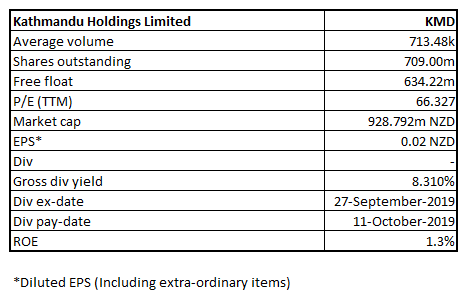

Company Overview: Kathmandu Holdings Limited (NZX: KMD) is a retailer of clothing and equipment for travel and adventure. The group is organized into four operating segments, depicting the four geographical regions in which the group operates. The company operates ~110 stores in Australia, over 46 stores in New Zealand and about 4 in the United Kingdom.

KMD Details

Apparel Industry Gearing-up for the New Normal: Kathmandu Holdings Limited (NZX: KMD) is a marketer, designer, wholesaler, and retailer of footwear, clothing, and equipment for travel and adventure. The company operates in New Zealand, the United Kingdom, the United States of America, and Australia. The company has a market capitalization of ~$928.792 million as on 19th October 2020.

Results Performance (Full Year Ending July 31, 2020)

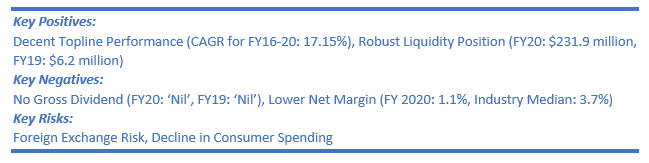

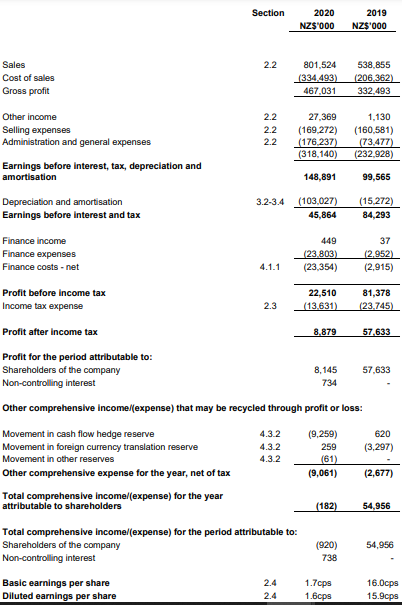

Group’s revenue from continuing operations for the full-year period stood at $801.5 million, an increase of 48.7% on the previous year. Underlying EBITDA of the Group for the period stood at $83.4 million, down 15.3% on the previous year. Underlying Net profit/(loss) for the period came at $31.5 million, down 44.5% on the previous year. Net tangible assets per Quoted Equity Security for the period stood at $0.14, as compared to $0.25 in the prior comparable period.

The results reflect on the significant impact of the COVID-19-led lockdowns on the performance of wholesale sales of the company. The Board of Directors announced no final dividend for the period.

Figure 1: Income Statement

Source: Company Reports

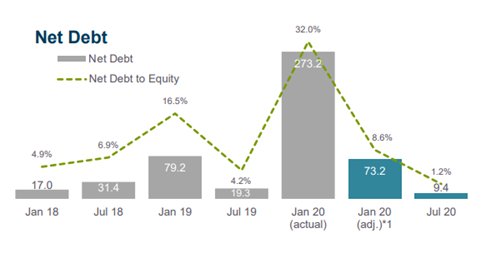

Reduction in Net Debt: The company has stated that net debt has been reduced with the help of capital raise as well as robust cash flows. At year-end, the company reported a net debt amounting to $9.4 million. The management of the company has stated that there has been decline in net debt and an improvement in leverage ratio mainly because of the fact that there was reduction in structure cost and capital raise of $207 million. Although there has been a temporary suspension of dividends during FY20, the management guided for the potential reinstatement of dividends in FY21, dependent on trading and covenant positioning.

