Sector Landscape

During 2019 to 2020, the government alone managed $1.04 billion of spending on medicines, facilitating 3.77 million Kiwis. In 2019 to 2020, it has funded 14 new medicines, 32 medicines with widened access, achieved $87.4 million saving to reinvest in medicine, and ~71,245 number of additional patients benefitting from new funded medicines. The government currently fund nearly 1,000 different medicines (in over 2,000 different preparations), which is available in hospitals and at local pharmacies. The government filled 47.6 million prescriptions to provide required healthcare support to people living in New Zealand. The government has employed ~140 experienced clinical experts to provide advice and assess all the scientific evidence.

There are various ways to garner healthcare services In New Zealand which spans across public and private healthcare system. Apart from this, one can also seek medical assistance from general practitioner, who is a fully trained medical doctor. With more than 35,000 General Practitioners present in the country who are based in almost every city, town and suburb. A general practitioner can also provide medical advice to patients for treatment and can also refer in case of any further requirement of specific tests or treatment, which can be done from both public healthcare system as well as private providers. While the treatment through public healthcare system which offers essential healthcare services that includes emergency care, essential surgery, and hospital care at a subsidised rate or free of costs, in case of private healthcare service providers, the users are required to borne the costs of the treatment.

New Zealand’s spending on healthcare system is significant ~10% of its GDP, which is slightly higher than the OECD average. Most of the spending is contributed towards the public healthcare which accounts for 83% of the total spend, providing healthcare services through 220 hospitals and 20 District Health Boards which are spread across different regions.

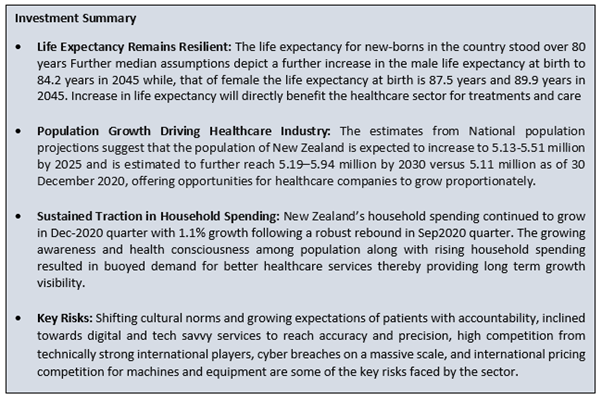

Exhibit 1: S&P/NZX All Health Care (Sector) v/s S&P/NZX All Index (One-Year Chart) *

Source: S&P Global; Chart Created by Kalkine Group

*Till March 25, 2021

The S&P/NZX All Healthcare sector has outperformed the S&P/NZX All Index with a 3-year return (26 March 2018 - 25 March 2021) of 23.14% as against the index’s 3-year return of 10.16%.

Household Spending on a Rise

Although the New Zealand economy contacted by 1.0% in the December 2020 quarter following a record rebound of 13.9% (revised) in the September 2020 quarter, the country however continues to witness traction in the household spending. Sustaining the robust rebounds in the previous quarter, the household spending in the December quarter increased by 1.1% supported by 3.8% growth in spending on services. The growing awareness and rising health consciousness among population amid demand for better healthcare services provides long term growth visibility for the sector.

