Company Overview: Meridian Energy Limited (NZX: MEL) is engaged in the business of electricity generation from 100% renewable sources like wind, water, and sun. All the electricity that the company supplies to the customers comes from the electricity grid, that mixes electricity supplied from renewable as well as non-renewable sources. The company is listed on the NZX and ASX and it is one of NZ’s largest listed companies which employs ~1,000 people throughout NZ and Australia. Notably, the NZ Government happens to be the majority shareholder at 51%.

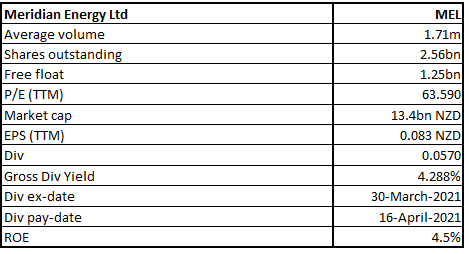

MEL Details

.png)

.png)

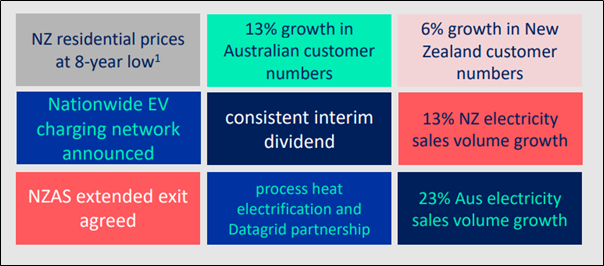

Results Performance (6 months ended 31st December 2020)

Meridian Energy Limited is the country's main electricity generator and the significant retailer. Its revenue from continuing operations rose by 5% YoY to $1,869 million. The company has managed to report 19% rise in the net profit for the 6 months ended 31st December 2020, that includes positive changes in the value of hedge instruments. However, excluding these hedge value movements, the company has witnessed a 9% fall in the EBITDAF. Notably, customer growth continued, however, lower NZ hydro generation as well as lower market prices in Australia adversely impacted EBITDAF from previous year’s record level. The fall in EBITDAF was mainly driven by the 7% decline in the generation production because of low inflows to the South Island hydro catchments since October 2020.

In January 2021, the company made an announcement that it reached an agreement with the largest customer, Rio Tinto. Rio Tinto operates the Tiwai Point Aluminium Smelter in Southland and it would be extending the planned closure period. The extension will be from August 2021 to December 2024.

Exhibit 1: H1 FY 2021 Highlights

(Source: Company Reports)

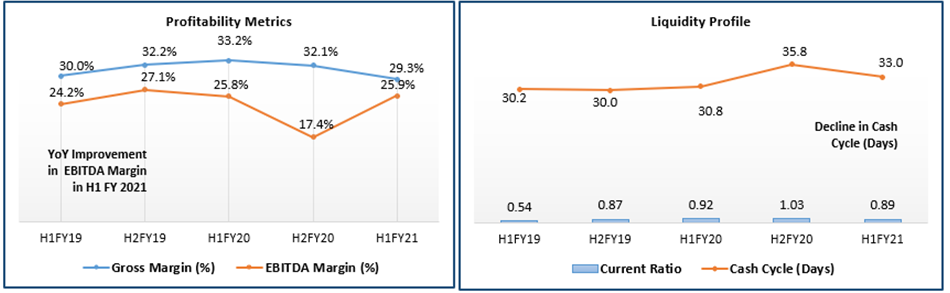

Key Metrics

The company’s gross margin for H1 FY 2021 stood at 29.3% and its EBITDA margin stood at 25.9%. Its net margin stood at 12.1% in H1 FY 2021 as compared to the industry median of 6.1% which reflects that the company is possessing better capabilities to convert its top line into bottom-line as compared to the broader industry. MEL’s Debt/Equity ratio stood at 0.35x as compared to the industry median of 0.95x and, therefore, it could be said that the company’s is having decent leverage position.

