Company Overview: Kiwi Property Group Limited (NZX: KPG) happens to be the largest listed property company on New Zealand Stock Exchange under the symbol “KPG”. The company’s objective revolves around providing investors with the reliable investment in NZ property by targeting superior risk-adjusted returns over time through ownership as well as active management of the diversified, high-quality portfolio. The company has never wavered from its strategy and it continues to focus only towards New Zealand property sector. Notably, Kiwi Property Group Limited is an active asset manager.

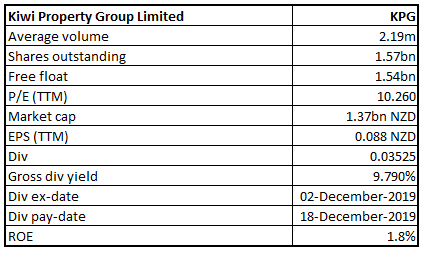

KPG Details

Investment Summary:

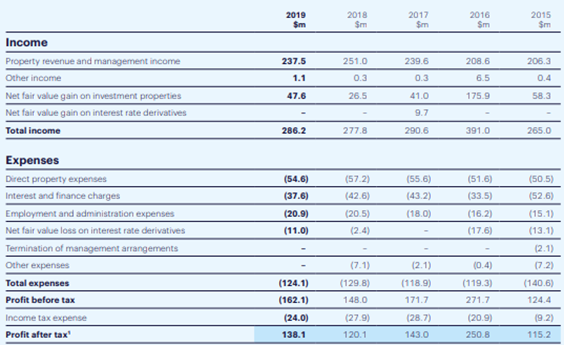

Portfolio Addition Expected to Cover Rental Income Shortfall: Kiwi Property Group Limited (NZX: KPG) is one of the leading property companies in New Zealand, with over 25 years of experience. It is managing ~$3.3 billion portfolio of real estate, comprising some of New Zealand’s best mixed-use, retail and office buildings. The market capitalisation of the company stood at ~$1.37 billion on 18th May 2020. Looking at the past performance over FY15 to FY19, total revenue and net income of the company have grown at a CAGR (compounded annual growth rate) of ~3.6% and ~4.6%, respectively. The company’s total revenue improved from $206.3 million in FY15 to $237.5 million in FY19, and net income improved from $115.2 million in FY15 to $138.1 million in FY19.

The company’s objective is to provide investors with a reliable investment platform to invest in New Zealand property through the ownership and active management of a diversified, high-quality portfolio. S&P Global Ratings has assigned Kiwi Property an issuer credit rating of BBB (stable) and an issuer credit rating of BBB+ for each of its fixed rate senior secured bonds.

The annual meeting of Kiwi Property shareholders is expected to be held on 29th June 2020. The company made strategic acquisitions to the properties adjacent to the Sylvia Park train station, giving Kiwi Property access to both sides of the railway line and creating significant scope for future mixed-use development. Moreover, construction of the galleria and south carpark were on track which are expected open around August 2020. There were commitments from the retailers for two-thirds of available space at the 60-store galleria, with strong demand for the remaining area from a variety of top local and international brands.

Moving forward, the company’s decent financial position, comprehensive cost savings programme, high occupancy of 99.4% and the stable rating S&P Global Ratings are expected to help the company in attracting the attention of market players.

Historical Financial Performance (Source: Company Reports)

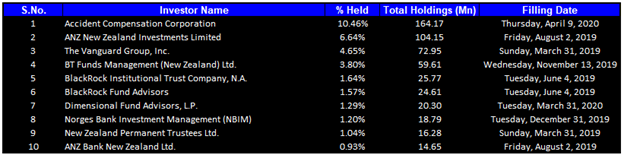

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 33.22% of the total shareholding. Accident Compensation Corporation and ANZ New Zealand Investments Limited hold maximum interests in the company at 10.46% and 6.64%, respectively.

