Company Overview: Kiwi Property Group Limited (NZX: KPG) is engaged in investing in New Zealand real estate. The Company's primary assets are investment properties in the retail and office sectors. Its investment objective is to provide investors with an investment in New Zealand property, focusing on risk-adjusted returns over time through the ownership and management of a diversified portfolio. Its property investment portfolio comprises retail portfolio, which includes regional shopping centers and large format retail within and outside Auckland region, and office portfolio that includes office properties with floorplate, services, location and car parking in Auckland, and core government office accommodation supported by long-term leases to the government in Wellington. Its portfolio includes properties, such as Sylvia Park, LynnMall, Westgate Lifestyle, The Base, North City, Vero Centre and The Aurora Centre, among others.

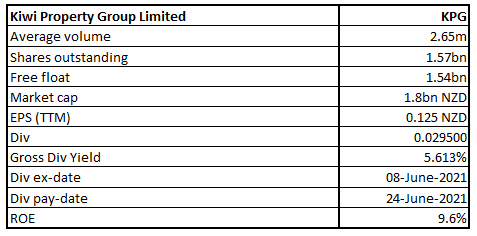

KPG Details

Kiwi Property Group Limited (NZX: KPG) is the largest listed property company listed on the New Zealand Stock Exchange. It owns and manages a significant real estate portfolio, comprising of best mixed-use, retail, and office buildings. The company has a market capitalization of ~$1.8 billion as on June 21, 2021.

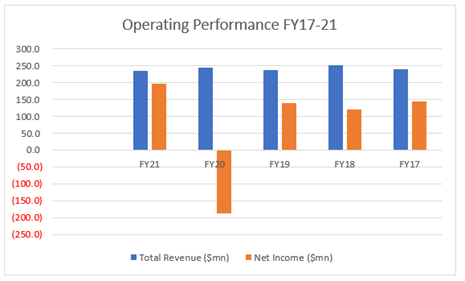

The company registered growth in bottom-line at CAGR of 8.27% over FY17 to FY21. The company’s net income increased from $143.0 million in FY17 to $196.5 million in FY21.

Exhibit 1: Historical Operating Performance

Source: Analysis by Kalkine Group, Company Reports

Results Performance (Year Ended March 31, 2021)

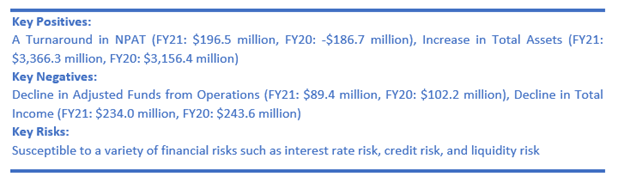

The company reported a turnaround in the net profit after tax at a positive $196.5 million for the year as against negative $186.7 million in the previous year, supported by growth in value of the investment properties. However, the costs of asset lockdowns and the associated rent relief measures caused net rental income to decline by 7.1% YoY to $173.6 million. In line with a decline in rental income, operating profit before tax declined by 10.3% YoY to $116.3 million. The company’s office assets performed strongly delivering a 10.2% YoY fair value gain, while mixed-use was up 1.5% YoY. On 31 March 2021, KPG’s property portfolio was valued at $3.3 billion.

The company maintained a strong balance sheet throughout FY21 and ended the year with a gearing of 31.2%, comfortably within its self-imposed range of 25-35%.

The Board of Directors declared a final dividend of 2.95 cents per share (cps), taking the full-year dividend to 5.15 cps, equivalent to 90% of Adjusted Funds from Operations (AFFO). Payment will be made on 24 June 2021.

Exhibit 2: Income Statement

(Source: Company Reports)

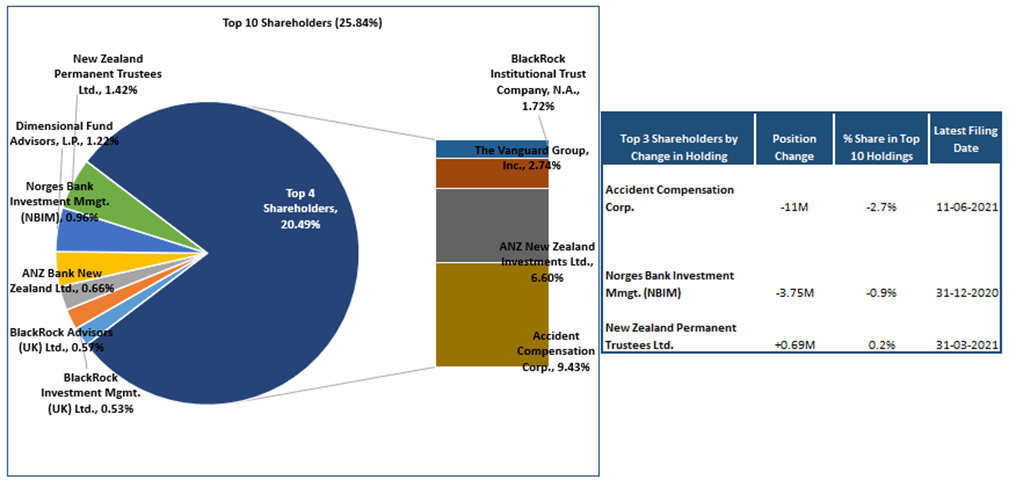

Top 10 Shareholders: The top 10 shareholders have been highlighted in the pie chart below, which together form around 25.84% of the total shareholding. Accident Compensation Corporation and ANZ New Zealand Investments Limited are holding a maximum stake in the company at 9.43% and 6.60%, respectively, as provided in the table below:

