Company Overview: Mainfreight Limited (NZX: MFT) is involved in providing a range of warehousing, domestic distribution, as well as international air and ocean freight services, under supply chain logistics. It operates its business from ~240 branches across ~20 countries. Under domestic supply chain, its operation comprises moving and storing freight within countries, while air and ocean freight includes operation of moving freight between countries. Its other product suite comprises, import and export by sea and air, customs clearance, tariff classification, and costing and consultancy all operated in house. New Zealand, Australia, The Americas, Asia and Europe, are the major geographies where it operates its business.

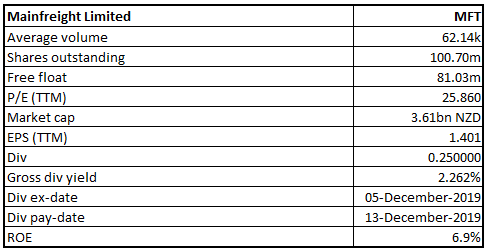

MFT Details

Investment Summary:

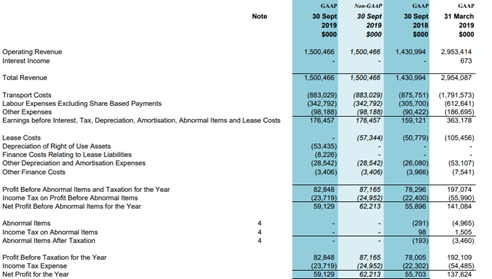

Satisfactory Improvement in Both Top-line and Bottom-line Performance for H1FY20: Mainfreight Limited (NZX: MFT) reported increase in total revenue for the first half period of FY20 by 4.9% to $1.500 billion, as compared to previous corresponding period (pcp). EBITDA for the period under IFRS 16, was reported at $176.46 million, an increase of 62.9% on pcp. Net profit for the half year period was reported at $59.13 million, an increase of 6.2% on pcp. The result is satisfactory reflecting the company’s global presence, underpinned by continuous increase in profits from Europe and the Americas along with improvement in margins and services in both regions.

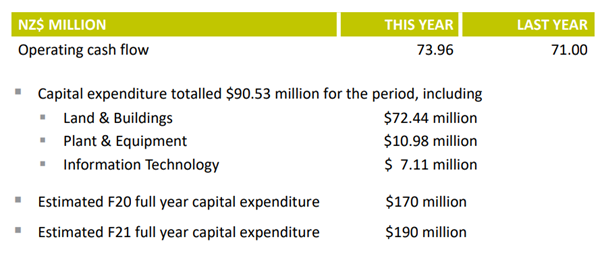

The company’s operating cash in-flow for the period was reported at $73.96 million, an increase of $71.00 million on the previous corresponding period (pcp), reflecting increased profitability and acceptable cash collection. Cash and cash equivalents at end of period was reported at $102.33 million, as compared to $85.32 million in the pcp. There are expectations that decent cash levels might help the company in carrying out operations effectively moving forward. Also, it can make deployments towards strategic growth initiatives. During the period, the Board of Directors approved an interim dividend (fully imputed) of 25.0 cents per share, an increase of 13.6% on the previous corresponding period.

Moving forward, there are expectations that its global presence, decent capabilities to convert top-line into bottom-line, decent capital management objectives and initiatives to reduce operating expenditure might help it in achieving decent growth levels.

