Company Overview: Kiwi Property Group Limited, formerly Kiwi Income Property Trust, is engaged in investing in New Zealand real estate. The Company's primary assets are investment properties in retail and office sectors. Its segments are Retail, Office and Other. Its investment objective is to provide investors with an investment in New Zealand property, focusing on risk-adjusted returns over time through the ownership and management of a diversified portfolio. It is focused on property investment portfolio comprising retail portfolio, which includes regional shopping centers and large format retail within and outside Auckland region, and office portfolio that includes office properties with floorplate, services, location and car parking in Auckland, and core government office accommodation supported by long-term leases to government in Wellington. Its portfolio includes properties, such as Sylvia Park, LynnMall, Westgate Lifestyle, The Base, North City, Vero Centre and The Aurora Centre, among others.

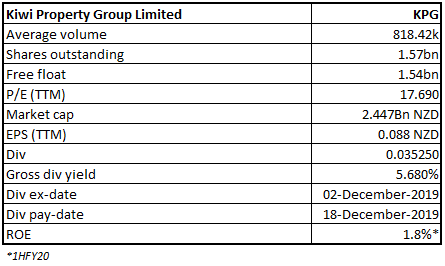

KPG Details

1HFY20 Results Driven by Strong Rental Income: Kiwi Property Group Limited (NZX: KPG) is the biggest listed property company on the New Zealand Stock Exchange, which manages a $3.3 billion portfolio of real estate, including some of New Zealand’s best mixed-use, retail and office buildings. The company aims to offer investors with a trustworthy investment in New Zealand property through the ownership and active management of a diversified, high-quality portfolio. The market capitalisation of the company stood at ~$2.447 billion on 10th February 2020.

The company reported its financial result for the six months ended 30th September 2019, comprising an improvement in rental operation across the half-year. It reported total rental growth of 4.6%, keeping pace with the previous period's solid growth momentum. The solid rental growth was driven by the demand for space at leading mixed-use and retail sites, as well as premium grade office buildings. New leases and renewals were particularly pleasant, with the office up 8.5%, retail up 0.8% and mixed-use up 14.1%. However, the net rental income was slightly lower as compared to last year to $89.6 million, impacted by the sale of North City in the comparative period. On like for like basis, the net rental income grew by $1.8 million or 2.1%.

Positive Retail Sales (Source: Company Reports)

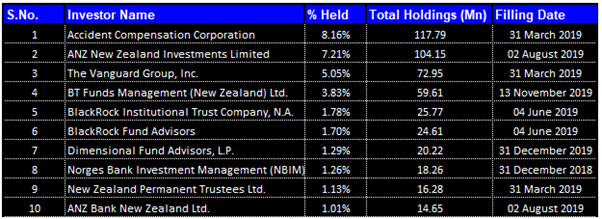

Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Kiwi Property Group Limited. Accident Compensation Corporation is the largest shareholder with a percentage holding of 8.16%.

Top 10 Shareholders (Source: Thomson Reuters)

Bottom-Line Impacted by One-Offs and Interest Rates: The company reported Funds from Operations (FFO) of $51.9 million in 1H FY 2020, slightly below the previous year, impacted by one-off disposals in FY19. Net profit after tax also declined to $36.8 million due to a fair value loss of $12.9 million in the value of Kiwi Property’s interest rate swaps, after successive interest rate cuts. On the contrary, these cuts are having a positive effect on the company’s weighted average cost of debt.

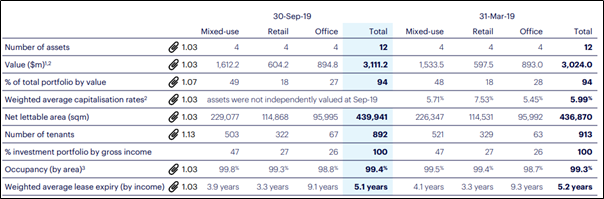

Robust Financial Position of the Company: The company kept its robust balance sheet through 1HFY20, boosting the value of its portfolio to $3.3 billion. Also, the company made strategic acquisitions at 51-53 Carbine Road and 7-10 Arthur Brown Place, at a combined cost of $25.5 million. The assets are adjacent to the Sylvia Park train station, offering the company access to both sides of the railway line and establishing a substantial scope for future mixed-use development.