Figure 2: Fall in Net Debt

Source: Company Reports

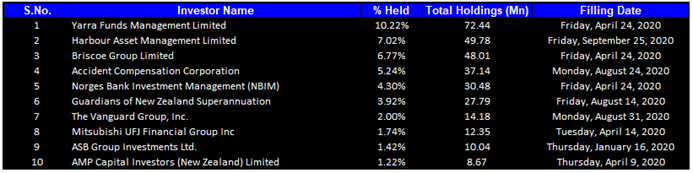

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 43.85% of the total shareholding. Yarra Funds Management Limited and Harbour Asset Management Limited are holding a maximum stake in the company at 10.22% and 7.02%, respectively, as provided in the table below:

Figure 3: Top 10 Shareholders

Source: Refinitiv (Thomson Reuters)

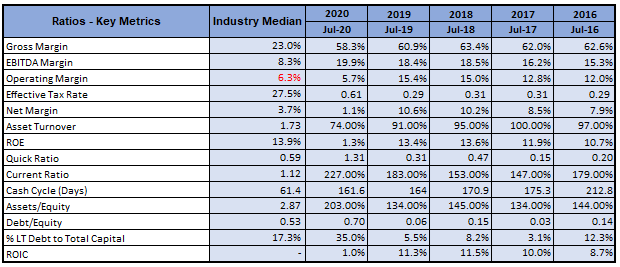

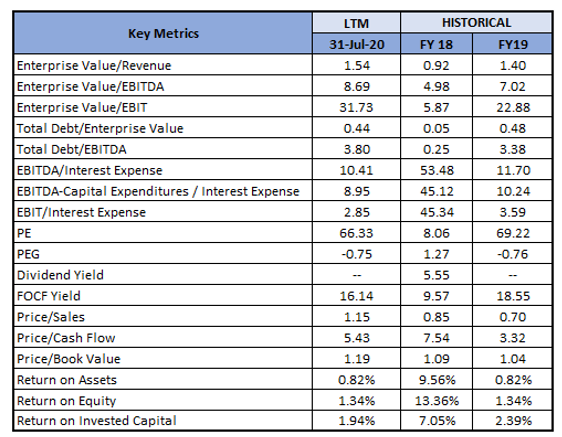

A Quick Look at Key Metrics: The company’s gross margin and EBITDA margin for FY20 stood at ~58.3% and ~19.9%, better than the industry median of ~23.0% and ~8.3%, respectively, implying the company’s ability to rationalize expenditures. Current ratio for FY20 stood at ~2.27x, better than the industry median of ~1.12x, implying that the company possesses better capabilities to meet its short-term obligations than its peer group.

Figure 4: Key Metrics

Source: Refinitiv (Thomson Reuters)

Outlook:

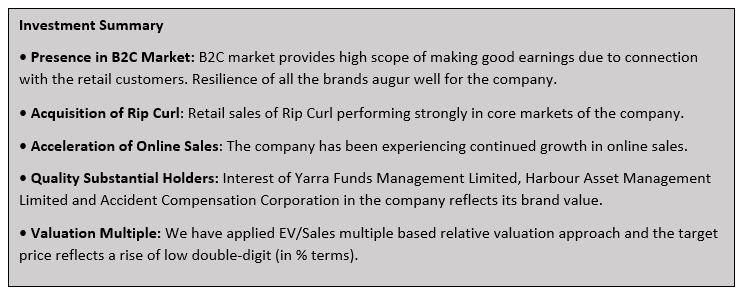

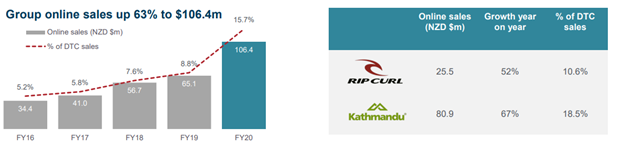

The Group has witnessed a strong recovery in retail sales for Rip Curl and Kathmandu in core markets of Australia, Europe, and California following the easing of lockdown restrictions. DTC same-store sales registered a stronger sales growth of 14.4% than pre-lockdown sales growth of 2.6%. Overall, online sales for FY20 were up 52% and now it comprises 10.6% of DTC sales.

Given post-lockdown sales performance, demand is expected to return to new normal soon benefitting FY21 overall sales. The company is well-placed to capitalize on opportunities that are likely to arise with increased participation in outdoor, beach, and surfing activities, amid easing of restrictions. The company’s omnichannel capabilities facilitate it to quickly respond to shifts in consumer behavior and rise in online demand. The long-term policy of the company related to product innovation, brand differentiation, and digital transformation will remain a key priority. The acquisition made is also in sync with the strategic objective of increasing online sales.

