Company Profile: Mainstream Group Holdings Limited (ASX: MAI) provides global outsourced fund administration and custody services to a range of wealth management sector participants. Based on the internal management structure, the group is organized into business units based on geographic locations with Asia-Pacific, the Americas and Europe as the reportable segments. The company was listed on ASX in 2015 to support growth in Asia-Pacific. It has its offices in Australia, Singapore, Hong Kong, United States, Cayman Islands, Ireland, Malta, and Isle of Man and manages over 1,012 funds with FUA of around $187.1 billion..png)

MAI Details

.png)

Decent Growth Momentum and Record FUA in 1H20: Mainstream Group Holdings Limited (ASX: MAI) provides global outsourced fund administration and custody services to a range of wealth management sector participants. As on 24 April 2020, the market capitalization of the company stood at ~$53.4 million. It has achieved another year of growth and improved financial results by delivering on its strategy of providing global fund administration services to its clients. During FY19, revenue and earnings of the company witnessed continued growth, with revenue and EBITDA growing for the fifth year in a row. During the year, revenue of the company reached $50.0 million, reflecting an increase of 21% on FY18. The majority of this is sourced from recurring income from long term contracts. In the same time span, EBITDA grew to $7.4 million, up by 17% on FY18 and funds under administration reached $173 billion, achieving a growth of 24% on the prior year. The group administers 1,012 funds for 356 clients. The company also reported a strong balance sheet strengthened by capital raise and strong cash generation in the underlying business.

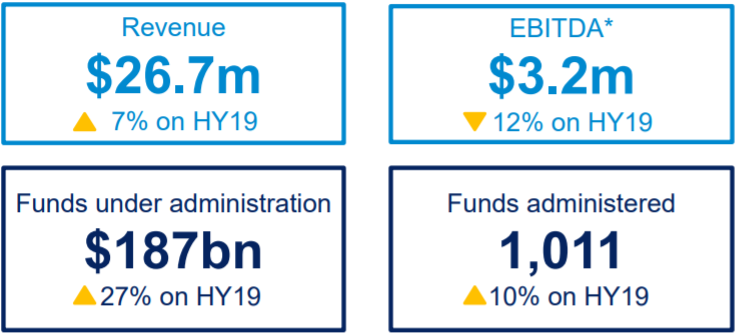

The company has also released its results for the half year ended 31 December 2019, wherein it reported record FUA of $187 billion. MAI continued to benefit from strong growth in its key markets and clients, as reflected in the sizeable increase in funds under administration over the period. During the half year, the company witnessed an increase of 7% in revenue, driven by ongoing demand for services in the core markets of Australia, Asia and the US. MAI continued to enhance its operating platform for future growth via targeted investment in people, processes, and technology. The company maintains a net cash position in excess of regulatory capital requirements and is investing in growth while reducing debt.

The company is well-positioned for continued growth with good momentum and a clear growth agenda. The company’s business model is based on high levels of recurring revenue with full-service administrator with deep client relationships and a diversified client base across markets. The company has attractive industry fundamentals to benefit from a continued trend towards fund administration and has a strong sales pipeline and growing brand awareness.

1H20 Financial and Operational Highlights (Source: Company Reports)

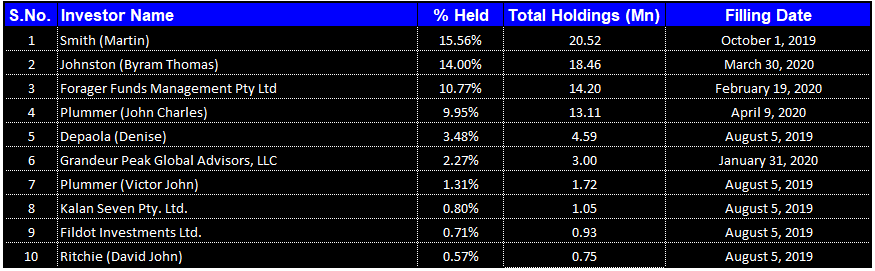

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Mainstream Group Holdings Limited.

Top 10 Shareholders (Source: Thomson Reuters)

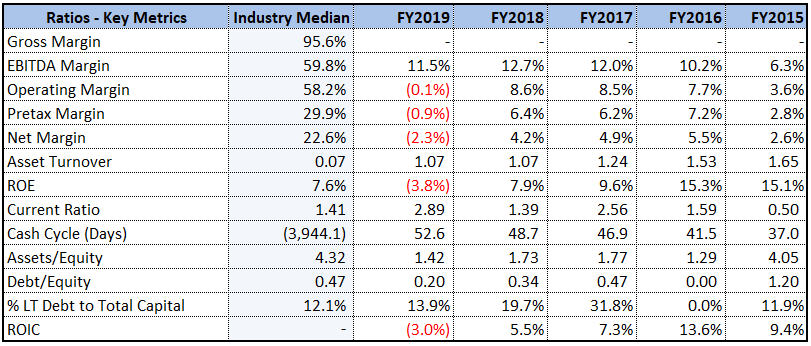

Increased Profitability and Decent Liquidity Levels: Over the span of 5 years from FY15 to FY19, the company witnessed an improvement in EBITDA margin, which stood at 11.5%, up from 6.3% in FY15. This indicates that the company has managed its costs well, thus increasing profitability. During 1H20, current ratio of the company stood at 2.89x, higher than the industry median of 1.41x. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. In the same time span, assets-to-equity ratio of the company was 1.42x, lower than the industry median of 4.32x and debt-to-equity ratio of the company stood at 0.20x as compared to the industry median of 0.47x. This indicates that the business is financed with a significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Thomson Reuters)

