1. