Company Overview: Power & Renewable Energy company, Meridian Energy Limited (NZX: MEL) is involved in the business of generation, trading and retailing of electricity, and the sale of complementary products and services. The Company operates through three segments: Wholesale, Retail and International. The Wholesale segment includes activity associated with its New Zealand generation of electricity and its sale into the wholesale electricity market, purchase of electricity, and development of renewable electricity generation opportunities. The Retail segment includes activity associated with retailing of electricity and complementary products through its two brands: Meridian and Powershop in New Zealand. The International segment includes activity associated with its generation of electricity and sale into the wholesale electricity market, retailing of electricity through the Powershop brand in Australia, and licensing of the Powershop platform in the United Kingdom. The Company supplies electricity to power homes, businesses and farms.

MEL Details

Meridian Energy Limited is New Zealand's largest electricity company wherein the Government retains 51% ownership. MEL is the only New Zealand electricity company with a customer and asset base diversified throughout different countries. The company generates 100% electricity through renewable sources. The market capitalisation of the company stood at ~$13.19 billion on March 8, 2021.

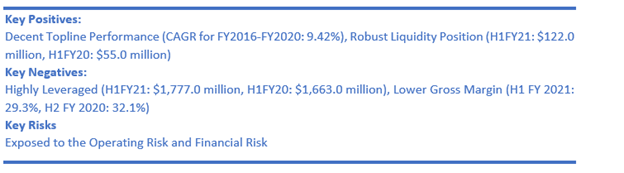

Looking at the past performance over FY16 to FY20, the top-line of the company grew with a compounded annual growth rate (CAGR) of 9.42%. The total revenue of the company improved from $2,375.0 million in FY16 to $3,405.0 million in FY20.

Results Performance (Half-Year ended 31 December 2020)

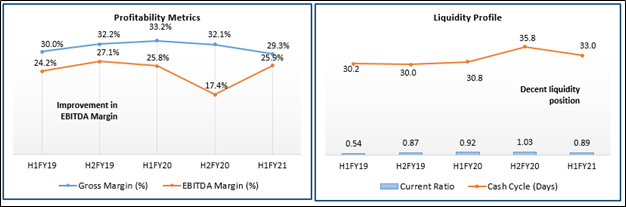

The company reported its revenue from continuing operations for the first half period of FY21 stood at $1,869 million, an increase of 5% on the previous corresponding period (pcp). Net profit for the period which includes positive changes in the value of hedge instruments stood at $227 million, an increase of 19% on pcp. However, excluding these hedge value movements, MEL reported a 9% decline in its EBITDAF. Besides, lower New Zealand hydro generation and lower market prices in Australia also negatively impacted EBITDAF from last year’s record level. Customer numbers across New Zealand and Australia have grown by 3% since June 2020, exceeding half a million.

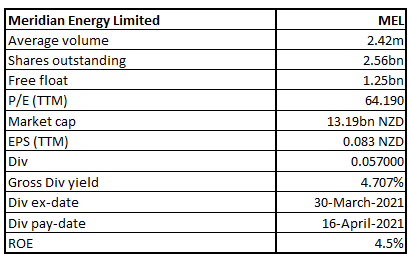

Exhibit 1: Financials

(Source: Company Reports)

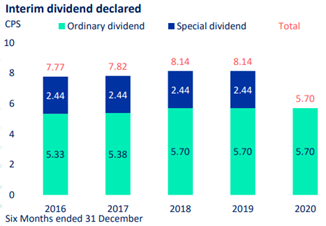

The Board of Directors declared an interim dividend of 5.70 cps (86% imputed), with a record date and payment date on 31 March 2021 and 16 April 2021, respectively.

