I. Sector Landscape and Outlook

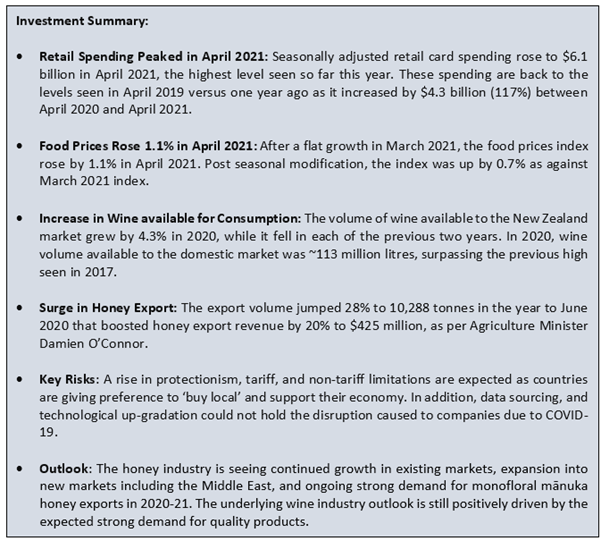

New Zealand is one of the developed countries with a temperate climate in the Asia-Pacific region. In addition, it has a stable democracy with strong economic freedom and low corruption. The fruitfulness of New Zealand in temperate food is developed around a natural environment conducive to cultivation. The favourable climate will also moderate the effects of global warming in future period. Further, the country is one of the leaders in food safety and product traceability. The consumers around the globe trust food and beverages produced and processed in New Zealand.

Exhibit 1: Rich Resources available to New Zealand to Produce more Food

Data Source: mbie.govt.nz, Chart Created by Kalkine Group

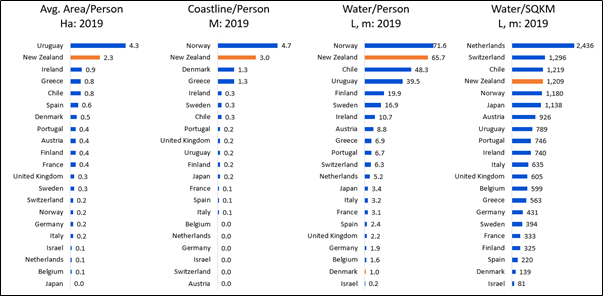

After a Flat Growth in March 2021, Food Prices Increased 1.1% in April 2021

As per Stats NZ, the food prices index increased by 1.1% in April 2021. Post seasonal modification, the index was up by 0.7% as against March 2021 index.

For April 2021, fruit and vegetable prices grew by 4.8% (up 3.4% after seasonal modification), followed by grocery food prices which increased by 1.0% (up 1.0% after seasonal adjustment), meat, poultry, and fish prices rose by 0.1%, and restaurant meals and ready-to-eat food prices increased by 1.2%. However, non-alcoholic beverage prices fell by 1.0%.

Exhibit 2: Food Prices Increased 1.1% in April 2021

Data Source: stats.govt.nz, Chart Created by Kalkine Group

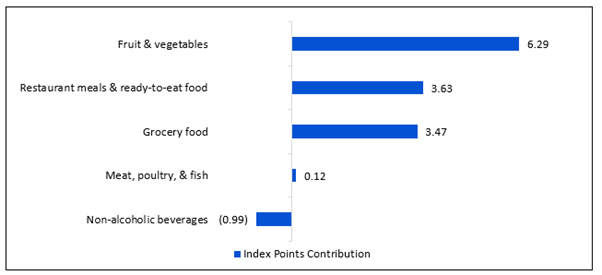

Total Volume of Wine available for Consumption Rose in 2020

The volume of wine available to the New Zealand market increased by 4.3% in 2020, while it decreased in each of the previous two years. In 2020, wine volume available to the domestic market was ~113 million litres, surpassing the previous high reported in 2017. This was led by the rise in the volume of wine made from grapes that increased by 4.9% to 94 million litres, following a decrease of 2.7% in 2019, and 2.6% in 2018. In addition, the volume of wine made from other fruit and vegetables (mostly cider) increased for the sixth year in a row, up 1.6% to nearly 19 million litres.