Exhibit 3: Top 10 Shareholders

(Source: REFINITIV)

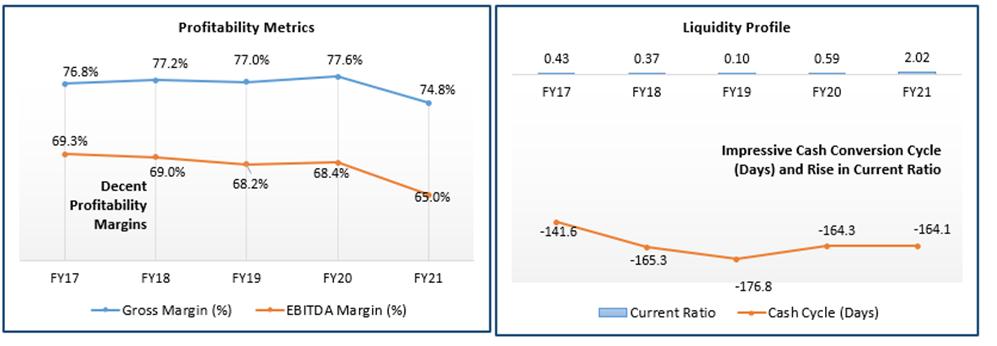

A Quick Look at Key Metrics: The company’s gross margin and EBITDA margin for FY21 stood at 74.8% and 65.0%, respectively. However, the liquidity profile of the company registered an improvement in FY21 over FY20 with the current ratio increasing to 2.02x and the cash conversion cycle declining to 164.1 days.

Exhibit 4: Key Metrics

(Source: REFINITIV)

Outlook:

KPG has entered FY22 with good momentum and a clear focus on achieving its strategic priorities of reducing its retail exposure and continue to create mixed-use spaces. Some of the major developments to look for in the coming period include Drury, the new office tower at Sylvia Park and the opportunity with BTR. Flagship store opening continues to strengthen retail offerings. International retailers including JD Sports and Culture King is expected to further strengthen retail offerings. KPG is focused on realising these and other opportunities, with a continued commitment to creating value for its stakeholders.

The company is expected to provide AFFO guidance once the sale of The Plaza and Northlands get concluded. However, based on current projections, the FY22 dividend is expected to be no less than 5.30 cents per share, subject to the financial performance of the company.

Recent Updates:

In the release dated 14th June 2021, the company has announced the appointment of Angela Henderson to the role of GM Digital. This role has been newly created.

In the release dated 2nd June 2021, KPG has made an announcement about the appointment of Chris Aiken to its Board as the Non-Executive Director.

Key Risks:

The company’s financial performance could be adversely impacted provided concerns on mutant COVID-19 pandemic linger which has the potential of dampening business sentiment. Besides, heating of economy may result in tightening of interest rate sooner than expected which could have an adverse impact on sales and profitability of the company.

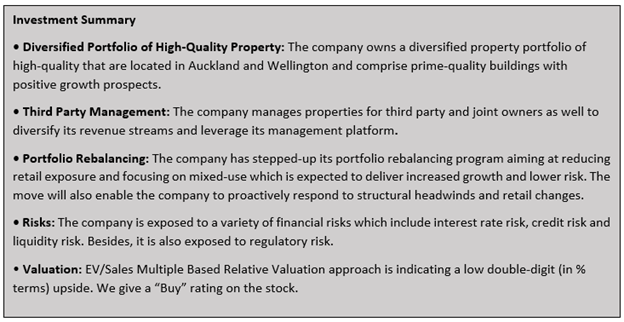

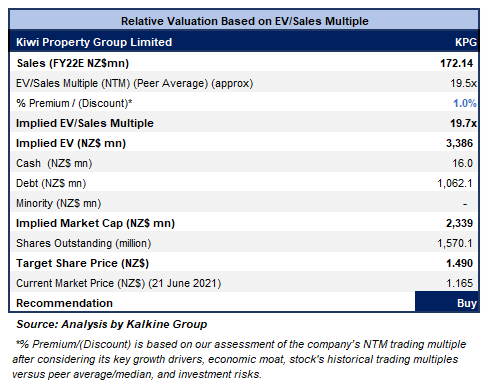

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock from its low of $0.73, retraced up to the 61.8% retracement level where it made a ‘Double Top’ and fell. On the first trading session of the ongoing week, the stock experienced low volatility and finally gave a close with a gain of 0.43% over the previous week’s close at $1.165. The technical indicator RSI with a reading of 41 and a curve at the end pointing up, suggests neutral to up momentum.

Going forward, the stock may have resistance around 20 periods SMA of $1.2190 whereas support could be around the 38.2% retracement level of $1.102.

Stock Recommendation:

The company has stepped up its portfolio rebalancing program in FY21, with the aim of reducing the company’s exposure to retail and recycling capital to help fund its growth pipeline. ROE for FY21 stood at 9.6%, better than the industry median of 5.6%, implying that the company generated better returns for its shareholders than its peer group. The current ratio for FY21 stood at 2.02x, better than the industry median of 0.69x, implying that the company possesses better capabilities to meet its short-term obligations than its peer group. Its return on invested capital for FY21 stood at 6.3%.

We have applied EV/Sales multiple-based relative valuation (on an illustrative basis) and there are expectations that the stock price might witness a rise of a low double-digit (in % terms). We have applied a slight premium to EV/Sales Multiple (NTM) (Peer Average) considering significant growth in NPAT and its focus towards achieving the strategic priorities.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of NZ$1.165 per share, up by 0.43% on June 21, 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...