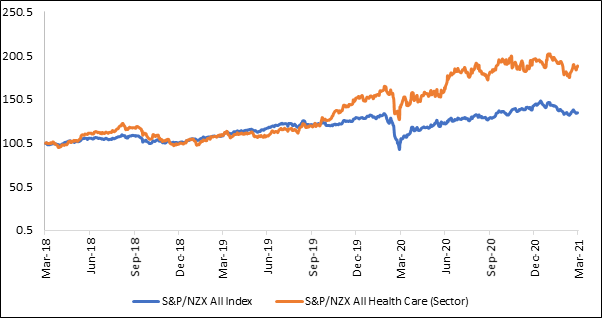

Wellbeing Statistics Portrays a Bright Picture

Exhibit 2: Self-Rated General Health Status Remain High

Source: stats.govt.nz; Chart Created by Kalkine Group

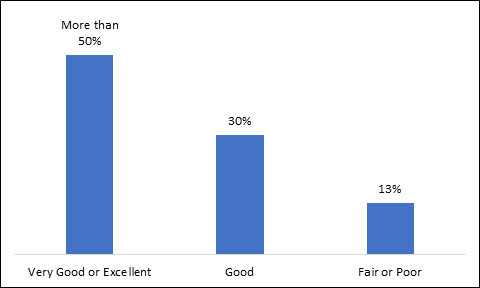

Reduction in Abortion Rate

As per New Zealand Stats, the overall abortions done in the country reduced by around 3% in 2019 to 12,857 from 13,282 in 2018. Of which, 64% of the abortions were accounted for woman’s first abortion performed, while woman with twice abortions was reported at 23% and the rest was accounted for two or more abortions. Albeit the country’s general abortion rate which takes into consideration the abortions per 1,000 women with age between 15–44 years reduced to 13.1 in 2019 as compared to 13.7 in 2018. However, the same has significantly lowered from 19.3 in 2009.

Exhibit 3: General Abortion Rates in a Declining Trend

Source: stats.govt.nz; Chart Created by Kalkine Group

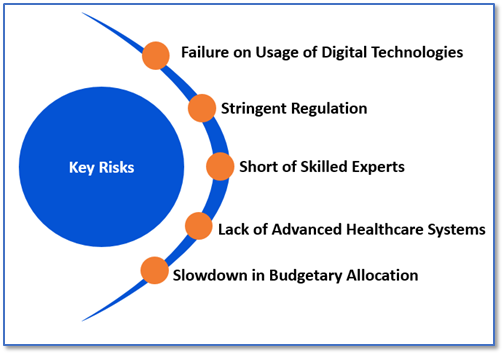

Key Risks and Challenges:

Albeit the country’s ageing population has been driving its healthcare sector, however, its citizens expect the public healthcare system to provide high standard of products and services at an affordable rate. Further growing incidence of long-term and chronic conditions among ageing population requires access to advanced equipment as chronic diseases comprise of around 80% of healthcare use. Broadly key risks can be identified as shifting culture norms and growing expectations of patients with accountability, inclined towards digital and tech savvy to reach accuracy and precision, high competition from international players who are advanced in technology and innovation, cyber breaches on a massive scale, international pricing competition for machines and equipment.

Moreover, the sector is weighed down by the risk of skills shortage in the country in view of robust demand. The hospitals and practices across the country rely on immigration to fill the gap in the niche skill set owing to the dearth of required skills in the field of doctors, midwives, surgeons and other healthcare occupations. The estimates foretell the requirements of additional 380 extra specialists annually to meet the OECD average by 2021. Moreover, estimates also suggests that New Zealand healthcare sector requires around 25,000 more nurses by 2030.

Exhibit 4: Key Risks in Healthcare Sector:

Outlook

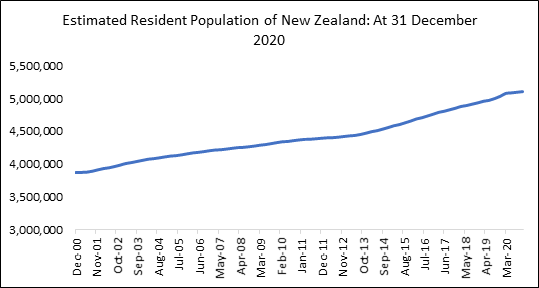

As per the estimates from National population, the population of New Zealand is likely to increase to 5.13-5.51 million by 2025 and is estimated to further reach 5.19–5.94 million by 2030 versus 5.11 million as of 30 December 2020 which propels buoyed demand for quality healthcare.

Further the birth rates are expected to remain robust as the country witnessed 57,573 live births in the year ended December 2020, although it was down by 3.5% YoY. While the death rate during the said period reduced by 1,647 to 32,613. This resulted in a net rise i.e., natural increase (live births minus deaths) of 24,960 during the period under consideration. Further, recent data from Stats NZ suggests that the life expectancy for new-born boys and girls stood at more than 80 years with the life expectancy for a new-born boy on average stood at 80.3 years, and that of a new-born girl at 83.9 years. Besides, the overall fertility rate of the country reached a record low level of 1.61 in 2020 as against the annual average of 1.97 over the last 30 years.

Overall, the prospects for the sector remains bright. Besides, with the benefits of the country’s unique public health and no-fault accident compensation system, which covers the whole demography through-out their lifespan also provides visibility on the sustainability of the growth momentum.