Top 10 Shareholders (Source: Refinitiv (Thomson Reuters))

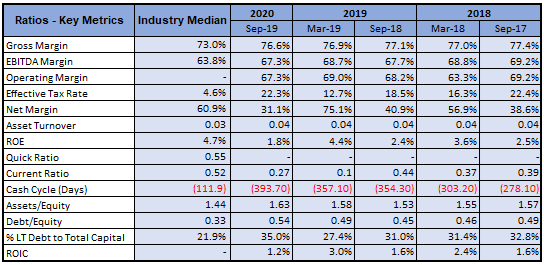

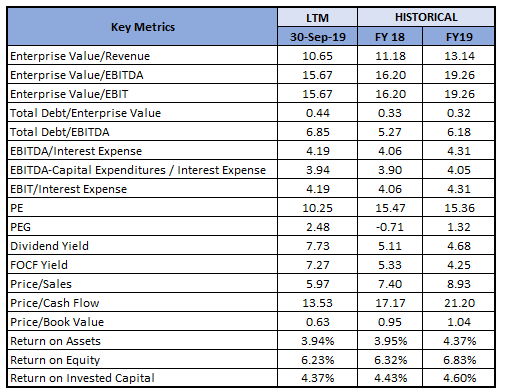

A Quick Look at Key Metrics: Its gross margin and EBITDA margin for H1FY20 stood at 76.6% and 67.3%, better than the industry median of 73.0% and 63.8%, respectively, implying decent operating efficiency of the company than the peer group. Its cash cycle for H1FY20 stood at negative of 393.70 days, lower than the industry median of negative of 111.9 days, implying that the company managed its asset-liability balances in an efficient manner as compared to its peer group.

Key Metrics (Source: Refinitiv (Thomson Reuters))

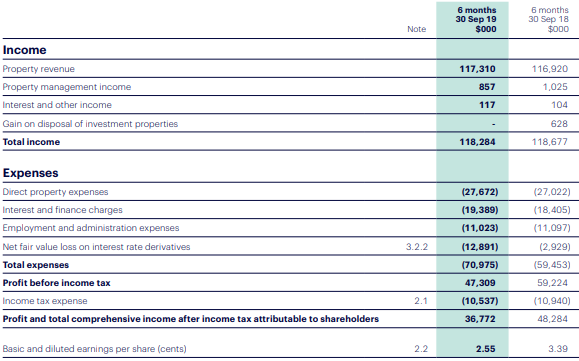

H1FY20 Highlights: Net rental income for the first half period of FY20 (ended on September 30, 2019) was reported at $89.6 million which was marginally down due to the sale of North City on pcp basis, but the net rental income grew by 2.1% on a like-for-like basis. Total rental growth for first half FY20 was reported at 4.6%, while maintaining solid momentum from previous year, mainly due to demand for space at leading mixed-use and retail location, along with premium grade office buildings.

The period witnessed good demand for space at leading mixed-use and retail locations, as well as premium-grade office buildings which is driving solid rental growth. New leases and renewals were particularly pleasing, with increase of 14.1% in mixed-use, 8.5% in office and 0.8% in retail.

Retail sales across Kiwi Property’s portfolio increased by 2.1% to $1.71 billion, with traditional shopping centre sales showing a surge of 2.3% to $1.54 billion. Specialty sales productivity improved from $11,000 per square metre in March’19 to $11,400 per square metre. Its Funds from Operations (FFO) for the period was reported at $51.9 million. Net profit after tax for the period declined by $36.8 million, due to a fair value loss of $12.9 million in the value of Kiwi Property’s interest rate swaps, following successive interest rates cuts.

The period also witnessed strategic acquisitions at 51-53 Carbine Road and 7-10 Arthur Brown Place, at a combined cost of $25.5 million. The acquisition becomes significant because these properties are adjacent to the Sylvia Park train station, giving Kiwi Property access to both sides of the railway line and creating significant scope for future mixed-use development.

H1FY20 Income Statement (Source: Company Reports)

Decline in Valuation of KPG’s Key Properties: Recently, the company reported a decrease of ~$290 million (-8.5%) in the fair value of its property portfolio. Its mixed-use, office, retail and other property assets amounted to $3.1 billion as at March 31, 2020, after their independent revaluation. KPG stated that the valuations were heavily impacted because of coronavirus pandemic.

Following the valuation result, KPG’s investment portfolio capitalisation rate has softened by 12 basis points (bps) from 5.99% to 6.11%, and its net tangible asset backing per share decreased by 18 cents from $1.42 to $1.24 per share. Its gearing has increased to 32%, which remains within the target range.

FY20 Guidance Update: As per the release, in view of the pandemic-led disruption in market, KPG has adopted a prudent approach to capital management and has decided that it would not be proceeding with the final dividend for year ended 31st March 2020.

