Company Overview: Kathmandu Holdings Limited is a specialist outdoor retailer. The Company is engaged in designing, marketing and retailing of clothing and equipment for travel and adventure. The Company's segments include New Zealand, Australia and the United Kingdom. It offers a range of apparels, including waterproof jackets, down jackets, thermals, fleece jackets, shirts and pants, merino apparel and thermals, and footwear and socks. It also offers equipment, including packs, bags, sleeping bags, tents, travel accessories and camping accessories. The Company operates approximately 110 stores in Australia, over 46 stores in New Zealand and approximately four in the United Kingdom. The Company's subsidiaries include Milford Group Holdings Limited, Kathmandu Limited, Kathmandu Pty Limited and Kathmandu (U.K.) Limited.

KMD Details

Another Year of Record Sales and Profit: Kathmandu Holdings Limited (NZX: KMD) is a designer, marketer, retailer, and wholesaler of clothing, footwear and equipment for travel and adventure. The company has operations in New Zealand, Australia, the USA and the UK. In FY19, the company reported another year of record sales and profit growth, with positive contribution from the Australian business and significant growth from Oboz business. A rise in sales during the key winter period, along with the cost efficiencies, helped boost earnings in Australia. Oboz brought in diversification on the product and market front, providing a significant contribution to sales and profits. Sales and EBITDA for the year went up by 9.7% and 10.9%, respectively. NPAT witnessed a rise of 13.7%. Out of the total capital expenditure during the year, a large portion was invested to further optimise the store network. The remaining amount was invested in growth enabler projects like the online platform upgrade and a new market leading warehouse management system.

Sales for the five-year period covering FY15 to FY19 witnessed a CAGR growth of 7.4%, with FY15 and FY19 sales amounting to $409.37 million and $545.62 million, respectively. Bottom-line CAGR growth for the above period stands at 29.6%, with FY15 and FY19 PAT amounting to $20.42 million and $57.63 million, respectively.

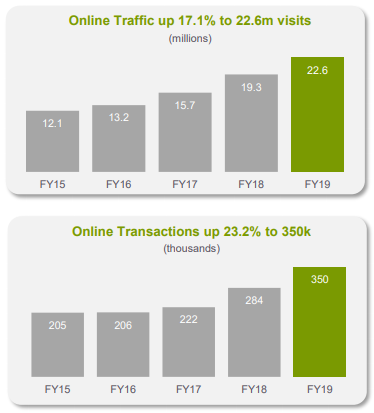

Over the five-year period starting FY15 to FY19, the company has witnessed a continuous upward movement in the online traffic. In FY19, the traffic went up by 17.1%, with 22.6 million visits by the end of the period. 5-year CAGR pertaining to online traffic stood at 16.9%, with the highest increase reported in FY18 at 22.9% (yoy). By the end of the year, the number of online transactions went up by 23.2% to 350,000, as compared to 284,000 in the previous year. This was the highest increase reported among all the years starting from FY15, depicting the increased effectiveness of the online channel in FY19.

Going forward, the company will focus on advancements of its core markets of Australia and New Zealand. It will aim at extending its market leadership in key product categories and will also work on accelerating growth in other high potential categories. Moreover, it will continue to enhance the customer experience through improvements in product information, payment options, and fulfilment solutions.

Progress in the Online Channel (Source: Company Reports)

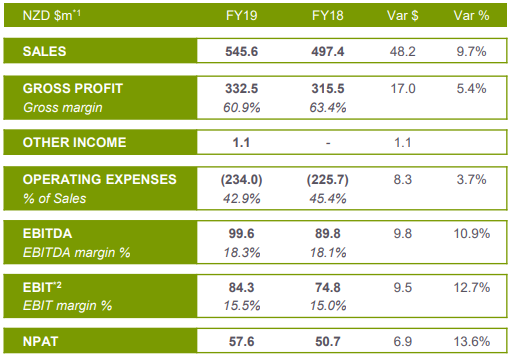

Financial Highlights: During the year ended 31 July 2019, the company reported sales amounting to $545.6 million, up 9.7% on prior corresponding year sales of $497.4 million. EBITDA for the year stood at $99.6 million, representing an increase of 10.9% on previous year EBITDA of $89.8 million. NPAT for the period amounted to $57.6 million, rising by 13.6% on FY18 NPAT of $50.7 million. Growth in sales and profit came in as a result of contribution from the Australian business, as well as the inclusion of Oboz. Oboz contributed significant value to sales, with contribution from North America coming in at $47.9 million. Excluding North America, growth in sales was reported at 2.1% at constant exchange rates. During the year, the company reported income worth $1.1 million from a tax refund for prior year GST treatment of reward vouchers.