H1FY20 Income Statement (Source: Company Reports)

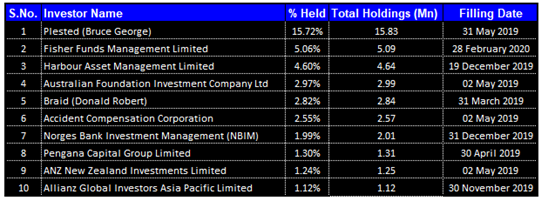

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in MFT:

Top 10 Shareholders (Source: Thomson Reuters)

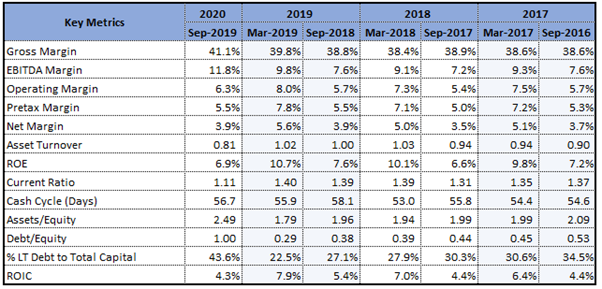

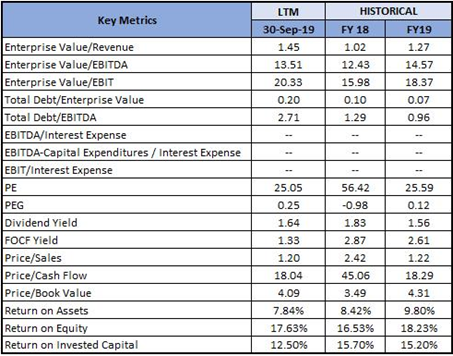

Overview of Key Margins: The company’s gross margin stood at 41.1% in 1H FY 2020 which is higher as compared to 1H FY 2019 figure of 38.8%. Notably, its net margin stood at 3.9% in 1H FY 2020 which is same as compared to 1H FY 2019 figure of 3.9% and, therefore, it can be said that MFT is possessing decent capabilities to convert its top line into bottom line.

Key Metrics (Source: Thomson Reuters)

Enough Cash Balance at the end of First Half of FY20: Net debt at the end of first half period was reported at $187.73 million, an increase of $57.25 million on pcp, and gearing ratios increased from 13.5% on March 31, 2019, to 17.5%. Net cash out-flow from investing activities for the period was reported at $90.53 million, an increase of $50.34 million on pcp. Net cash out-flow from financing activities for the period was reported at $1.06 million, as compared to cash out-flow of $29.92 million in the previous corresponding period.

The net capital expenditure (capex) of the company for the half year period was reported at $90.53 million, where expenditure for land and buildings stood at $72.44 million, plant and equipment stood at $10.98 million, and information technology at $7.11 million.

Capital Expenditure (Source: Company Reports)

Well-positioned for Post-lockdown Developments: On April 20, 2020, Mainfreight Limited (NZX: MFT) has provided the trading update as effects of the COVID-19 lockdowns, throughout 5 regions of the world where MFT is located, begin to weigh over the current trading patterns. The company stated that it has been deemed as an essential service provider throughout all its global operations, however, the differences in COVID-19 response levels, as well as in customer profiles, are providing varying financial results by region. With respect to New Zealand, the transport sales revenues witnessed a fall as non-essential freight was no longer available for the distribution purposes. However, as the definition of “essential products” broadens, the company is expecting volumes to improve. Warehouse storage revenue continues but pick activity has been reduced to essential products only.

Food and food-related product activity happens to be consistent with prior weeks. In Air & Ocean operations, normal air freight volume has been replaced with the air charter opportunities. The majority of these are committed, with important export volume into China, and with returns of PPE supplies. However, Australian air charters have been currently under negotiation. Sea freight imports are variable in volume and only the essential supplies are being able to be delivered. This might pose medium-term equipment supply issues for shipping industry for the important exports. The company has mentioned that NZ operations might witness difficult month of trading through April but are well-placed for the post-lockdown developments.

Reasonable Freight Volumes in Australia: As per the recent update, freight volumes are reasonable throughout all of its divisions within Australia, and a number of new customer gains are assisting. Inter-State distribution continues for the company’s transport operations and considering the high level of exposure towards supermarket and hardware retail sectors, the volumes are ahead of prior year. Coming to Warehousing operations, the products related to retail and restaurant sectors are slowing, but food and food-related products have been trading at regular levels of activity.

