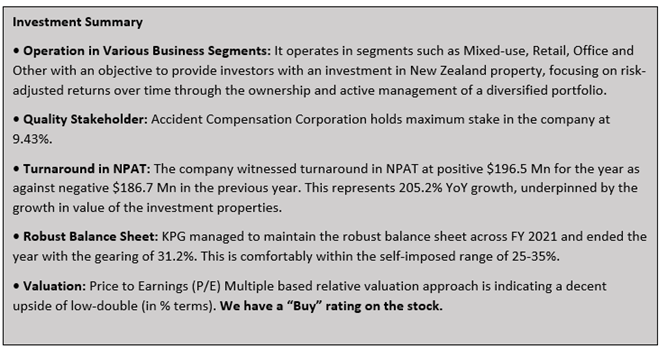

Company Overview: Kiwi Property Group Limited (NZX: KPG), formerly Kiwi Income Property Trust, is engaged in investing in New Zealand real estate. The Company's primary assets are investment properties. Its reportable segments are Mixed-use, Retail, Office and Other. Its investment objective is to provide investors with an investment in New Zealand property, focusing on risk-adjusted returns over time through the ownership and active management of a diversified portfolio. It is focused on property investment portfolio comprising retail portfolio, which includes regional shopping centers and large format retail within and outside Auckland region, and office portfolio that includes office properties with floorplate, services, location and car parking in Auckland, and core government office accommodation supported by long-term leases to government in Wellington. Its portfolio includes properties, such as Sylvia Park, LynnMall, Westgate Lifestyle, The Base, North City, Vero Centre and The Aurora Centre, among others.

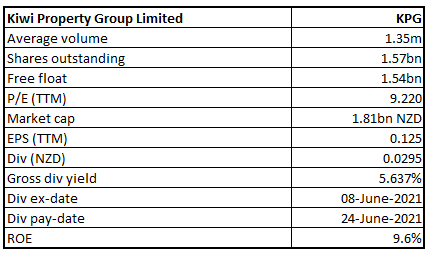

KPG Details

Kiwi Property Group Limited (NZX: KPG) is the largest listed property company on the New Zealand Stock Exchange. It owns and manages a significant real estate portfolio. The company has a market capitalization of ~$1.81 billion as on 4th October 2021.

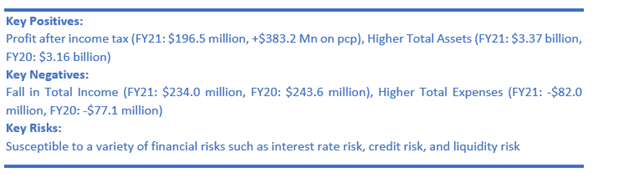

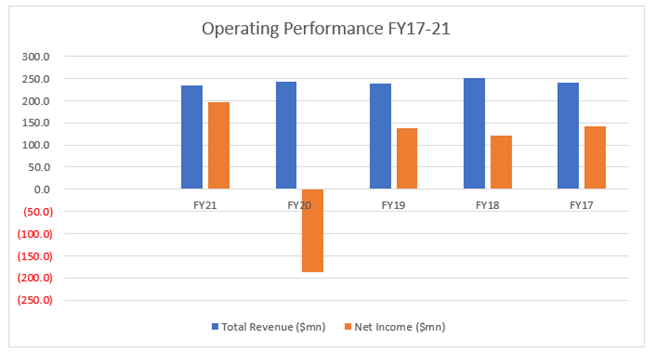

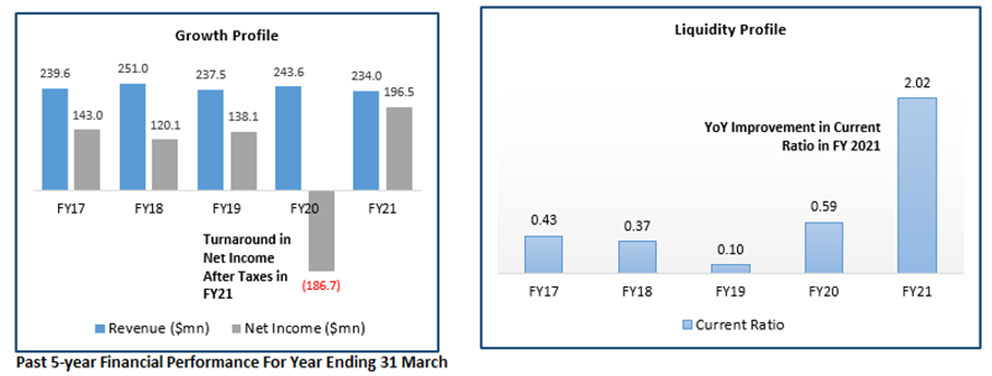

The company registered growth in bottom-line at CAGR of 8.27% over FY17 to FY21. The company’s net income increased from $143.0 million in FY17 to $196.5 million in FY21.