FY19 Financial Summary (Source: Company Reports)

Business Performance: Australia segment reported a growth of 4.5% in total sales, with continued growth in key product categories. Same stores sales in the Australian market reported a growth of 2.7%. Sales in New Zealand went down by 3.1%. Growth in online sales was supported by successful re-platforming of Kathmandu’s online offering, pushing the sales upward by 9.2%. The period saw higher conversion rates of online traffic to sales on the back of rich customer experience. The company’s online channel now comprises of 10.1% of direct to consumer sales as compared to 9.4% in the previous year. FY19 saw the first full-year contribution after the integration of Oboz. The business reported FY19 pro forma sales growth of 30.0% to US$44.6 million. Pro forma EBIT growth was reported at 38.6%. Contribution from North America to Group EBIT, increased from $2.4 million in FY18 to $9.6 million in FY19.

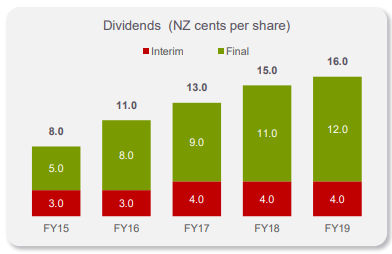

Dividend on Rise: The company declared a final dividend of NZ 12.0 cents per share as compared to NZ 11.0 cps in FY18, with a record date and payment date of 30 September 2019 and 11 October 2019, respectively. During the last 4 years, the company has delivered over $100 million in shareholder dividends, reflecting a safe and secure platform for investors.

Dividend Trend (Source: Company Reports)

As discussed in the above section, the company saw decent results with respect to the Australian and Oboz businesses. Moving forward, the company is eyeing increased foot traffic and conversion metrics in key metro markets in New Zealand, which will be supported by recent openings of Kathmandu flagship stores in key cities. The company has already done remarkably in North America after integrating Oboz and is expecting further expansion from the recently acquired Rip Curl business.

Recent Updates:

Change in Shareholding: The company recently updated that the voting power of Briscoe Group Limited increased from 16.290% to 17.707%.

Acquisition of Rip Curl and Senior Manager Changes: The company had entered into a binding agreement for the acquisition of Rip Curl, a global surf brand and action sports company. Kathmandu Holdings Limited offered a consideration of $368 million for acquiring 100% of Rip Curl Group Pty Limited. As per the information provided on the exchange, the company completed the acquisition on 31 October 2019. The above deal will help to diversify Kathmandu’s geographic footprint, with Rip Curl’s widespread global presence across Australia, New Zealand, Brazil, North America, South East Asia and Europe.

The combined group of Kathmandu, Oboz and Rip Curl will comprise 341 owned retail stores, 254 licensed stores and over 7,300 wholesale doorways, forming a global outdoor and action sports company with revenue of over $1.0 billion. One of Kathmandu’s strategic priorities has been to establish itself in North America and Europe, which can now be accelerated. The transaction is expected to deliver decent EPS accretion for the company’s shareholders.

Following the acquisition of Rip Curl, the company updated that Reuben Casey, currently serving as the COO, has been appointed as the CEO of the Kathmandu business. In addition, Michael Daly will continue serving as the Chief Executive Officer of the Rip Curl business.

Rip Curl’s acquisition was fully funded through a combination of debt and equity, including $231 million from new senior secured debt facilities, $32 million through placement of new Kathmandu shares to the founders and CEO of Rip Curl, subject to escrow for 12 months after the issue, and an underwritten 1 for 4 pro-rate accelerated entitlement offer to raise $145 million. Details of the entitlement offer are provided in the section below.

Entitlement Offer: Out of the total amount of $145 million, the company raised $113 million through an Institutional Bookbuild. The clearing price under the Institutional Bookbuild was $3.06 per share, comprising a premium of $0.51 on the application price of $2.55 per share. The remaining amount of $32 million was raised via the Retail Bookbuild component, with a clearing price of $3.08 per share, representing a premium of $0.53 on the application price of $2.55 per share.