Initiatives To Focus Towards Reduction in Operating Expenditure: There are several initiatives which have been put in place in order to reduce and/or eliminate the unnecessary operating expenditure. Some of these are: 1) Usual annual wage and salary review has been deferred and hiring freeze is now in place, 2) Managing Director’s salary as well as other Directors’ fees have been reduced by 50% which would be in effect for the foreseeable future, 3) Government employment subsidies are under review and application is likely to be in NZ and some European countries, and 4) Reduction of unnecessary discretionary expense have been actioned.

Understanding MFT’s Overall Financial Position: As per the recent release, the debt facilities are at satisfactory levels and they are well supported by the company’s 6 banking partners. Its current debt facilities totalled $500 million, out of which $230 million remained undrawn as at March 31, 2020.

An amount of $415 million is maturing in the month of April 2024 and the balance of $85 million in the month of April 2022. Notably, net debt as at March 31, 2020 amounted to around $160 million. Capital expenditure (or Capex) of $120 million has been deferred. Committed capex amounted to $78 million for the current construction projects in 2021 financial year.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

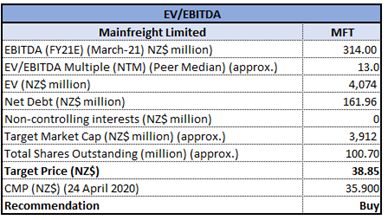

EV/EBITDA Based Relative Valuation

EV/EBITDA Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

What to Expect From MFT Moving Forward: The company’s trading through the month of April is expected to be significantly reduced on the YoY basis, although it has been shielded to some extent as the company’s global locations give a measure of sanctuary from the single country exposure. Also, additional financial leverage is available to the company if required. MFT’s balance sheet and debt facilities give sufficiently strong coverage in the current scenario. Moreover, the company happens to be well-positioned for the economic recovery.

The company’s China air freight volumes have been improving as demand for the air charters is increasing, particularly to the USA and Europe for PPE supplies. The company added that air freight pricing is increasing (excluding China), but normalising (excluding Hong Kong). The sea freight volumes (excluding China) have increased, though it seems like forward orders are now cancelling because of the delivery difficulties in the country of destination.

With respect to Americas, freight volumes were strongly consistent through March. The transport volumes have fallen by about 20%, and health care and home use products are still relatively strong. In warehousing division, the new customer implementation has continued, and activity levels are consistent.

In CaroTrans sea freight business, there has been an increase in the demand for LCL capacity. Revenue has been stronger than it was expected, and outlook for the month of April and May for the Americas is not as bad as was anticipated.

Technical Overview:

Weekly Chart –

Source: Thomson Reuters

Note: Purple colour lines are Bollinger Bands, yellow lines are retracement lines and orange colour dotted line is Paraboic SAR.

While remaining on multi-weeks of uptrend, the stock made the high of $44.27 and then it was caught under bearish trap pulling down the price to $23.89. From the low, the stock has shown smart recovery, retracing up beyond 61.8% retracement level of $36.48 and closing around 37.45 in the previous week. However, the just concluded week remained softer for the stock wherein it opened at the previous week close but closed lower at $35.90.

Technical indicators such as MACD with bearish cross-over but curve at end pointing up and RSI with reading around 46 suggest gaining of bullish momentum.

Stock Recommendation: With respect to capital management, the Board’s objective revolves around ensuring that the entity continues as a going concern and to maintain optimal returns to the shareholders and benefits for other stakeholders. The Board also focuses towards maintaining a capital structure which ensures the lowest cost of capital available. The Board is periodically reviewing as well as adjusting its capital structure in order to take benefits of favourable costs of capital.

Considering the above facts, we have valued the stock using EV/EBITDA based relative valuation (on an illustrative basis) and the target price reflects a growth of higher single-digit (in % terms).

Thus, we give a “Buy” rating on the stock at the current market price of NZ$35.900 per share, down by 0.88% on April 24, 2020.

.png)

MFT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...