Company Overview: With over 25 years of experience, Kiwi Property Group Limited (NZX: KPG) is the leading listed property company in New Zealand, managing ~$3.1 billion portfolio of real estate, comprising some of New Zealand’s best mixed-use, retail and office buildings. The company’s objective is to provide investors with a reliable investment in New Zealand property through ownership and active management of a diaversified and high-quality portfolio. Notably, Kiwi Property is a member of NZX15 Index.

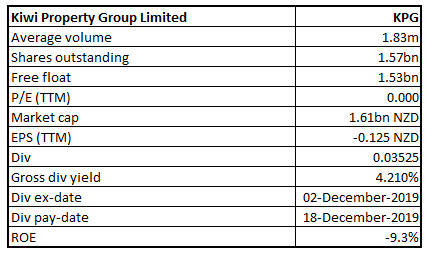

KPG Details

Investment Summary:

‘Zero’ New Covid-19 Cases in NZ to Re-energize Business Activities: Kiwi Property Group Limited (NZX: KPG) happens to be a leading property company that is listed on New Zealand Stock Exchange. The company has a market capitalisation of around $1.60 billion as on June 15, 2020. S&P Global Ratings has assigned Kiwi Property an issuer credit rating of BBB (stable) and an issuer credit rating of BBB+ for each of its fixed rate senior secured bonds.

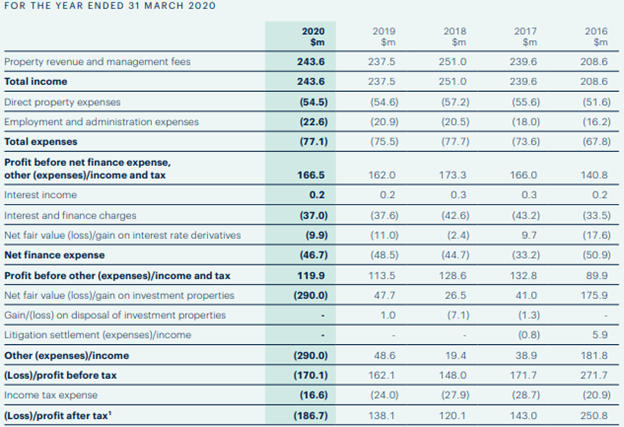

The company registered growth in top-line at CAGR of 3.95% over FY16 to FY20. The company’s total revenue increased from $208.6 million in FY16 to $243.6 million in FY20. Total income of the company during FY20 increased by 2.6% to $243.6 million on the previous period. The company’s all asset classes delivered positive rental income growth, wherein, office delivered strong growth of 7.3%, mixed-use assets rose 5% and retail grew by 0.9%. Its Funds from Operations increased 6.3% to $113.6 million on pcp. At the year-end, the portfolio was 99.3% occupied with a healthy weighted average lease expiry of 5.2 years. The company posted a pre-tax operating profit of $129.7 million (excluding the impact of fair value movements), up 4.2% on pcp.

The company’s FY20 revenue was largely unaffected by COVID-19, which caused the widespread economic uncertainty that prompted asset valuers to soften their assumptions, resulting in a $290 million, or 8.5%, write-down in the fair value of the company’s property portfolio. The revaluation of Kiwi Property’s investment assets caused a drag on the company’s reported full year financial performance, turning an otherwise healthy operating result into a net loss after tax of $186.7 million.

Historical Financial Performance (Source: Company Reports)

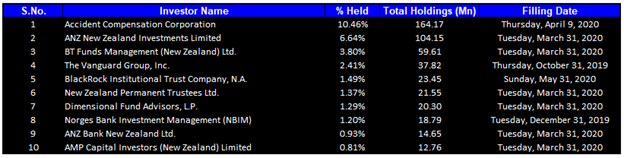

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 30.42% of the total shareholding. Accident Compensation Corporation and ANZ New Zealand Investments Limited are holding maximum interests in the company at 10.46% and 6.64%, respectively.

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

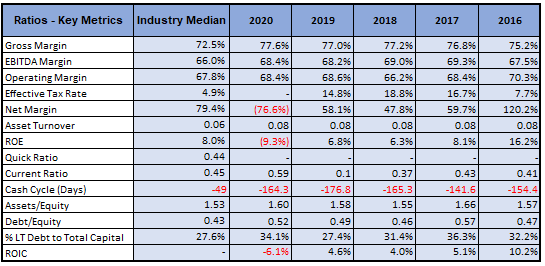

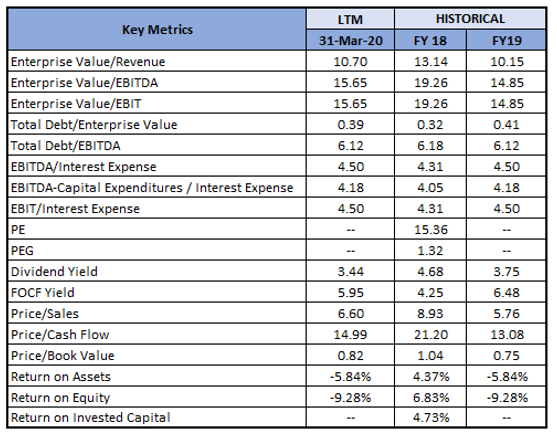

A Quick Look at Key Metrics: Its gross margin and EBITDA margin for FY20 stood at 77.6% and 68.4%, better than the industry median of 72.5% and 66.0%, respectively, implying decent operating efficiency of the company than the peer group. Its cash cycle for FY20 stood at negative of 164.3 days, lower than the industry median of negative of 49 days, implying that the company managed its asset-liability balances in an efficient manner, than its peer group.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Negative Impact of COVID-19 on Investment Portfolio: Recently, the company reported a decrease of ~$290 million (-8.5%) in the fair value of its property portfolio. The significant uncertainty caused by pandemic has prompted valuers to include an assessment of its effects on property values. Resultantly, their assumptions around rental growth, vacancy, downtime, leasing up allowances as well as trading conditions have softened.

