Company Overview: Metlifecare Limited owns and operates retirement villages in New Zealand. The Company is engaged in providing rewarding lifestyles and care to over 5,000 New Zealanders. Many of the Company's villages also provide a full continuum of care from independent villas and apartments through to serviced apartments, rest homes and hospitals. It offers retirement living across the Bay of Islands, Auckland, Hamilton, Bay of Plenty, Manawatu and the Kapiti Coast. The Company offers various levels of care and support, depending on the village and user's needs. Its aged-care assistance ranges from serviced apartments, rest home and hospital options. Its assisted living options are designed for residents, which includes regular support in the form of daily tasks and/or medical assistance. Its independent living accommodation includes villas, apartments and cottages. Its subsidiaries include Forest Lake Gardens Limited, Hibiscus Coast Village Holdings Limited and Metlifecare Bayswater Limited.

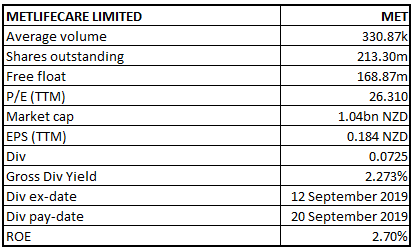

MET Details

Higher Settlement Volumes and Margins Drive Revenue Growth: Metlifecare Limited (NZX: MET) is an owner and operator of retirement villages, providing rewarding lifestyles and outstanding care to more than 5,500 customers across New Zealand. Currently, the company owns a portfolio of 25 villages in areas with strong local economies, excellent growth rates and high median house prices. During FY19, the company reported decent operating performance with 4% growth in underlying profit before tax, in comparison to the previous year. Increased settlement volumes and margins, along with a significant contribution from the care business, drove the revenue to $131 million, up 14% on previous year. The company reported pleasing results from sales of new homes, settling 116 new Occupation Right Agreement (ORAs) over the year. In comparison to the previous year, the number went up by 18%. Average selling price per new home also increased to $689,000, up 5% on FY18. The period was also marked by settlement of 354 resales of ORAs, representing a growth of 3% on previous year. Average selling price per home was reported at $572,000, up 6% on previous year.

Going forward, the company expects growth to be driven by high demand, strong pricing, and resident satisfaction. The positive response from customers reflects the success of investments made in the quality of villages. The company is now looking forward to expansion through land acquisition, which will be supported by a strong balance sheet with low gearing and attractive funding options.

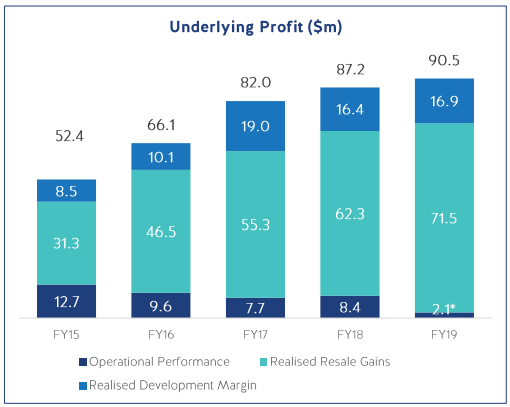

Over the period covering FY15 to FY19, the company has witnessed continued growth in the underlying profit, reflecting the impact of positive resales performance and development margins. Underlying profit CAGR over the above-mentioned period stands at 14.6%, with the highest growth reported in FY16 at 26.1%. In FY18, profit pertaining to operational performance amounted to $8.4 million as compared to $2.1 million in FY19. The gap in operational performance was due to the higher promotional spend, higher property costs, and expensed interest costs. Top-line CAGR growth stands at 7.3%, with FY15 and FY19 revenue amounting to $101.5 million and $131.0 million, respectively.

Growth in Underlying Profit (Source: Company Reports)

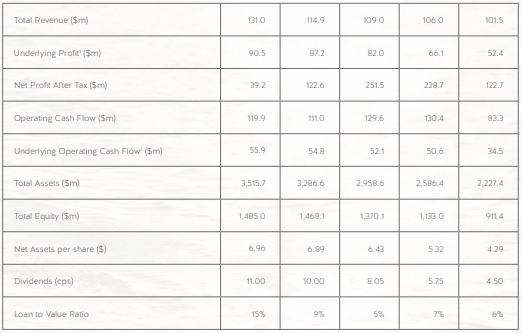

Five-Year Performance (Source: Company Reports)