Further, the total volume of spirits (including spirit-based drinks) available for consumption increased by 5.2%. Spirit-based drinks, which include ready-to-drink or RTD beverages, increase 5.4%, and traditional spirits (such as whisky, gin, and vodka) increased 4.4%.

Exhibit 3: Volume of Wine, by Type, Year Ended December 2005–2020

Data Source: stats.govt.nz, Chart Created by Kalkine Group

Surge in Honey Exports Witnessed in Year to June 30, 2020

The country produces between 15,000 to 20,000 tonnes of honey every year, provided the climate is favourable for honey production. Further, the export earnings are over $340 million a year that continues to grow further. The Ministry of Primary Industries helps honey exporters sell their products to approximately 40 countries.

Meanwhile, overseas consumers who are inclined towards natural products in the face of the COVID-19 pandemic have boosted honey export revenue by 20% to $425 million in the year to June 30, 2020, as per Agriculture Minister Damien O’Connor. The export volumes jumped 28% to 10,288 tonnes in the year to June 2020. This was driven by the rise in honey volume seen from February 2020, with export volumes for the six months from January to June 2020 reaching 5,700 tonnes, up 49% from January to June 2019. Importantly, better weather conditions in most mānuka growing areas supported the average hive yields for the 2019/20 season.

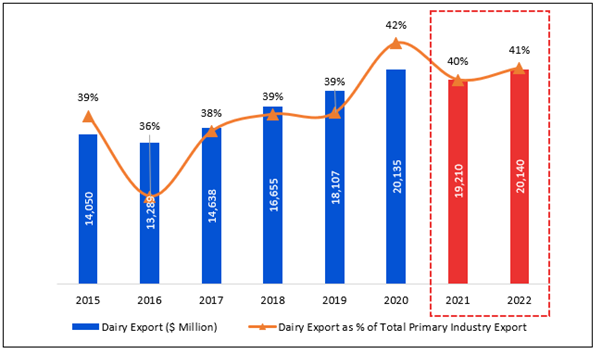

New Zealand Dairy Exports Primarily Driven by Butter, Powders, and Cheese

The primary items that are driving dairy exports in New Zealand are Powders, Butter, and Cheese as together they contributed approximately 80% to total dairy exports in 2018.

However, in January 2021, total goods exported decreased 10% from January 2020 to $4.2 billion, on the back of fall in dairy and meat. Export of dairy products fell as milk powder was down $97 million, butter was down $62 million, and whey was down $31 million from the corresponding month last year. Meanwhile, the fall in dairy exports was partly led by the fall in the volume of whey products exported to the United States. January 2021 is the fifth consecutive month this season where monthly dairy exports were below the corresponding month in the previous year. However, following a $194 million decrease in milk powder, butter, and cheese to China in December 2020, there was $89 million increase in January 2021, led by a $57 million rise in milk powder exports versus January 2020.

Exhibit 4: Prediction of Dairy Exports by Ministry of Primary Industries:

Data Source: mpi.govt.nz, Chart Created by Kalkine Group

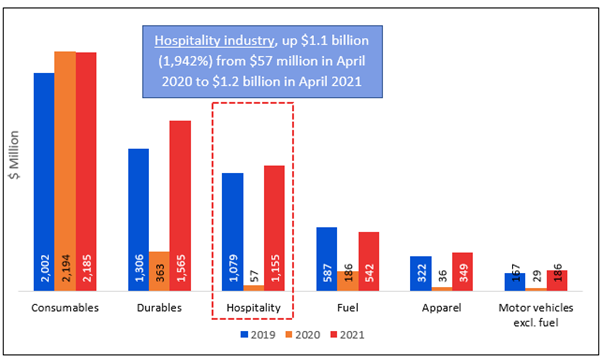

Retail Spending for 2021 Peaks in April

Seasonally adjusted retail card spending increased to $6.1 billion in April 2021, the highest level is seen so far this year. Besides, the spending increased $234 million (4%) compared with March 2021. Card spending in April 2021 is back to the levels seen in April 2019 versus one year ago as it increased by $4.3 billion (117%) between April 2020 and April 2021. This rise in spending was seen across almost all industries. Meanwhile, the hospitality industry saw the largest relative rise in spending, up $1.1 billion (1,942%) from $57 million in April 2020 to $1.2 billion in April 2021.