Exhibit 2: Information on Dividends

(Source: Company Reports)

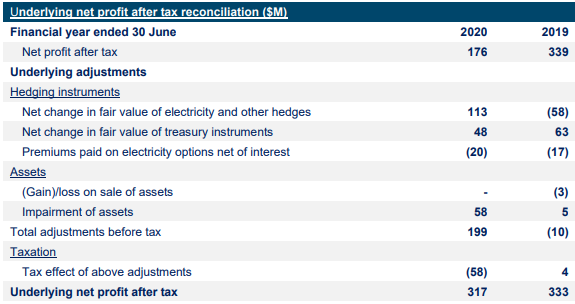

Results Performance (Year ended 30 June 2020)

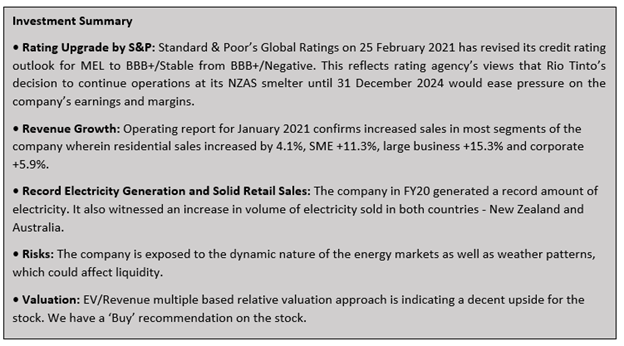

Group’s EBITDAF for the full-year period, stood at $854 million, an increase of 2% on the previous year, mainly due to increased retail performance in both New Zealand and Australia. MEL generated a record amount of electricity in New Zealand underpinned by improved wind farm availability and lake inflows that were 115% of average. There was an increase in the volume of electricity sold to customers by 18% in New Zealand and 24% in Australia. Underlying net profit after tax (which removes fair value movements) for the period declined by 5%. There was an increase of 3% in ordinary dividends in FY20.

The period witnessed significant development with Powershop New Zealand being named as Energy Retailer of the Year at the Deloitte Energy Excellence Awards, and MEL came out on top of the major retailers in Consumer New Zealand’s power satisfaction survey.

Exhibit 3: FY20 Key Metrics

(Source: Company Reports)

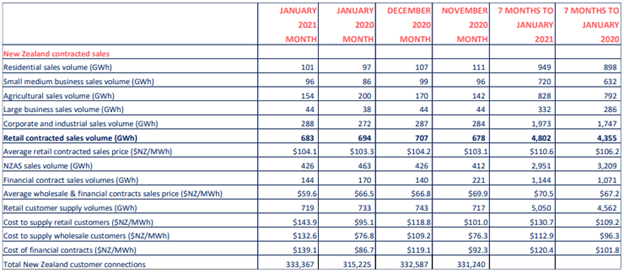

Operational Performance for January 2021:

National hydro storage from the start of January month till the date 11 February 2021, increased from 79% to 80% of historical average. While North Island storage decreased to 97%, South Island storage increased to 78% of average by 11 February 2021. Total inflows in the month stood at 84% of the historical average. National electricity demand in January 2021 was 4.1% lower than the same month last year. MEL’s retail sales volumes for the month stood 1.6% lower than the same period last year. The company witnessed an increased sales in most segments wherein large business segment grew by +15.3%, followed by SME (+11.3%), corporate (+5.9%), and residential (+4.1%). However, agricultural volumes were 23.2% lower than the same period last year.

Exhibit 4: Key Data for New Zealand Market

(Source: Company Reports)

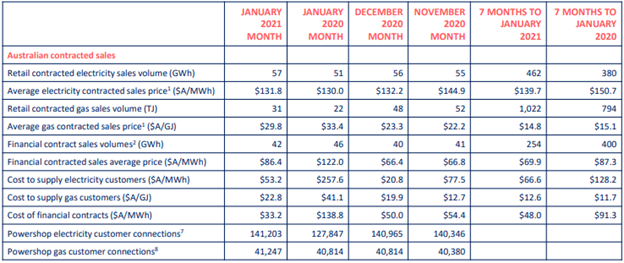

Exhibit 5: Key Data for Australian Market

Source: Company Reports

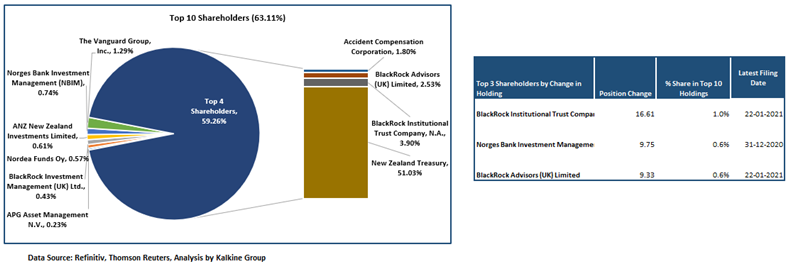

Top 10 Shareholders: The top 10 shareholders have been highlighted, which together forms around 63.11% of the total shareholding. New Zealand Treasury and BlackRock Institutional Trust Company, N.A. are holding a maximum stake in the company at 51.03% and 3.90%, respectively.