Exhibit 1: Historical Operating Performance

Source: Company Reports, Analysis by Kalkine Group

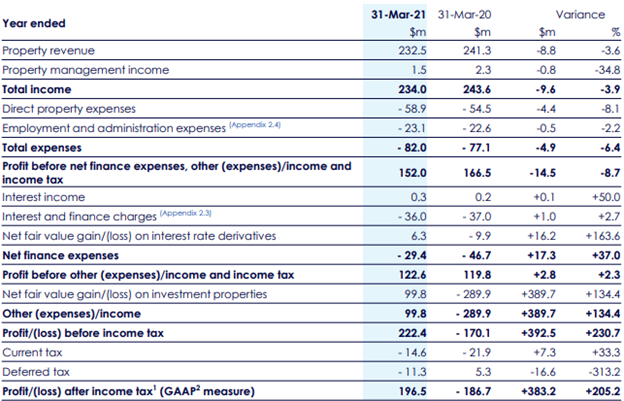

Results Performance (Year Ended March 31, 2021)

Exhibit 2: Income Statement

(Source: Company Reports)

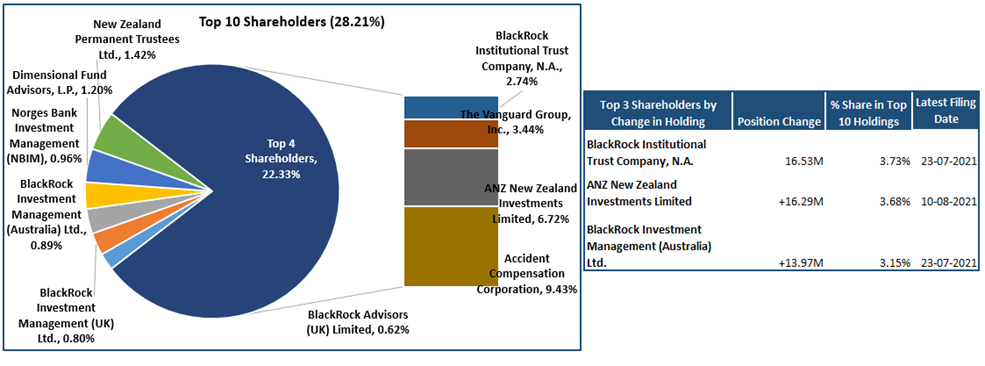

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 28.21% of the total shareholding. Accident Compensation Corporation and ANZ New Zealand Investments Limited are holding maximum stake in the company at 9.43% and 6.72%, respectively, as provided in the table below:

Exhibit 3: Top 10 Shareholders

Source: Analysis by Kalkine Group

A Quick Look at Key Metrics: The company’s gross margin and net margin for FY21 stood at 74.8% and 84.0%, better than the industry median of 69.2% and 48.4%, respectively, implying greater efficiency in managing operating and non-operating costs than the peer group. ROE for FY21 stood at 9.6%, better than the industry median of 6.7%, implying that the company generated better return for its shareholders than its peer group. Current ratio for FY21 stood at 2.02x, better than the industry median of 0.75x, implying that the company possesses better capabilities to meet its short-term obligations than its peer group. Its return on invested capital for FY21 stood at 6.3%.

Exhibit 4: Key Metrics

Source: Analysis by Kalkine Group

Recent Updates:

Outlook:

FY22 Dividend Expected at least 5.30 cps: The company is expected to provide AFFO guidance once the sale of The Plaza and Northlands has concluded, however based on current projections, the FY22 dividend is expected to be no less than 5.30 cents per share, subject to the financial performance of the company and barring material adverse effects or unforeseen circumstances, such as further COVID-19 related lockdowns. KPG has entered FY22 with good momentum and a clear focus on achieving its strategic priorities.

Key Risks:

The company’s financial performance could be adversely impacted due to COVID-19 pandemic and could affect its net rental income. Notably, operating profit before tax could also witness some impacts.

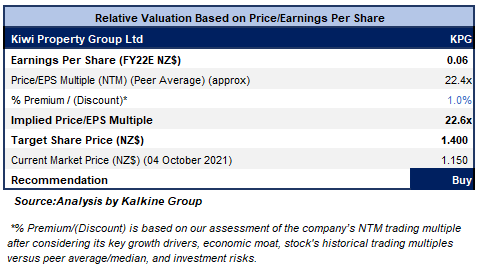

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

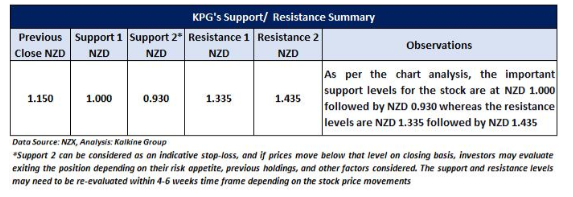

Technical Overview:

Chart:

Source: REFINITIV

Note: Orange Color Line Reflects RSI (14-Period)

Stock Recommendation:

The company stepped-up its portfolio rebalancing programme in FY21, with the aim of reducing the company’s exposure to regional retail and recycling capital to help fund its growth pipeline.

The stock has been valued using a Price/Earnings Per Share multiple based illustrative relative valuation method and arrived at a target price which reflects the rise of low double-digit (in percentage terms). The company might trade at a slight premium to its peers’ average considering turnaround in NPAT as well as decent outlook.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of NZ$1.150 per share, down by 0.43% on 4th October 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...