Property Portfolio Summary (Source: Company Reports)

Successful Equity Raise to Support Development Pipeline: The company undertook a successful equity raise after the half-year balance date, raising gross proceeds of $180 million. The placement was strongly supported by a broad range of new and existing investors from both local and offshore markets. The company is also targeting a $20 million retail offer, with the ability to accept oversubscriptions of up to $10 million. The new equity will allow the company to reduce pro-forma gearing below 30% and create additional capacity to fund the development pipeline and engage in new acquisition opportunities.

Appointment of Simon Shakesheff as Non-Executive Director: The company has appointed Simon Shakesheff to its Board as a Non-Executive Director. Simon is a recognised leader in Australia’s property finance sector and has a 30-year executive career covering several of the country’s most prolific property groups as well as investment banks.

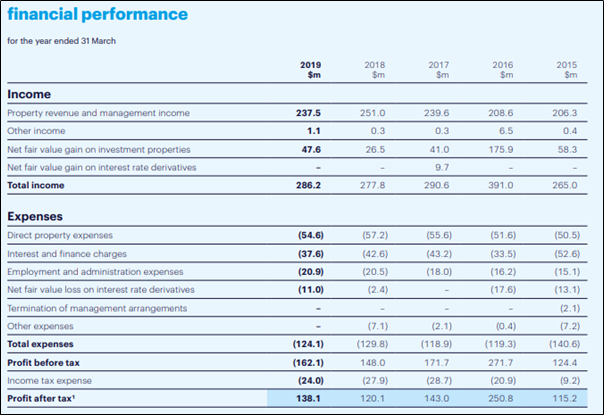

Strong FY19 Results Driven by Robust Revaluation Performance: The company reported a profit after tax of $138.1 million for the year ended 31st March 2019, up from $120.1 million in the prior year, driven mainly by a stronger revaluation performance from a high-quality portfolio of assets. The company’s key measure of operating performance, FFO was $106.9 million. It was down from $111.3 million in the prior year due to the short-term impact associated with selling two non-core assets and reinvesting the proceeds into superior development opportunities at Sylvia Park in Auckland. The company has declared a final cash dividend of 3.475 cents per share, taking the full-year cash dividend to 6.95 cents per share, in line with guidance and up from 6.85 cents per share in the prior year.

Five Year Summary (Source: Company Reports)

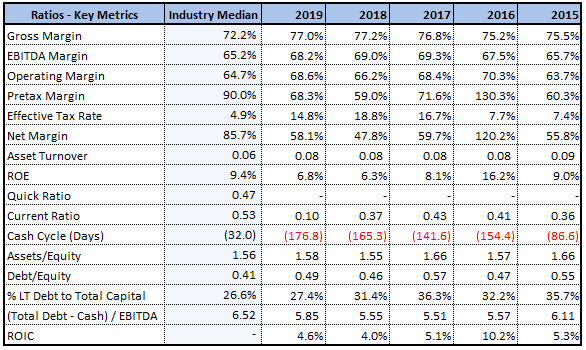

Increasing Returns to Shareholders: In FY19, the company’s gross margins stood at 77.0%, which is better than the industry median of 72.2%. The company’s EBITDA margin stood at 68.2% in FY19, which is above the industry median of 65.2%. The company has also seen an increase in its net margin, from 47.8% in FY18 to 58.1% in FY19. During FY19, Return on Equity stood at 6.8%, up from 6.3% in FY18. This reflects that the company has been delivering decent returns to its shareholders.