Exhibit 6: Top 10 Shareholders

A Quick Look at Key Metrics: The company’s net margin for H1FY21 stood at 12.1%, better than the industry median of 7.4%, implying an improvement in the operational efficiency of the company. Its ROE for H1FY21 stood at 4.5%, better than the industry median of 3.9%. Notably, its current ratio for H1FY21 stood at 0.89x, better than the industry median of 0.48x, implying that the company possesses better capabilities to meet the short-term obligations than the peer group.

Exhibit 7: Key Metrics

(Source: Refinitiv (Thomson Reuters)), Analysis by Kalkine Group

Recent Update:

Standard & Poor’s Global Ratings on 25 February 2021 revised its credit rating outlook for Meridian Energy Limited (MEL) to BBB+/Stable from BBB+/Negative, reflecting their view that Rio Tinto’s decision to continue operations at its NZAS smelter until at least 31 December 2024, eases previously forecast pressure on earnings and energy margins. At the same time, Standard & Poor’s affirmed Meridian’s ‘BBB+’ long-term issuer credit rating and ‘A2’ short term issuer credit rating.

In an earlier update of 24 February 2021, the company stated that MEL will soon begin construction of a new $395 million wind farm in Hawke’s Bay, boosting New Zealand’s ability to act on climate change and accelerating the transformation of the economy to clean energy sources.

Outlook:

The recent operational agreement with Rio Tinto who would now be extending the planned closure for Tiwai Point from August 2021 to December 2024, has brought about great relief for the MEL as Rio Tinto happens to be the largest customer of the company. The move will provide certainty on earnings. Besides, the company’s decision of constructing of a new $395 million wind farm in Hawke’s Bay will not only accelerate the transition of the economy to clean energy but also earnings for the company in the years to come.

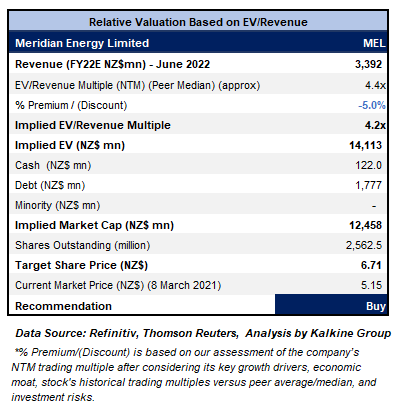

Valuation Methodology: EV/Revenue Based Relative Valuation (Illustrative)

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock came under selling pressure ever since it made a high of $9.94. It has given a lower close on the first trading session of the ongoing week at $5.15. The technical indicator RSI with a reading around 41 and a flattish curve at the end suggests flattening of weaker momentum for the stock.

Going forward, the stock may have resistance around the 61.8% retracement level of $6.02 whereas support could be around the lower Bollinger band of $4.50.

Stock Recommendation:

The monthly operating report for January 2021 suggests increased sales across most segments compared with the same period last year. The stock has delivered a return of ~3.42% in the past six months, and a return of ~10.5% in the past one year. It is trading below the average of 52-week high price of $9.94 and 52-week low price of $5.15.

Considering the aforesaid facts, we have valued the stock using EV/Revenue multiple based valuation (on an illustrative basis) and there are expectations that the stock price might witness an upside of low double-digit (in % terms). We have applied a slight discount to EV/Revenue (NTM) (Peer Median) considering the risks as the company trades in the wholesale energy markets and is exposed to volatility in the forward energy prices. Also, it is exposed to the dynamic nature of the energy markets as well as weather patterns.

Hence, we give a “Buy” recommendation on the stock at the current market price of $5.15 per share, down by 3.01% on March 8, 2021.

.png)

MEL Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...