Key Risks: The company is susceptible to variety of financial risks such as interest rate risk, credit risk, and liquidity risk. The company uses interest rate derivatives to mitigate these risks (also referred as interest rate swaps). Credit based risks, such as trade receivables, are managed with a credit policy that includes performing credit evaluations on tenants and imposing standard payment terms and the monitoring of aged debtors. Liquidity risks are dealt by generating sufficient cash flows from its operating activities to meet its obligations arising from its financial liabilities and has bank facilities available to cover potential shortfalls.

Set to Counter Risks Due to COVID-19: The company’s operating performance was in-line with expectations prior to COVID-19. However, the pandemic is expected to have material impact on KPG’s forward-looking performance as well as rental receipts. KPG has been taking several measures to counter the risks posed by coronavirus pandemic. The company extended $361 million of bank debt facilities on three and five year terms, increasing weighted average term of all debt facilities to 3.9 years. It has no bank debt maturities until 2023 financial year.

The company has also implemented comprehensive cost savings programme in order to reduce expenses and help offset any decline in income as a result of the measures to control pandemic. Non-essential capital expenditure projects are now on hold until there is greater clarity with respect to the future trading environment. The company has maintained high occupancy of 99.4% and the weighted average lease expiry of 5.1 years.

Real Estate Sector Outlook: As per the announcement by the Government official under housing ministry on May 9, 2020, building activities across the country have recommenced with all 300 work sites across New Zealand expected to be up and running again shortly. Another key message, as provided by the Government, is that real estate sector has been put forth to be one of the significant sectors in creating jobs and homes. The interest rates, which are at all-time low, are going to be there for long time and this might be a key demand driver for the broader real estate sector.

Commercial property market is expected to gain pace with the ease in restrictions along with strong government initiatives to drive the economy back on track. Moreover, the rise in coworking, serviced office space and other variations, with the focus on the small and medium enterprises and start-up sectors, are changing the dynamics of commercial market.

Key Valuation Metrics (Source: Refinitiv (Thomson Reuters))

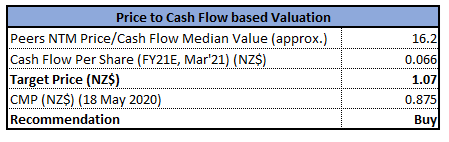

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Overview:

Weekly Chart:

(Source: Refinitiv (Thomson Reuters))

Note: Purple colour lines are Bollinger Bands, yellow lines are retracement lines and orange colour dotted line is Parabolic SAR. Technical tool Parabolic SAR uses trailing ‘Stop’ and ‘Reverse’ method to identify suitable exit and entry points. It appears as dotted line either above or below the underlying stock’s price, depending upon the direction of the stock.

The stock while remaining in ascending channel, provided by upper Bollinger Band and 20 period SMA, made the high of $1.70 and from there it steadily fell into descending channel provided by 20 period SMA and lower Bollinger Band. The falling magnitude kept on intensifying leading to enlarging of descending channel. The stock prices kept on falling till it made the low of $0.72. From the low, the stock rebounded beyond 23.6% retracement level of $0.96 and kept trading above the same. But, for last two weeks the stock had been giving close below the same. In first trading session of the on-going week, the stock gave closing at $0.87, pointing at softness in trend.

Technical indicators such as MACD with bearish cross-over and flattish curve at the end, and RSI with 20 reading and flattish curve at the end suggest flattish momentum for the stock. However, RSI reading of 20 also suggest highly oversold zone for the stock which may be the reason for prospective rebound in the stock prices.

Going forward, the stock is likely to find good resistance around 50% retracement level of $1.21 while on price retreating further, it could have support around the previous low of $0.72.

Stock Recommendation: The company offers a platform to invest in New Zealand property through the ownership and active management of a diversified, high-quality portfolio. The current pandemic situation has led to decrease in valuation of properties and related asset classes. However, with the lowering of alert level, several offices have been opened and economic activities have started gaining momentum. The rise in commercial activities will give rise in demand for corporate/government offices, shopping mall and large format retail stores and factories and warehouses. This will result into rise in rental income for the company. KPG, being one of the largest player in the industry, is well-placed to capitalize on emerging opportunities in the industry. Besides, to strengthen its balance sheet, KPG has initiated work on several measures to reduce expenses, which may offset any decline in income resulting from pandemic.

Considering the aforesaid facts and recent updates, we have valued the stock using Price to Cash Flow Multiple Based Relative Valuation (on an illustrative basis) and we have arrived at a target price of lower double-digit growth (in % terms).

Hence, we give a “Buy” recommendation on the stock at the current market price of NZ$0.875 per share, down by 3.31% on May 18, 2020.

.png)

KPG Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...