Key Metrics (Source: Thomson Reuters)

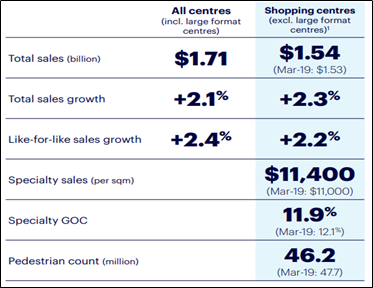

Strong Portfolio Performance: The company’s portfolio of mixed-use, retail and office assets continue to perform strongly. At year-end, the portfolio was 99.3% occupied, with a healthy weighted average lease expiry of 5.2 years. For the year ended 31st March 2019, total retail sales from shopping centre assets were $1.53 billion, up 2.0% (2.4% like-for-like), with specialty sales productivity-improving to $11,000 per square metre. Total retail sales, including those from large format centres, were $1.70 billion.

Update on the Development Pipeline: During FY19, the company delivered its first office building at Sylvia Park, ‘ANZ Raranga’ and the dining development, Langdons Quarter, at Northlands in Christchurch. It completed the first of two new multi-level carparks at Sylvia Park, and construction activity for the arrival of a new Kmart store, together with major Sylvia Park galleria retail expansion, is well in train. The company has decided to expand its galleria retail development at Sylvia Park. An increase in the net lettable area will accommodate key tenants who want to be in this location. The expansion increases the project cost by $35 million to $258 million, and the company has maintained key yield metrics and increased the projected development profit to 13% of the project cost.

Outlook for Full Year FY20: The company is in a strong position to capitalise on New Zealand’s continued growth. The company’s new funds management and property investment teams will focus on examining market opportunities, while its asset management team will continue to drive the operational performance of property assets. Supportive economic and property market fundamentals, in combination with strong portfolio metrics, provide with confidence the company will continue to deliver a strong financial performance. As per the release, for 2H FY 2020, it will pay a half-year cash dividend of 3.525 cents per share, up 1.4% on last year. The company also confirmed its intention to hold its full-year cash dividend at 7.05 cents per share.

Key Valuation Metrics (Source: Thomson Reuters)

Price to Earnings-Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Technical Overview:

Monthly Chart -

Monthly Chart (Source: Thomson Reuters)

Weekly Chart -

Weekly Chart (Source: Thomson Reuters)

Daily Chart -

Daily Chart (Source: Thomson Reuters)

Note: Purple colour lines are Bollinger bands, yellow colour horizontal lines are retracement levels and orange colour dotted line are Parabolic SAR.

The stock is trading below 20 periods SMA on weekly and daily charts but above the same on monthly chart thereby exhibiting near-term weakness but strength in medium-term to long-term. Bullish cross-over for MACD on monthly and daily charts and RSI reading above 50 suggest positive momentum to continue in medium-term.

In the past three months, the stock tried twice to break 50% retracement level of $1.60 but failed. Thus, $1.60 should act as an initial resistance for the stock. However, on breach above, stock may even move around $1.70. On the downside, stock may have good support at around $1.50.

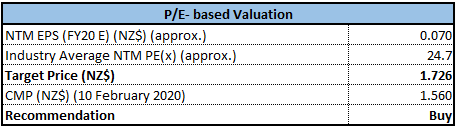

Stock Recommendation: The stock of KPG gave a return of 1.29% and 1.62% in the past one month and nine months respectively and is trading slightly below its average of 52-weeks’ low high level of $1.4 and $1.7. This offers a decent opportunity for the shareholders to enter the market and benefit from accumulation. The company has a well-defined structure for future growth. Considering the better margins than the industry, current trading levels and decent outlook, we have valued the stock using a relative valuation method, i.e., Price to Earnings multiple and have arrived at a target price of lower double-digit growth (in percentage terms). We have considered Goodman Property Trust (NZX: GMT), Argosy Property Ltd (NZX: ARG), Property for Industry Ltd (NZX: PFI), Stride Property Ltd (NZX: SPG) and Investore Property Ltd (NZX: IPL) as a peer group. Hence, we recommend a “Buy” rating on the stock at the current market price of $1.560.

KPG Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...