Growth in Core Markets: The company has recently released its quarterly results for the period ending 31 March 2020, wherein it reported steady funds under administration of $187.1 billion, reflecting a YoY increase of 15%. This comprised of net inflows from clients of $15.6 billion and market movements of $8.7 billion. While global markets fell by over 20% during the quarter, the exposure of the company to market movements was cushioned by its diverse client base and strong inflows. The number of clients remained the same, and net funds increased by 31 as compared to the prior quarter with continued wins in US private equity and significant growth in the Singapore and Hong Kong businesses despite COVID-19. The performance of the company was in line with expectations with a reduction in custody income, which however, was cushioned by higher transaction volumes. The company continued to maintain a net cash position of $10.5 million, in excess of regulatory capital of $8.1 million.

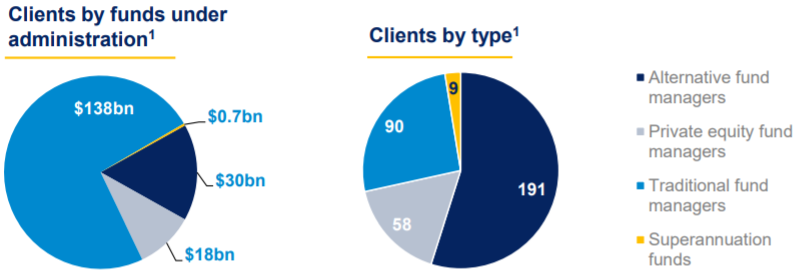

Diversified and High-Quality Client Base (Source: Company Reports)

Performance of the Segment: Based on the internal management structure, the group is organized into business units based on geographic locations with Asia-Pacific, the Americas and Europe as the reportable segments. During 1H20, Asia-Pacific region contributed 72% of the group’s revenue, which stood at $19.2 million. This was mainly due to decent progress on custody growth strategy and significant IT investments to lift automation and client experience. In the same time span, the Americas contributed 19% of the revenue, which stood at $5.0 million. This was mainly due to continued growth in private equity. During 1H20, Europe contributed 9% of the revenue of around $2.4 million. This revenue was impacted by the rationalization of smaller unprofitable clients and delayed fund launches.

Future Expectations and Growth Opportunities: The company is well-positioned to benefit from the continued trend towards fund administration and has a strong sales pipeline from deep client relationships and growing brand awareness. MAI has attractive fundamentals and is partnered with high-quality fund managers. The growth prospects of the company are promising with quality new business leads. It is focusing on investing in growth and expects to reap the benefits of these investments in FY21.

The company progressed with higher margin private equity and custody businesses and is expecting increased demand for its services. MAI is managing well through the outbreak of the virus and has adapted and risen to the challenge of this crisis while managing high volumes of transactions and enquiries. The company has undertaken initiatives to control its costs. It is maintaining service levels and business continuity and leveraging its experience from the Global Financial Crisis to assess the opportunities for permanent changes. MAI retains a strong balance sheet, demonstrating resilience to market conditions, via geographic and product diversity.

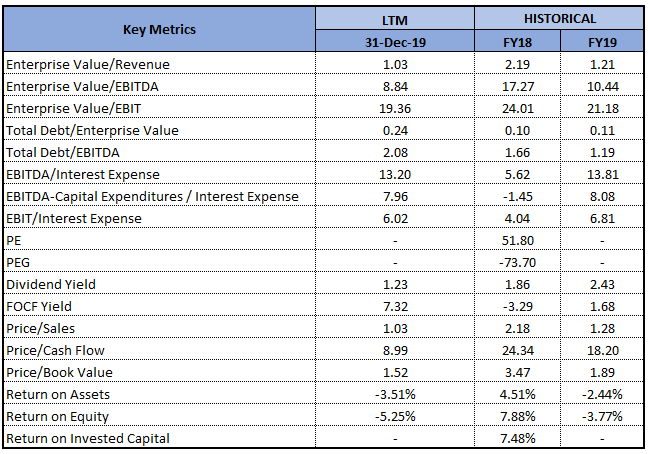

Key Valuation Metrics (Source: Thomson Reuters)

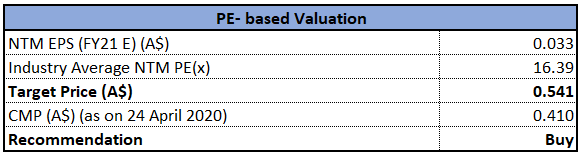

Valuation Methodology: P/E Multiple Based Illustrative Relative Valuation Approach

P/E Multiple Based Illustrative Relative Valuation Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of MAI gave a return of 62% in the past one month and is trading towards its 52-weeks’ low level of $0.245, proffering a decent opportunity for accumulation. During FY15 to FY19, the company witnessed a CAGR of 35.78% in total revenue, indicating clear growth momentum and deep client relationships. The majority of Mainstream’s revenue is recurring in nature, and the company expects robust revenue with some impact from market volatility. Considering the decent returns in last one month, trading levels, resilient business despite the uncertain environment and positive long-term outlook, we have valued the stock using Price to Earnings multiple based relative valuation approach and have arrived at an indicative target price offering an upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $0.410, up by 1.235% on 24 April 2020.

MAI Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...