Exhibit 5: Actual card spending ($ million) by industry, April months, 2019 to 2021:

Data Source: stats.govt.nz, Chart Created by Kalkine Group

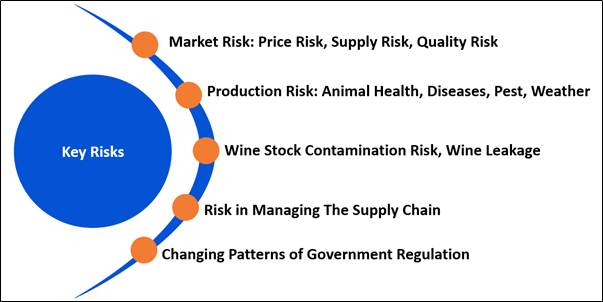

Key Risks and Challenges:

New Zealand has experienced a fall of 16.5% in total exports of goods and services, to $72.6 billion in the year ending March 2021, mainly driven by a sudden drop in both travel and transportation services, leading to the increased impact on primary industries.

In the year ended March 2021, dairy was down $512 million (3.1%) from the prior year to March 2020. Broadly, travel exports fell by 63.1% to $5.8 billion, and transportation exports fell 60.1% to $1.3 billion.

Further, the supply chain channels to consumers are shifting with an enforced switch to buy through online retail led by closure of food service businesses internationally. Although the restaurants have been reopened in COVID-19-hit areas, many consumers are cautious about exposing themselves to infection risk. This indicates more reliance on domestically produced food and switch towards greater self-sufficiency.

Moreover, climate change involves physical and transitional risks to the primary industry, which necessitates transformation across the supply chain ambit from the farm through to the end consumer.

Figure 6. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

The honey industry is witnessing continued growth in existing markets, expansion into new markets including the Middle East, and ongoing strong demand for monofloral mānuka honey exports in 2020-21. Moreover, three consecutive years of elevated production indicates that there is plenty of stock available to meet future demand.

The wine industry is optimistic regarding the year ahead with growers anticipating a slightly lower crop on the outturn. Further, the COVID-19 infection has spread significant uncertainty in growers’ forecasts. However, the underlying industry outlook is still positively driven by the expected strong demand for quality products in future period.

Further, the outlook for hard-hit hospitality sector is bleak due to uncertainties concerning the mass vaccinations, lockdowns, COVID-19 variants, localised waves and return to the stable hospitalisation rates. In addition, the trading condition will be under pressure in the short-run as the occupancy levels are at low.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) The a2 Milk Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$4.53 billion)

Business Description:

The a2 Milk Company Limited (NZX: ATM) enriches the lives of its customers by harnessing the nutritional values of nature through the naturally occurring a2 MilkTM difference. Further, the company operates in New Zealand, Australia, Greater China, North America, and few emerging markets.

Outlook:

The management has taken aggressive actions in Q4FY21, which is expected to impact the FY21 results. The company is taking suitable action to address the elevated inventory imbalances so that the current situation of inventory imbalance is under control and, more importantly, to create a platform for future growth. In addition, it continues to invest in the brand and to drive consumer demand/offtake through this rebalancing phase. The plan is to further boost the level of marketing in Q4FY21 and into FY22. Moreover, it is targeting revenue for FY21 in the range of $1.20 billion to $1.25 billion. It is targeting EBITDA to sales margin for FY21 in the range of 11% to 12% (excluding MVM transaction costs).

Valuation Methodology: Price/Earnings per Share Based Relative Valuation (Illustrative)

.png)

Stock Recommendation

We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to P/E Multiple (NTM) (Peer Average) as the trading dynamics in the China infant nutrition market are under pressure for a2MC and many international competitors. Further, the level of channel inventory is higher than previously anticipated.

For the purposes of relative valuation, we have taken peers such as Sanford Ltd (SAN.NZ), Synlait Milk Ltd (SML.NZ), Treasury Wine Estates Ltd (TWE.AX), to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $6.10 per share on 3rd June 2021.