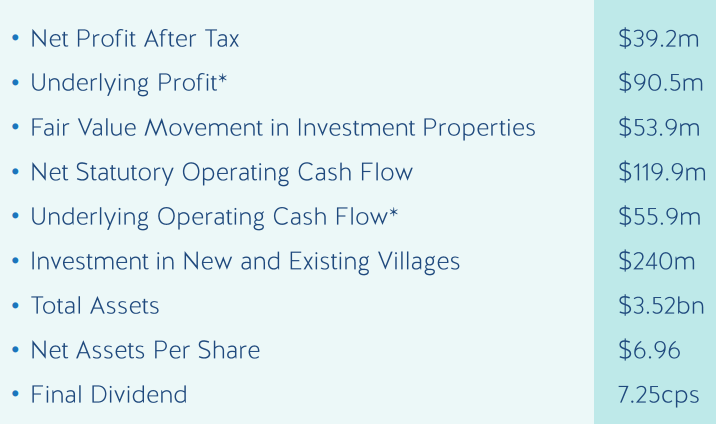

A Quick Look at FY19 Results: During the year ended 30 June 2019, the company’s reported NPAT came in at $39.2 million, down 68.0% on prior corresponding period NPAT of $122.58 million, predominantly due to lower unrealised fair value gains in a slower real estate market. Underlying profit for the period stood at $90.50 million, up 3.8% on prior corresponding period profit of $87.15 million. Operating revenue went up by 8.3%, from $114.76 million in FY18 to $124.28 million in FY19. The period saw delivery of 182 units and beds, along with village occupancy of 97% and care occupancy of 96%. Operating revenue for the year amounted to $124.28 million, representing an increase of 8.3% on prior corresponding period revenue of $114.76 million. Operating performance during the year improved on the back of higher sales volumes, strong pricing and continued investment in villages and resident services. Total assets during the year were reported at $3.5 billion, up by 7%.

FY19 Results Summary (Source: Company Reports)

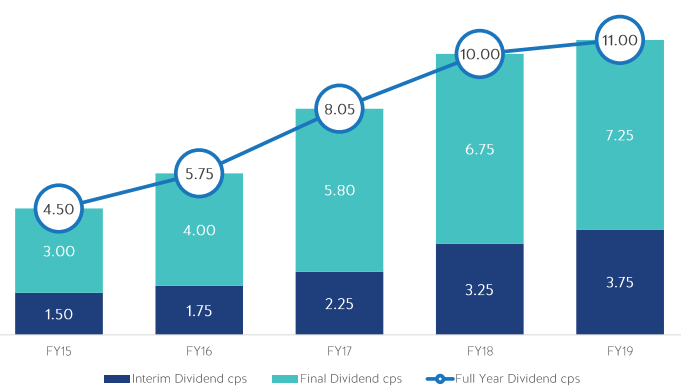

Dividend on Rise: The Board declared a final dividend of 7.25 cents per share, making the total dividend for the year ended 30 June 2019 to 11 cents, representing a growth of 10% on previous year. The dividend was paid to the shareholders on 20 September 2019. The final dividend declared was in line with the company’s policy to distribute 30% - 50% of underlying operating cash flow in the form of dividends.

5-Year Dividend Trend (Source: Company Reports)

Operational Highlights: During the year, settlement volumes went up by 18% for new homes and 3% in relation to resales. Sales price pertaining to new homes and resales went up by 5% and 6%, respectively. With three new premium care homes in place, the company witnessed a 19% increase in care capacity.

Capital Management: Due to land acquisitions made during the year, gearing increase to 15% at balance date, representing the lowest gearing in the listed retirement village sector. Recently, the company announced the retail bond offer of up to $75 million (with the ability to accept up to an additional $25 million in oversubscriptions), of 7 year secured fixed rate bonds maturing on 30 September 2026. The bonds will be offered to New Zealand institutional and retail investors. Proceeds from the offer are expected to support the replacement of a portion of bank debt, to provide diversity and increased tenor of funding.

Village Investment: During the year, the company invested an approximate amount of $240 million in new and existing village development. The company delivered a total of 182 new homes and care beds across four villages. In addition, 33 new homes are expected to be completed in the first quarter of FY20. Through the acquisitions of two new sites at Botany and Kerikeri, the company enhanced its development pipeline, which will add considerable value to the company’s village portfolio.

Remediation Programme: The company has in place a remediation programme that will provide it with improved competitiveness and value of homes. 85% of the remediation involves capital investment in village betterment and 15% involves general repairs and advancement of preventive property maintenance costs. In FY19 full year result presentation, released on 26 August 2019, the company reported that the total programme cost including investment made to the above date, represented 4% of the net assets or 31 cents per share.

During the year, the company witnessed continued growth in its investment property portfolio in a slower market, reflecting premium locations for its villages. To continue to build profitably in a changed construction environment, the company has re-phased certain aspects of its development programme and is also working towards strengthening its land bank through acquisition.

Recent Updates:

(a) Results of 2019 Annual Shareholders’ Meeting: At the meeting, the shareholders of the company passed three resolutions, pertaining to re-election of retiring Director, Carolyn Steele, authorisation to Directors to fix the fees and expenses of PricewaterhouseCoopers, auditor of the Company, and to amend the Company’s Constitution with effect from close of the meeting.