Exhibit 5: Estimated Resident Population of New Zealand: Building Momentum for Future Growth

Source: stats.govt.nz; Chart Created by Kalkine Group

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

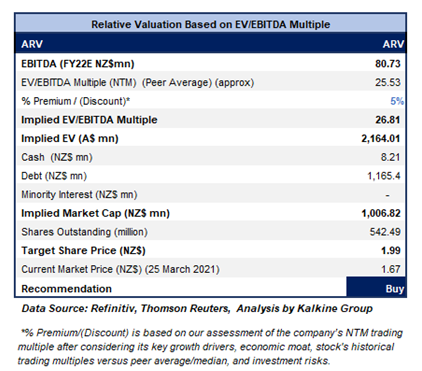

1) Arvida Group Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$905.955 million, Gross Dividend Yield: 3.193%)

Business Description:

Arvida Group Ltd (NZX: ARV) is one of the leading operators of the aged care facilities as well as retirement villages in NZ. ARV has 32 retirement communities spread across New Zealand, with a range of living options to cater the specific requirements.

Outlook

ARV is on an expansion mode driven by continued sales momentum. ARV is on track to complete 247 units/beds in FY21. Of which 29 apartments and 55 care suites of the new Copper Crest care suite centre in Tauranga are to be delivered in Q4FY21. Further the new care and apartments wing at St Albans in Christchurch is scheduled to be deliver on Q4FY21. Moreover, it is eyeing to deliver more than 200 units in FY22, reflects continued strong sales activity. Besides the company is also looking at continued acquisition opportunities, including well located greenfield land opportunities. Considering continued buoyancy in the property market, high care occupancy and an underlying positive organisational culture, bodes well for growth going ahead.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

Considering its sustained high care occupancy level, continued sales momentum, and robust growth plans, we give a “Buy” recommendation on the stock at the current market price of $1.67 per share, up by 0.60% on 25th March 2021.

2) Rua Bioscience Ltd (Recommendation: Spec-Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$59.612 million)

Business Description:

Based in New Zealand, Rua Bioscience Ltd (NZX: RUA) is engaged in pharmaceutical business and is targeting to be a leading producer of cannabinoid derived medicines for both domestic as well as export markets.

Outlook:

The company focuses on executing on its export-led strategy in order to deliver sustainable revenue. With the securing of binding sales agreement with one of Germany’s leading distributors of medicinal cannabis - Nimbus Health, the company is focusing on export led strategy and it expects its first wholesale exports of dried cannabis flower to happen by the end of 2021. The IPO proceeds will enable the company to chart out growth as it utilised the IPO proceeds of $20 million towards Rua’s strategic priority areas which support the achievement of sustainable revenue and accelerate growth. In a major milestone, the company has commenced export of a sample of medicinal cannabis flower to Germany.

Technical Overview

Weekly Chart

(Source: Refinitiv (Thomson Reuters))

Note: Yellow line indicates Fibonacci Retracement levels, while Orange color lines represents trend lines. Purple line shows the RSI (14-period) and the green color histograms at the bottom of the chart indicating weekly volumes.

RUA is broadly trading in a falling wedge pattern and continuously drifting to its 52 weeks lowest levels. Prices broke the major support level of NZ$ 0.52 in the latter half of February 2021 and have achieved its targets of NZ$ 0.4277 levels according to the Fibonacci golden ratio 161.8% levels. Positive divergence in RSI can be seen on charts where prices are making lower lows but subsequently RSI is making higher lows that indicates bullish sign for the stock prices. RSI (14) is trading at oversold region ~27 that indicates short covering might happen. Volumes are decreasing with falling prices which indicates the current prices trend might recover from supporting levels. Immediate support levels are NZ$ 0.4155 and NZ$ 0.4090 while resistance levels appears to be at NZ$ 0.4624 and NZ$ 0.520.

Stock Recommendation

The stock has decreased by ~16.67% in 1 month and ~29.17% in 3 months, thereby providing an opportunity to enter at lower levels. Besides, the company has sound fundamentals and focuses on executing on its export-led strategy to deliver sustainable revenue.

Considering its competitive edge as it is the first private company in New Zealand to receive a license to cultivate cannabis for research purpose along with its strong liquidity profile and decent outlook, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.425 per share, down by 1.16% on 25th March 2021.

