Company Overview: Kathmandu Holdings Limited (NZX: KMD) is a specialist outdoor retailer engaged in the designing, marketing and retailing of clothing and equipment for travel and adventure. The company operates in New Zealand, Australia, and the United Kingdom. It offers a range of apparel, including waterproof jackets, down jackets, thermals, fleece jackets, shirts and pants, merino apparel and thermals, and footwear and socks. It also offers equipment, including packs, bags, sleeping bags, tents, travel accessories and camping accessories.

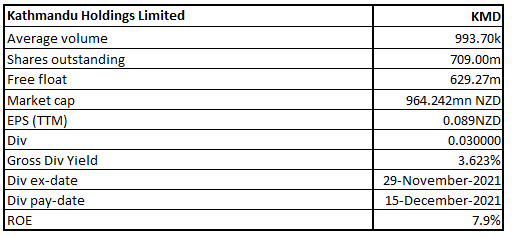

KMD Details

Kathmandu Holdings Limited (NZX: KMD) is a global retailer of outdoor, lifestyle, and sports. It owns three iconic brands: Kathmandu, Rip Curl and Oboz. The market capitalisation of the company stood at ~$964.242 million on 21st February 2022.

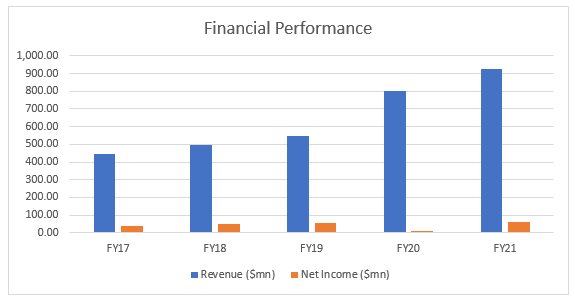

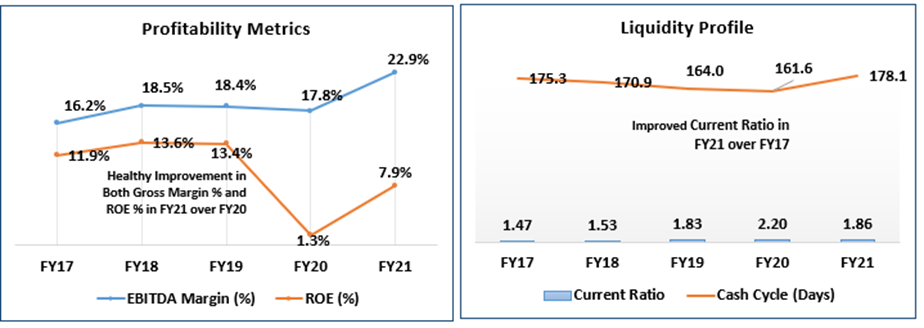

Looking at the past performance over FY17 to FY21, KMD’s top line grew with a compounded annual growth rate (CAGR) of 19.98%. Total Revenue of the company improved from $445.3 million in FY17 to $922.8 million in FY21. Net Income increased to $63.1 million in FY21, up from $38 million in FY17.

Exhibit 1: Financial Statistics

Source: Analysis by Kalkine Group

Result Performance (FY21 Ended 31 July 2021)

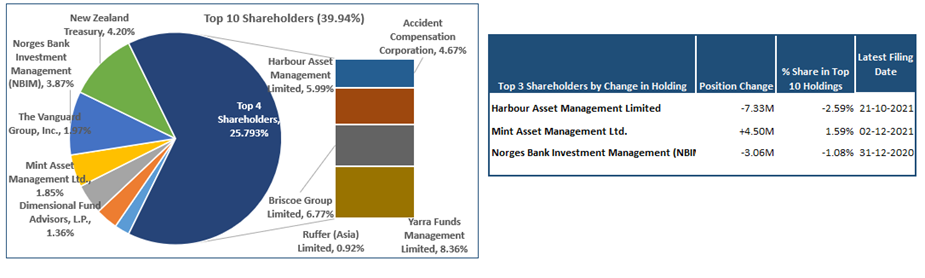

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 39.94% of the total shareholding. Yarra Funds Management Limited and Briscoe Group Limited are holding a maximum stake in the company at 8.3607% and 6.7711%, respectively, as provided in the table below:

