Company Overview: Michael Hill International Limited is engaged in the retail sale of jewelry and related services sector. The Company's segments include Michael Hill, Emma & Roe, and Corporate & Other. The Company operates through four geographical segments: Australia, New Zealand, Canada and the United States of America. The Company operates a retail jewelry chain of over 300 Michael Hill and Emma & Roe branded stores. The jewelry collections available at Michael Hill stores include Michael Hill Designer Bridal, Infinitas, Everlight and Spirits Bay. The Company operates over 170 stores across Australia, over 50 in New Zealand, over 70 in Canada and over 10 in the United States. Emma & Roe offers a range of jewelry, such as charms, bracelets, rings, pendants and earrings that are interchangeable. Its jewelry features an array of stones, including diamonds, Murano glass and other gems. The Company's stores are located at Broadway Mall, New South Wales; Casey, Victoria, and Halls Head, Western Australia.

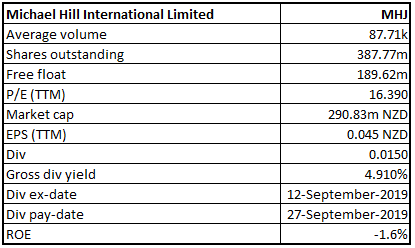

MHJ Details

Decent Sales Performance Across all Markets: Michael Hill International Limited (NZX: MHJ) is primarily engaged in the retail sale of jewellery and related services sectors in Australia, New Zealand, and Canada. During the year ended 30 June 2019, the company reported a statutory net profit after tax amounting to A$16.5 million, as compared to FY18 restated profit of A$1.6 million. EBIT for the period stood at A$34.6 million, which went down in comparison to prior corresponding period EBIT of A$40.1 million and was partially offset by the cost out program announced in February 2019. Same store sales of the business returned to growth in the fourth quarter with an increase of 0.7%. The period was characterised by continued investment in technology for the purpose of migrating to a highly integrated IT environment. The period was also marked by continued investment and development across the e-commerce business that bounced back with a record uplift of 43.6% in online revenue, representing 2.8% of total sales. At the end of the period, the company has 306 operating stores, after inclusion of ten new stores opened during the period. In FY19, the company closed 5 Emma & Roe stores along with 11 under-performing stores. In Q1FY20, same store sales of the company went up by 11.9% on prior corresponding period, as positive sales momentum started taking shape from the fourth quarter of FY19. All the markets responded with impressive sales performance, particularly Canada and New Zealand.

Going forward, the company is focusing on improved performance in the Australia retail segment through improved retail in-store execution and product newness, continued online revenue growth and strong property portfolio management. The New Zealand retail segment is expected to reap benefits out of operational improvements, improved cost efficiencies, and continued refinement of the property portfolio.

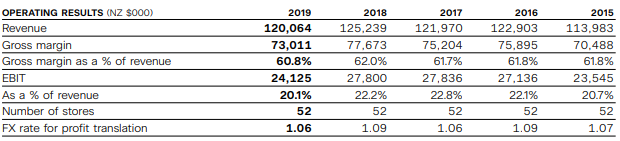

Over a period of 5 years covering FY15 – FY19, the company reported a top-line CAGR growth of 1.3% in the New Zealand retail segment, with FY15 and FY19 revenue amounting to $113.98 million and $120.06 million, respectively. The Australia retail segment reported a top-line CAGR growth of 0.4%, with FY15 and FY19 revenue of A$294.44 million and A$313.59 million, respectively. The Canada Retail segment reported the highest CAGR growth of 13.9%, with FY15 and FY19 revenue amounting to C$79.10 million and C$133.15 million, respectively.