Subscribed Entitlement Under the Offer (Source: Company Reports)

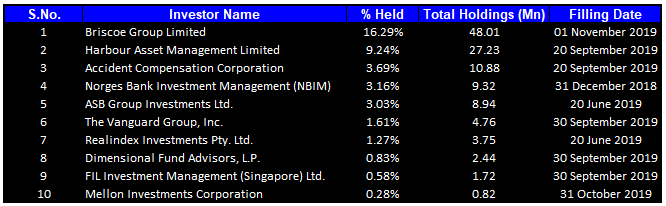

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 40.00% of the total shareholding. Briscoe Group Limited is the entity, holding maximum shares in the company at 16.29%. Harbour Asset Management Limited is the second largest shareholder, with a percentage holding of 9.24%.

Top Ten Shareholders (Source: Thomson Reuters)

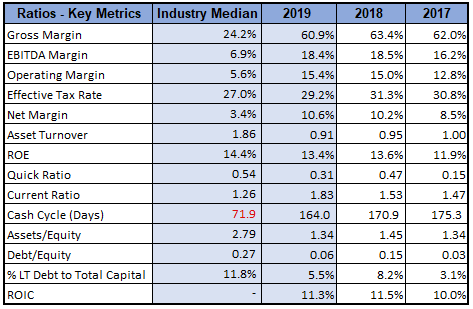

Key Metrics: During the year ended 31 July 2019, the company’s gross margin and EBITDA margin stood at 60.9% and 18.4%, respectively, higher than the industry median of 24.2% and 6.9%, implying decent fundamentals of the company. Net margin for the year stood at 10.6%, higher than the industry median of 3.4%. Current ratio for the period was reported at 1.83x, better than the previous year’s ratio of 1.53x. The ratio also exceeded the industry median of 1.26x, depicting better liquidity in comparison to its peers.

Key Metrics (Source: Thomson Reuters)

Outlook: Going forward, the company’s growth initiatives will be based on four strategic imperatives, including growth in core markets of Australia and New Zealand through diversification, optimisation of store network, elevating the performance of key metro markets, etc. Secondly, the company is eyeing to expand the market for key product categories, while simultaneously focusing on growth in other high potential categories. Third in the list will be enhancing the customer experience through advancement in product and payment options. The last strategic priority will be to enhance the global footprints and explore other international market opportunities in addition to North America.

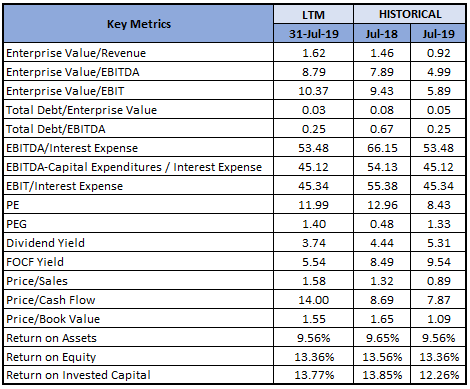

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

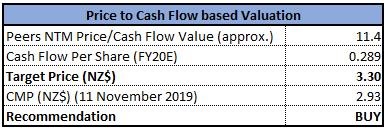

Method 1: Price to Cash Flow Multiple Approach:

Price/Cash Flow Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

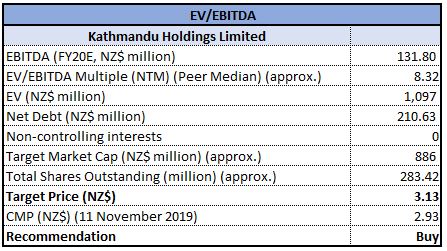

Method 2: Enterprise Value to EBITDA Multiple Approach:

EV/EBITDA Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Stock Recommendation: FY19 was marked by decent growth across all key financial metrics. The company reported an improvement in the balance sheet position, with strong cash flows supporting a $14 million repayment of net debt and $15.7 million capital investment. Operating expenses as a percentage of sales, went down by 2.5%, reflecting the benefits of channel diversification into wholesale. The period was marked by a decent operating cash flow of $61.7 million. In terms of dividend, the company reported a record high full-year payout of NZ 16.0 cents per share. FY19 was a period of significant full-year contribution from Oboz. Moreover, the company’s recent acquisition of Rip Curl is expected to provide further synergistic benefits in terms of geographical expansion, product and brand diversification, and accelerated growth in the online channel. Considering the above scenario, we have valued the stock, using two relative valuation methods, i.e., Price to Cashflow multiple and Enterprise Value to EBITDA multiple, and arrived at a target price of high single-digit to low double-digit (in % term). Hence, we recommend a “Buy” rating on the stock at the current market price of NZ$2.930, down 2.98% on 11 November 2019.

KMD Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...