Figure 5: Group Online Sales

Source: Company Reports

Figure 6: Key Valuation Metrics

(Source: Refinitiv (Thomson Reuters)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

.png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv (Thomson Reuters))

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months.

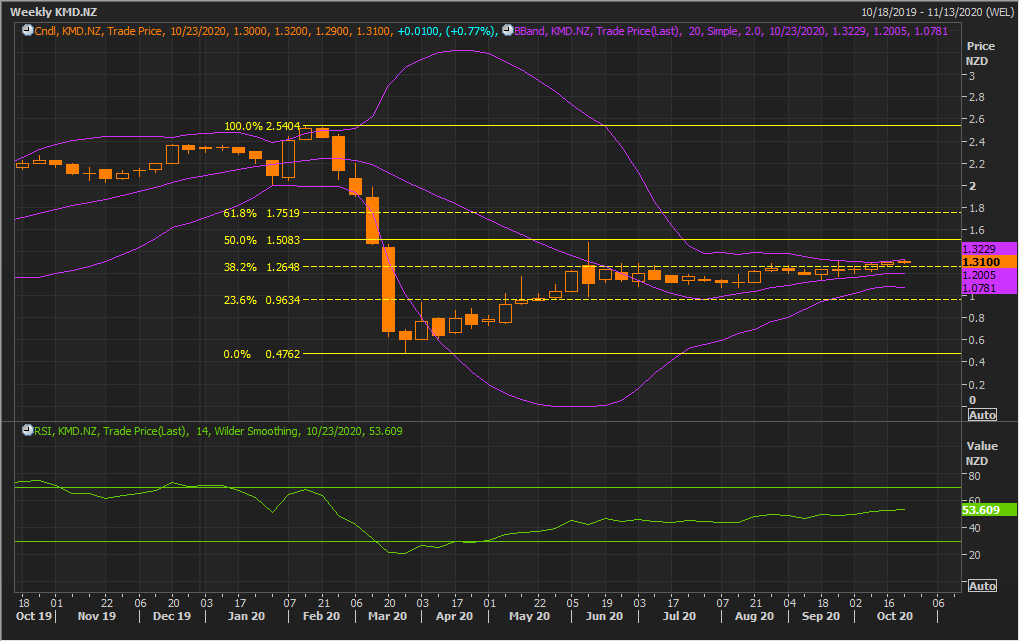

Technical Overview:

Weekly Chart –

Source: Refinitiv (Thomson Reuters)

Note: Purple colour lines are Bollinger Bands with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack.

Amidst low volatility, the stock on the first trading session of the ongoing week has given slightly close at $1.31 with a gain of 0.77% over the previous week’s closing price. The technical indicator RSI with around 54 reading and a curve at the end pointing up, suggests strong bullish momentum for the stock.

Going forward, the stock may have resistance around the 50% retracement level of $1.50 whereas support could be around 20 periods SMA of $1.20.

Stock Recommendation:

KMD seems to be well-positioned to deliver on the next level of growth opportunities. It has an un-diverted focus on growing the core markets of Australia and New Zealand. It is enhancing the customer experience through technology by providing product information, payment options, and fulfillment solution. Kathmandu and Oboz are two well-established and distinctive brands. It is building strategic partnerships, leveraging Oboz relationships to establish the Kathmandu brand. The company seems to be well-capitalized to navigate through the current trading uncertainties caused by COVID-19.

The digital infrastructure and supply chain investments have underpinned the company’s ability to rapidly ramp up online trading capabilities and distribution capacity in the face of unprecedented online demand. We have applied EV/Sales based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). For the purposes of valuation, we have taken peers such as Baby Bunting Group Ltd (ASX: BBN), Warehouse Group Ltd (NZX: WHS), Briscoe Group Ltd (NZX: BGP), Adairs Ltd (ASX: ADH), and Cash Converters International Ltd (ASX: CCV).

Considering the aforesaid facts, and future development plans, we give a “Buy” recommendation on the stock at the current market price of NZ$1.31 per share, up by 0.77% on 19th October 2020.

.png)

KMD Daily Technical Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...