2) Good Spirits Hospitality Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit (M-Cap: NZ$4.33 million)

Business Description:

Good Spirits Hospitality Limited (NZX: GSH) is one of the leading specialty hospitality operators in New Zealand. From establishments in Auckland’s Viaduct, the company has grown to 9 sites across Auckland and Hamilton.

Outlook

The management expects further disruption as indicated by the February 2021 lockdown. However, the company has cemented its position to capitalize on its compelling market offering along with acquisition opportunities. Further, the management aims to pursue profitable growth through both same venue growth and accretive acquisitions.

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has been trading in the range provided by the 38.2% retracement level of $0.090 on the upside and the 23.6% retracement of $0.074 on the downside. It has given a flattish close for the ongoing week at $0.075. The technical indicator RSI with a reading around 45, suggests neutral momentum for the stock.

Going forward, the stock may have resistance around $0.090 whereas support could be around the lower Bollinger band of $0.071.

Stock Recommendation:

Considering the current trading levels, expected turnaround in the future period that is currently under pressure due to COVID-19 circumstances and wide presence of business across New Zealand, we give a “Speculative Buy” rating on the stock at the current market price of $0.075, on 3rd June 2021.

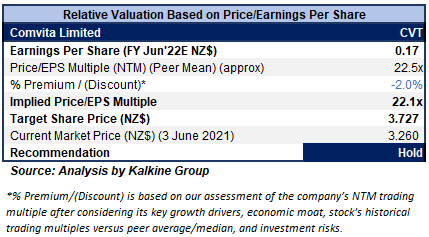

3) Comvita Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$229.2 million)

Business Description:

Founded in 1974, Comvita Ltd (NZX: CVT) is one of the leading companies in the business of Manuka honey. Further, it has developed a wide geographical presence in parts of Australia, New Zealand, China, and North America, among other places.

Outlook

As per the full-year guidance released on 13 April 2021, the company plans to achieve operating EBITDA in the range of $22.5-$25.5 million in FY21 (earlier guided range of $20 million-$23 million). The upgrade in earnings is mainly led by continuing strong growth in its focused growth markets of China and North America that offsets the challenges in ANZ and Hong Kong. Further, the benefits of strong performance in the digital channel, which currently contributes over 30% of group sales along with sustained efficiencies in production and better cost management are the reasons for the upgrade.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Stock Recommendation

We have valued the stock using P/E multiple-based illustrative relative valuation and have arrived at a target price that reflects a rise of low double-digit (in % terms). We have assigned a slight discount to P/E Multiple (NTM) (Peer Average) considering the challenges in ANZ and Hong Kong market and lower liquidity.

For the purposes of relative valuation, we have taken peers like Delegat Group Ltd (DGL.NZ), A2 Milk Company Ltd (ATM.NZ), and BWX Ltd (BWX.AX).

Considering the upgrade in forecasted earnings for FY21 and sustained focus on cost management, we give a “Hold” recommendation on the stock at the current market price of $3.26 per share, down by 0.91% on 3rd June 2021.

4) Foley Wines Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$113.1 million, Gross Dividend Yield: 2.423%)

Business Description:

Foley Wines Limited (NZX: FWL) is an integrated wine company based in New Zealand. It has a pool of iconic wineries and brands from New Zealand’s best-acclaimed wine regions.

Outlook

The harvest totalled 5,582 tonnes for 2021 vintage throughout the Marlborough, Martinborough, and Mt Difficulty wineries, down 28% on the 2020 harvest of 7,803 tonnes.

However, the fundamentals of the company are well in place. The company is working on the premiumisation strategy and it is of the view that the work done on this together with securing new channels at the higher price points would be helping in mitigating the cost effect of the higher vintage costs.

Technical Overview:

Weekly Chart –

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

While on correction path, the stock has given close at $1.72 below the 50% retracement level of $1.74. The technical indicator RSI with a reading around 42 suggests neutral momentum for the stock.

Going forward, the stock may have resistance around the 38.2% retracement level of $1.83 whereas support could be around the 61.8% retracement level of $1.65.

Stock Recommendation

Considering current trading levels, premium pricing strategy and strong balance sheet, we give a “Speculative Buy” recommendation on the stock at the current market price of $1.72 per share on 3rd June 2021.

Comparative Price Chart (Source: REFINITIV)

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined:-

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...