Australia Retail Segment Results (Source: Company Reports)

New Zealand Retail Segment Results (Source: Company Reports)

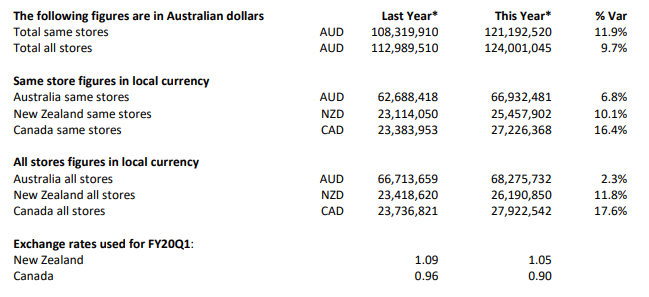

Highlights of Q1FY20: During the quarter ended 29 September 2019, all the markets reported a positive movement in same store sales. The highest growth in sales was reported in Canada at 16.4%, followed by New Zealand at 10.1% and Australia at 6.8%. Overall group same store sales witnessed a rise of 11.9% on prior corresponding period. Due to volatility in the retail environment, gross margin could not be recovered to historic levels but has seen a slight improvement from Q4FY19.

Segment Details: Same store sales and all stores sales in the Australia retail segment went up by 6.8% and 2.3%, respectively. The company closed three under-performing stores, with a total of 165 stores reported as at 29 September 2019. Due to widespread discounting in the sector on account of competition for market share, the market continues to be challenging for the business. Same store sales and all stores sales for the New Zealand retail segment went up by 10.1% and 11.8%, respectively, reflecting the strength of the brand and a strong lift in the market share. As at 29 September 2019, the segment had 52 trading stores. The highlight of the period was the Canada retail segment, that reported same store sales and all stores sales growth of 16.4% and 17.6%, respectively, as the company delivered on its Canadian productivity strategy. During the period, one new store was opened under the segment, taking a total number of trading stores as at 29 September 2019 to 87.

Q1FY20 Sales Performance (Source: Company Reports)

Although the competitive environment will pose a challenge to the business, the company has taken various measures to counter those challenges and will continue to introduce more such initiatives to succeed in the future. The company is committed to modernise the business and is working on improving the online business to drive increased customer relevancy in a rapidly changing retail environment.

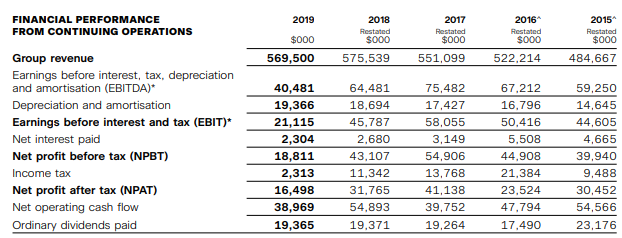

Dividend: In FY19, the company declared a final dividend of AU 1.5 cents per share, taking full year dividend to AU 4.0 cents per share, as compared to AU 5.0 cents per share in the period corresponding period. Total amount of ordinary dividends paid during the year amounted to A$19.36 million.

FY19 Financial Performance (Source: Company Reports)

Recent Updates: At the 2019 Annual General Meeting, the management notified about a range of measures taken to improve the performance of the business. The company came up with new initiatives and strategies that expanded the market share and improve results going forward. One of the most important decision was to strengthen the executive team in order to bring in new talent with a fresh perspective. In mid-November, the company signed in Daniel Bracken as the new CEO, who contributed a positive momentum to sales in a very short time period. Significant advancements were made across all areas of people proposition after Joanne Matthews joined as the Chief People Officer. Andrea Slingsby was appointed as the Chief Operating Officer. Over the past one year, the company has made good progress on its digital and data capability, a key enabler for a more relevant personalised customer experience. In addition, the company has also come up with several initiatives to shape the business in FY20. Under the initial annualised cost out program for A$5 million, the company has identified an additional cost reduction of A$5 million to be delivered across FY20 and FY21. Going forward, it aims to focus on the online channel to expand its digital platform and provide richer customer experience. As Canada represents a significant opportunity in terms of productivity, the company is planning to drive sales per square metre and sales per hour, benefits from which will unfold over the course of FY20.

