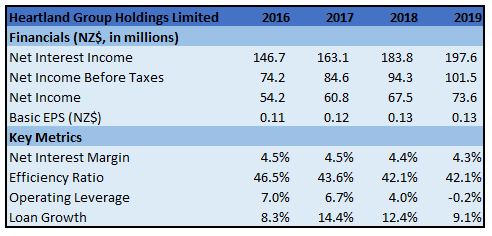

Business Description: Heartland Group Holdings Limited (NZX: HGH) is a financial services group with operations in Australia and New Zealand. In New Zealand, Heartland Bank Limited is a registered bank that concentrates on ‘best or only’ banking products in three key markets: Household, Business, and Rural. In Australia, it is a professional provider of reverse mortgage loans and offers funding to associates in the Consumer Lending and Small Business sectors.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: Asset growth from the bank’s core lending activities is expected to continue in the second half of FY2020, particularly in Australia and New Zealand reverse mortgages and small business lending. Investment will continue, specifically in marketing, to continue building awareness of reverse mortgages (in Australia and New Zealand) and Open for Business (O4B), as well as in new areas of opportunity. Some of these costs are anticipated to be one-off and will contribute to growth beyond FY2020. The underlying balance sheet growth supports a result in line with the original NPAT forecast in the range of $77 million to $80 million.

Key Risks: The bank is exposed to interest rate risk and foreign exchange risk. The market interest rates or foreign exchange rates can change and adversely impact the bank’s earnings due to adverse moves in foreign exchange market rates or in the case of interest rate risks mismatches between repricing dates of interest-bearing assets and liabilities.

Valuation: Fitch Ratings (Fitch) has recently affirmed the Long-Term Issuer Default Ratings (IDR) of Heartland Group Holdings Limited and Heartland Bank Limited at 'BBB' and the Long-Term IDR of Heartland Australia Group Pty Ltd at 'BBB-'.

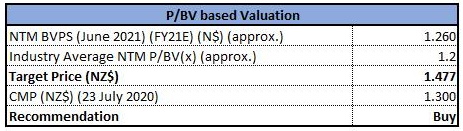

We have applied P/BV based relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms). Thus, we give a “Buy” recommendation on the stock at the current price of NZ$1.300 per share, up by 0.78% on July 23, 2020.

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

4. Australia and New Zealand Banking Group Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit), (M-Cap: NZ$56.43 billion, Gross Dividend Yield: 4.781%)

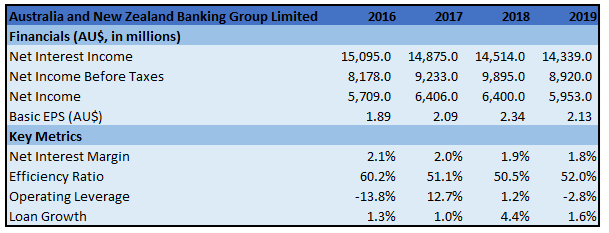

Business Description: Australia and New Zealand Banking Group Limited (NZX: ANZ) provides banking and financial products and services to individual and business customers and operate in and across 33 markets.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The bank’s core business continued to perform well with targeted balance sheet growth in preferred segments. It maintained a strong capital position with a Common Equity Tier 1 Capital Ratio of 10.8% at 31 March 2020, even after bolstering credit reserves to record levels. Liquidity also remained strong.

Key Risks: Increasing competition as well as regulatory requirements places pressure on margins and customer volumes. Demand for home lending in Australia and New Zealand is impacted by a range of supply and demand factors largely outside the bank’s control, including population growth, housing prices and dwelling construction.

Valuation: Total CRWA increased $27.9 billion (or 7.8%) from September 2019 to $386.0 billion at March 2020. As per the release, this increase is mainly because of lending growth in Institutional business ($11.5 billion) as well as impact of foreign exchange movements ($9.1 billion). The bank continued its focus on running the business as efficiently as possible with business as usual costs falling again.

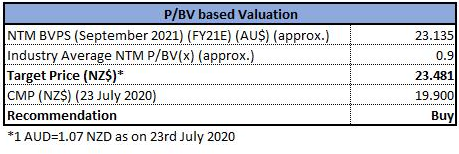

We have applied P/BV based relative valuation (on an illustrative basis), and the target price reflects a rise of lower double-digit (in % terms). Thus, we give a “Buy” recommendation on the stock at the current price of NZ$19.900 per share on July 23, 2020.

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

.png)

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...