Exhibit 2: Key Metrics

Source: Refinitiv, Thomson Reuters, Analysis by Kalkine Group

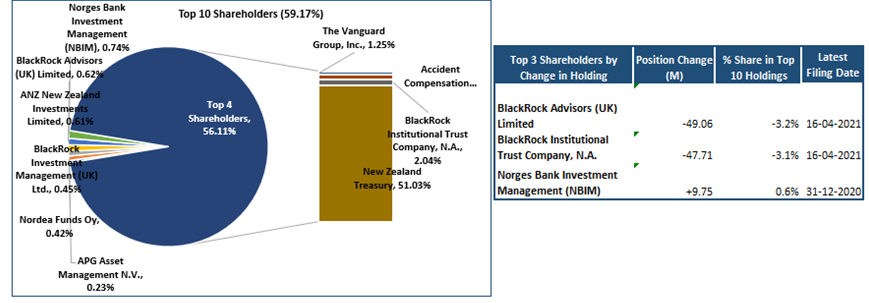

Top 10 Shareholders:

The top 10 shareholders have been provided in the below given pie chart which together forms ~59.17% of the total shareholding. New Zealand Treasury and BlackRock Institutional Trust Company, N.A. are holding maximum stake in the company at ~51.03% and 2.04%, respectively.

Exhibit 3: Top 10 Shareholders

Source: Refinitiv, Thomson Reuters, Analysis by Kalkine Group

Recent Updates:

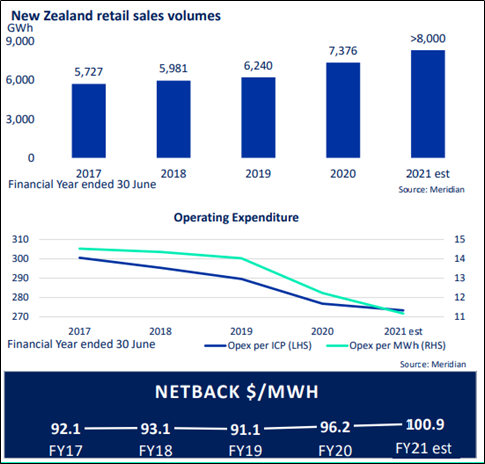

The company has recently released investor presentation in which it stated that, with respect to retail, profitable growth was delivered via volume and margin management and it witnessed improvement in the financial performance even though there was increased competition as well as pressure on the retail margins. Also, discipline on the controllable costs amidst increasing customer base led to the continued reduction in the operating expenditure by ICP and MWh.

Exhibit 4: New Zealand Retail Sales Volumes

(Source: Company Reports)

In the release dated 28th April 2021, MEL, and New Zealand’s Aluminium Smelter (or NZAS) agreed an electricity swap that will assist NZAS to voluntarily decrease the electricity consumption at the Tiwai Aluminium Smelter by up to 30.5MWh per hour. This became effective from 28th April till 31st May 2021 to help manage the dry hydrology conditions.

The company released monthly operating report for March 2021 on 20th April 2021. As per the release, in the month to 13th April 2021, national hydro storage witnessed a fall from 70% to 59% of the historical average. Notably, South Island storage fell to 59% of the average and North Island storage reduced to 57% of average by 13th April 2021. However, compared to March 2020, there has been an increase in segment sales in SME (+26.8%), agricultural (+10.9%) as well as corporate (+23.9%). The sales were lower in residential (-2.7%) and large business (-1.6%). The company’s Q3 total inflows were 70% of the historical average as well as 31% lower than Q3 of the last year. However, all the segments witnessed increased sales, except agricultural, that decreased by 3.7%.

As per the release dated 8th April 2021, the company confirmed that Jason Stein, CEO of Meridian Energy Australia and Powershop Australia, have decided to continue in the role till the end of the calendar year.