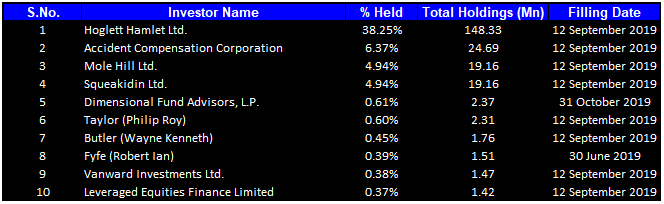

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 57.30% of the total shareholding. Maximum number of shares were held by Hoglett Hamlet Ltd. with a percentage holding of 38.25%, followed by Accident Compensation Corporation with a holding of 6.37%. Mole Hill Ltd. and Squeakidin Ltd have a holding of 4.94% each in the company.

Top Ten Shareholders (Source: Thomson Reuters)

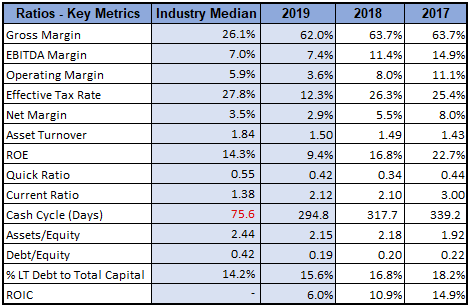

Key Metrics: During the year ended 30 June 2019, the company reported a gross margin of 62.0%, which was slightly lower than the previous year’s margin of 63.7%, but much higher than the industry median of 26.1%. EBITDA margin for the year stood at 7.4%, which is higher than the industry median of 7.0%. At the end of the period, the company has a current ratio of 2.12x, which stood above the industry median of 1.38x, representing a better liquidity position to address short-term business liabilities in comparison to peers. Debt-to-Equity ratio for the period remained almost flat in comparison to previous year at 0.19x but was lower than the industry median of 0.42x, again reflecting financial stability than the competitors.

Key Metrics (Source: Thomson Reuters)

Outlook: The first quarter of FY20 has laid a strong foundation as the company enters the crucial Christmas trading period. During the period, the company performed remarkably in the Canadian retail segment by focusing on its productivity strategy for the region, through restructuring of the retail operations team, introduction of the new operating model, product launches, etc. The company’s leadership team is continuously working on developing new ways of maintaining and growing its customer base, with many initiatives to be taken over the remainder of FY20.

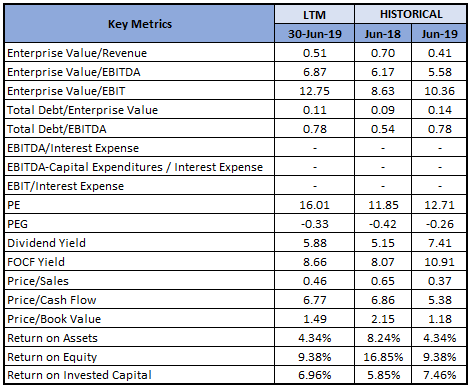

Key Valuation Metrics (Source: Thomson Reuters)

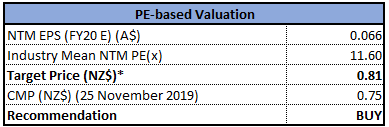

Valuation Methodology: Price-to-Earnings Multiple Approach:

Price-to-Earnings Multiple Based Valuation (Source: Thomson Reuters), *1 AUD equals ~1.06 NZD (as on 25 November 2019)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company is currently trading at a market price of $0.750 and has a price-to-earnings multiple of 16.390x. FY19 proved to be a challenging period for the business but demonstrated signs of improvement towards the end, with same store sales momentum depicting recovery in Q4FY19. The period also reported decent growth in e-commerce sales and a percentage reduction of 11.4% in debt, depicting an improvement in financial stability. The efforts made to revive the business were evident from the trading update for Q1FY20, which depicted positive sales performance across all the markets. Moreover, the company has taken several initiatives for FY20 to underpin the future success of the business. Considering the performance in Q1FY20, strategic initiatives discussed for FY20, such as cost reduction, improvement in online channel, increased focus on Canada productivity, and anticipated positive impact in the future, we have valued the stock using a relative valuation method, i.e., Price-to-Earnings multiple and arrived at a target price of high single-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$0.750, up 2.74% on 25 November 2019.

MHJ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...