Following the independent revaluation for each segment, its mixed-use, office, retail and other property assets were worth $3.1 billion as on 31 March 2020, heavily impacted by the COVID-19 pandemic. Following the valuation result, KPG’s investment portfolio capitalization rate has softened by 12 basis points (bps) from 5.99% to 6.11%, and its net tangible asset backing per share decreased by 18 cents from $1.42 to $1.24 per share. However, its gearing has increased to 32%, which remains within the target range.

While the company delivered a decent operating performance for FY20, the onset of the COVID-19 pandemic late in the financial year had a significant impact on its property valuations and net profit. It has implemented several measures to help its business navigate the pandemic and emerge strongly from the crisis.

Developmental Projects in KPG’s Pipeline: The company made strategic acquisitions of the properties adjacent to the Sylvia Park, giving Kiwi Property access to both sides of the railway line and creating significant scope for future mixed-use development. Moreover, construction of the galleria and south carpark were on track with expected opening around August 2020. There were commitments from the retailers for two-thirds of available space at the 60-store galleria, with strong demand for the remaining area from a variety of top local and international brands.

A Look at Key Updates: The annual meeting of Kiwi Property shareholders is expected to be held on 29th June 2020. The Board of Directors has decided not to pay a final dividend for the year ended March 2020, given the uncertainty caused by the pandemic, necessitating protection of the company’s balance sheet.

The company has taken the opportunity to revise the dividend policy in order to ensure that future payments are covered by underlying cash flows. As per the revised dividend policy, the company would be targeting dividend payments which are around 90-100% of the company’s Adjusted Funds from Operations. The company’s aim is to resume paying a dividend, as appropriate, after financial impact of coronavirus is clear.

What to Expect: As per the release, the company will be working alongside its tenants through the downturn, pursuing targeted development opportunities and strictly controlling costs. Diversified property portfolio, commitment to cost discipline and banking headroom, are expected to help the company to navigate through the financial impacts of COVID-19 and capitalise on the opportunities that follow.

Key Risks: The company is susceptible to variety of financial risks such as interest rate risk, credit risk, and liquidity risk. It uses interest rate derivatives to mitigate these risks (also referred as interest rate swaps). Credit based risks, such as trade receivables, are managed with a credit policy that includes performing credit evaluations on tenants and imposing standard payment terms and the monitoring of aged debtors. Liquidity risks are dealt by generating sufficient cash flows from its operating activities to meet its obligations arising from its financial liabilities and has bank facilities available to cover potential shortfalls.

Real Estate Sector Outlook: Commercial property market is expected to gain pace as the country has been successful in defeating coronavirus. Moreover, the rise in co-working, serviced office space and other variations, with the focus on the small and medium enterprises and start-up sectors, are changing the dynamics of commercial market. Real estate sector is one of the significant sectors in creating jobs and homes. The interest rates have been set at lower levels and this might be a key demand driver for the broader real estate sector.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

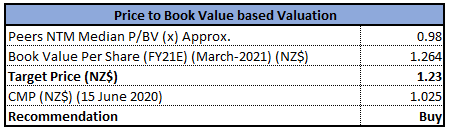

Valuation Methodology: Price to Book Value (P/BV) Multiple Based Relative Valuation (Illustrative)

Price to Book Value (P/BV) Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with upper band suggesting overbought status while lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

In the previous week, the stock rebounded beyond 50% retracement level of $1.168 and made a high of $1.200. But it could not hold on positive momentum and slipped below 38.2% retracement level of $1.066 and finally gave close at $1.0250. On this date of June 15, 2020, the stock gave opening at marginally high level of $1.050 and made the high of $1.070 but gave closing at the previous week closing level of $1.025 thereby forming Bullish Harami chart pattern suggesting that bearish trend is near end. Momentum indicator RSI with around 59 reading also suggests strength in bullish momentum.

Going forward, the stock may have resistance around 61.8% retracement level of $1.269 while support could be around $0.940.

Stock Recommendation: The company manages diversified and high-quality portfolio, which enables it to offer its valuable investors with a trustworthy investment in New Zealand property through the ownership and active management. The country has managed the spread of coronavirus well, giving the nation ‘Coronavirus Free’ tag. This would not only help the NZ government to put in place strategic economic recovery measures but would also attract foreign investments. Following the NZ government decision to lower alert level to 1, the number of visitors to shopping centres are likely to significantly increase, which will give big boost to the company’s property portfolio.

KPG is expected to benefit from successful extension of its bank debt facilities on three- and five-years term. Moreover, to strengthen its balance sheet, the company has initiated work on several measures to reduce expenses, which may offset any decline in income resulting from pandemic.

Considering the aforesaid facts, recent updates and FY20 results, we have valued the stock using Price to Book Value (P/BV) multiple based relative valuation method (on an illustrative basis) and we have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$1.025 per share on June 15, 2020.

.png)

KPG Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...