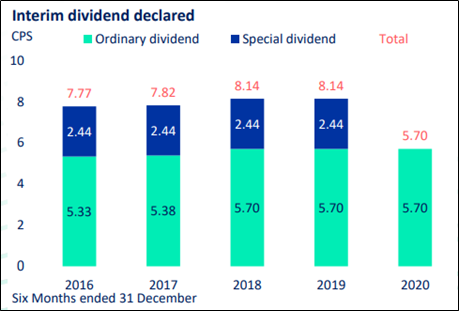

Decent Dividends Reflect Financial Strength:

The company declared interim ordinary dividend amounting to 5.70 cps, 86% imputed, which is same as compared to H1 FY 2020. The company has managed to maintain consistency in its dividends which reflects that it is focussed towards delivering returns to its shareholders, despite challenging business conditions.

Exhibit 5: Dividends

(Source: Company Reports)

Key Risks

The company’s performance is exposed to several risks like uncertainty with regards to the gas supply as well as frequent change in climatic conditions. Moreover, fall in generation production can impact the company’s EBITDAF.

Outlook

The company’s operating costs have remained flat as compared to H1 FY 2020. However, there was modest growth in Australia as well as Flux spend, but this was offset by the lower NZ asset maintenance. The company’s FY 2021 capital expenditure is anticipated at the higher end of the range of $70 million- $80 million. It is expected that newly committed wind as well as geothermal projects (2.7TWh) will enable 90% renewable energy generation over the time span of next few years.

As per the report, the new $395 million wind farm in Hawke’s Bay was deferred in the month of July due to NZAS announcing the intention to exit NZ. However, as NZAS has decided the 4-year exit deal, the company is now confident that Harapaki will support the growth plans. Notably, the Harapaki wind farm would be the country’s second-largest wind farm, with 41 turbines generating 176 megawatts of renewable energy. This will be enough to power over 70,000 average households. The construction will take ~3 years and is anticipated to create 260 new jobs. It would also help in boosting the country’s ability to meet the climate change commitments as well as accelerate the transformation of the economy to the clean energy sources.

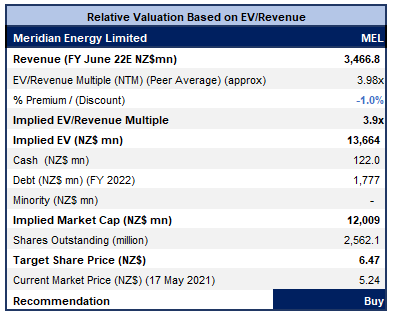

Valuation Methodology: EV/Revenue Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock ascended from the low of $3.57 and in the process, made a high of $9.97. From the high, it has corrected beyond a 61.8% retracement level of $6.02, and has been experiencing a low volatility for the past couple of weeks. In the first trading session of the ongoing week, the stock has given a softer close amidst low volatility. The technical indicator RSI with a reading around 44 and a flattish curve at the end, suggests flattening of neutral momentum.

Going forward, the stock may have resistance around the converging point of a 61.8% retracement level and 20 periods SMA of $6.02 whereas support could be around $5.00 which has held strongly in the past.

Stock Recommendation

The stock price of the company declined by ~17.3% in 6 months. It has made a 52-week low and high of $4.300 and $9.94, respectively. The stock is trading towards the 52-week lower levels. The generation volume as well as price volatility are the features of NZ’s hydro-based renewable electricity system. However, in H1 FY 2021, there was robust underlying performance of the business and the company was pleased with the strength of Meridian and Powershop brands.

We have valued the stock using EV/Revenue multiple-based illustrative relative valuation and have arrived at the target price which reflects the rise of low double-digit (in % terms). We have applied a slight discount to EV/Revenue Multiple (NTM) (Peer Average) considering lower EBITDA and gross margins as well as the risks related to the climate change.

Considering the above facts, we give a “Buy” recommendation on the stock at the current market price of NZ$5.240 per share, down by 0.38% on 17th May 2021.

Note: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...