Exhibit 2: Top 10 Shareholders

Source: Analysis by Kalkine Group

A Quick Look at Key Metrics:

The company has posted a gross margin of 58.7% in FY 2021 as compared to the industry median of 24.5%. It has posted a net margin of 6.9% as compared to the industry median of 5.7%. Therefore, it could be said that KMD is possessing decent capabilities to convert its top line into bottom line as compared to the broader industry.

Exhibit 3: Key Metrics

Analysis by Kalkine Group

Recent Updates:

On 11 February 2022, the company released an update on its trading performance for H1FY22. Same-store sales grew significantly for the Q2FY22, as Rip Curl wholesale sales witnessed the growth and retail sales met expectations while cycling strong growth in the prior year. Supply chain disruptions continue to heavily impact Oboz.

Outlook:

Kathmandu was pleased to see a strong rebound in sales over Q2FY22. The company is well placed in terms of its inventory and new product introductions for the upcoming half year. Group wholesale sales for H1 FY 2022 are expected to be 3.4% above last year, with Rip Curl wholesales sales +18.2%, offsetting declines in Oboz. The company forecasts an underlying EBITDA in the range of $9 Mn-$11 Mn.

The company has been deploying towards the long-term value of its brands, with an additional $14 Mn expenditure in 1H FY 2022 in order to help brand marketing as well as expansion into the international markets. Notably, net debt is anticipated to be ~$48 Mn with liquidity of ~$252 Mn.

Even though supply challenges are there, forward wholesale demand for the company’s products are at record levels. Additionally, the company is well capitalised, deploying towards the long-term international expansion of the global house of brands.

Risks:

The company is exposed to credit, market, and liquidity risk that arises in the normal course of the business. KMD operates in a highly competitive industry. Since it is operating in international markets, the company is prone to foreign exchange risk.

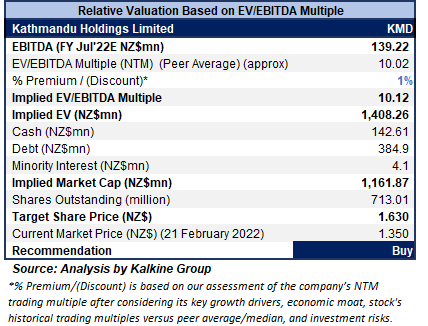

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (illustrative)

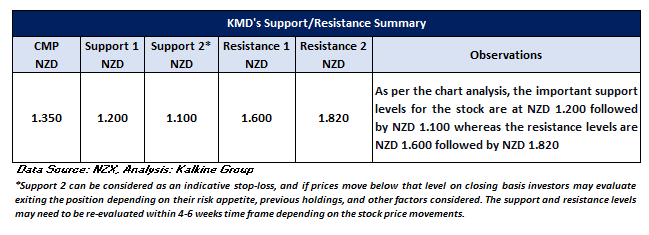

Technical Overview:

Chart:

Source: REFINITIV

Note: Purple Color Line Reflects RSI (14-Period)

Stock Recommendation:

The stock has been valued using EV/EBITDA based relative valuation (on an illustrative basis), and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to EV/EBITDA Multiple (NTM) (Peer Average), considering the decent outlook as well as higher ROE.

The company stated that H2 gross margins are expected to be in line with last year considering the current promotional plans as well as expectations of the international freight costs and currency impacts. The company is anticipating a gradual recovery from the transitory supply constraints in H2. Notably, demand for the Oboz brand as well as products has never been stronger. Also, forward orders into FY 2023 are supporting the medium-term revenue growth targets.

Considering the aforementioned facts and its current trading levels, we give a “Buy” recommendation on the stock at the current market price of NZ$1.35 per share (New Zealand Time: 5:14 PM (GMT +12)) on 21st February 2022.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...