(b) Share Buy-back Programme: In another recent announcement, the company updated regarding an on-market share buyback programme of up to $30 million of its shares, which is believed to enhance value for continuing shareholders. Funding for the same will be done from funds received from the proposed and previously signalled sale of the company’s Albany site. The company believed that the buyback represents an efficient use of capital while the share price remains significantly below the intrinsic value of the business and can be managed without compromising on the company’s ability to invest in its continuing development activities. Proceeds from the share buyback programme are expected to be received during 2020.

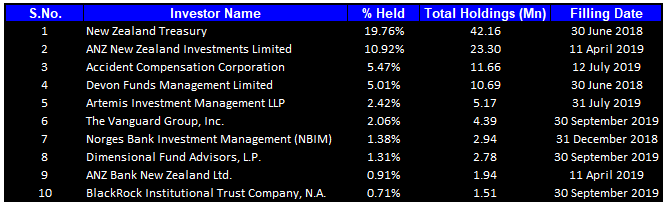

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 49.95% of the total shareholding. New Zealand Treasury is the entity, holding maximum shares in the company at 19.76%. ANZ New Zealand Investments Limited is the second largest shareholder, with a percentage holding of 10.92%.

Top Ten Shareholders (Source: Thomson Reuters)

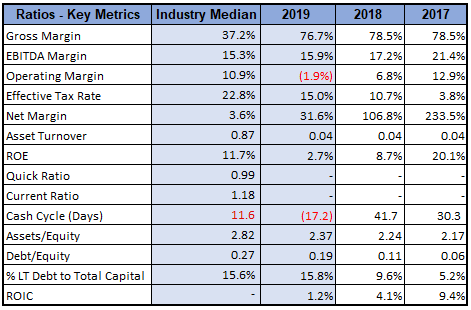

Key Metrics: During the year ended 30 June 2019, the company reported a gross margin of 76.7%, which is higher than the industry median of 37.2%. EBITDA margin for the year was reported at 15.9%, which is slightly above the industry median of 15.3%. However, the margin was lower than previous year’s EBITDA margin of 17.2%. Net margin for the period stood at 31.6%, significantly above the industry median of 3.6%. Moreover, the company stands at a better position in comparison to the industry, with respect to debt also. In FY19, debt to equity ratio for the company and the industry stood at 0.19x and 0.27x, respectively.

Key Metrics (Source: Thomson Reuters)

Outlook: The company has a remediation programme in place, which is expected to be completed in 2023. The programme is expected to provide improved competitiveness and value of homes for the company. Going forward, the company’s strategy will be based on investment in markets that offer the best long-term value creation and retain a high conviction in the premium locations. The programmes have been developed in a way that will ensure profitability without losing focus on key markets. By the end of 1HFY20, the company expects to deliver 80 units. In addition, 280 units and beds are expected to be under construction for delivery in FY21.

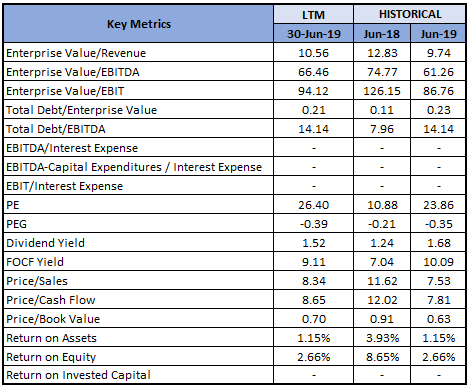

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

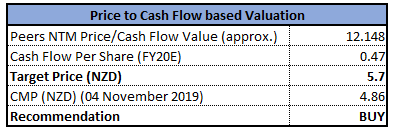

Method 1: Price to Cash Flow Multiple Approach:

Price to Cash Flow Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

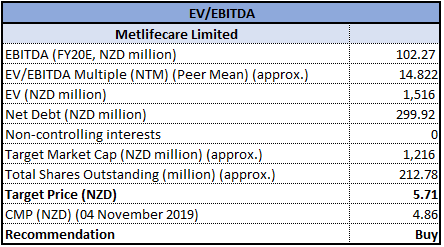

Method 2: Enterprise Value to EBITDA Multiple Approach:

EV/EBITDA Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: In FY19, the company witnessed decent growth across key financial metrics. Higher settlement of new homes generated total realised development margin of 21%. Alongside, higher settlement from resales increased realised resales gains by 15%. The recently announced buyback programme is also well aligned with the company’s plans to invest in development activities, which are expected to ramp up early in the new calendar year. Over the next three years, the company is expecting to invest an amount of over $500 million in five major projects. The management expects that the projects will provide strong value accretion to the business, in turn providing growth prospects to shareholders. A low gearing ratio of 15% provides ample scope to fund ongoing targeted growth for the business. Considering the above factors, we have valued the stock, using two relative valuation methods, i.e., Price to Cash Flow multiple, and Enterprise Value to EBITDA multiple, and arrived at a target price of lower double-digit growth (in % term). Hence, we recommend a “Buy” rating on the stock at the current market price of $4.86.

MET Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...