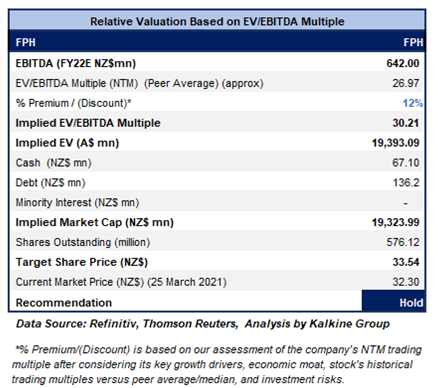

3) Fisher & Paykel Healthcare Corporation Limited (Recommendation: Hold, Potential Upside: Low Single-Digit) (M-Cap: NZ$18.617 billion, Gross Dividend Yield: 1.393%)

Business Description:

Fisher & Paykel Healthcare Corporation Limited (NZX: FPH) is engaged in designing, manufacturing, and marketing of products and systems which finds usage in surgery, acute care, respiratory care, and the treatment of obstructive sleep apnea.

Outlook

The company has commenced planning on its third manufacturing facility in Tijuana, Mexico, which is expected to be ready for occupancy in FY23. The company’s hospital hardware sales continued to gain traction driven by the increasing hospitalisation rates for COVID-19. Resultantly, it garnered 73% YoY growth in its operating revenue for the nine months ended 31 December 2020.

Meanwhile, FPH recently has guided its FY21 revenue and net profit after tax to be higher than earlier estimated. The company at the time of release of its half yearly results has guided its FY21 operating revenue to be ~$1.72 billion and net profit after tax to be between $400 million to $415 million on the back of assumptions that the use of hospital hardware and sales return to a normal level and continued robust Hospital hardware sales to date.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

We have applied EV/EBITDA based relative valuation (on an illustrative basis) and the target price reflects a rise of low single-digit (in % terms). We have applied a premium EV/EBITDA Multiple (NTM) (Peer Average) considering the commenced planning on its third manufacturing facility in Tijuana, Mexico, which is expected to be ready for occupancy in FY23, strong growth in its products used for nasal high flow therapy in the home, continued traction in Hospital hardware sales and usage.

Considering the expected upside, robust balance sheet, and decent outlook we give a “Hold” recommendation on the stock at the current market price of NZ$32.30 per share, up by 2.87% on 25th March 2021.

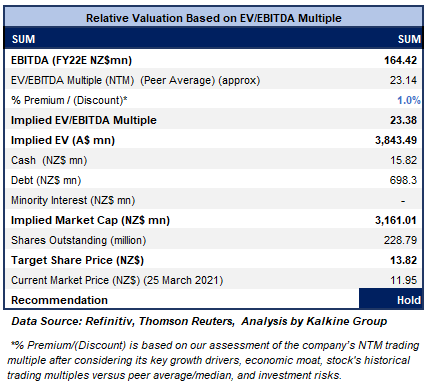

4) Summerset Group Holdings Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$2.74 billion, Gross Dividend Yield: 1.076%)

Business Description:

Summerset Group Holdings Ltd (NZX: SUM) is engaged in providing retirement village and aged care services. The company has 31 retirement villages which are either completed or in development phase with more than 5,700 residents residing in those retirement villages. Besides, SUM has a robust portfolio of retirement units with 901 care beds under its kitty.

Outlook

The company has delivered a resilient performance in FY20 on the backdrop of the COVID-19 pandemic which reflects the underlying strength of Summerset’s business. The company owned the largest land bank in the sector. Going ahead, SUM is lined up with launch of the main buildings in its Richmond (Nelson) and Avonhead (Christchurch) retirement villages in 2021. Further it is likely to launch apartment blocks in Kenepuru. SUM is anticipating the FY21 build rate in New Zealand in the range of 500 and 550 units and 50 care beds.

Moreover, the company is on an expansion with the recent acquisition of property in the desirable suburb of Chirnside Park, northeast Melbourne, which marks the company’s third acquisition in Victoria since September 2019.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

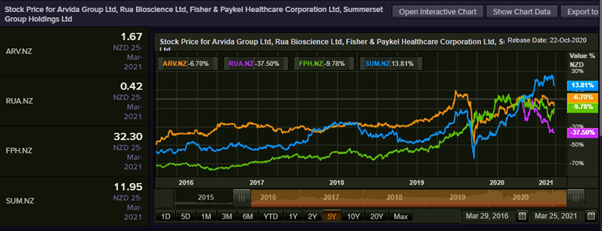

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...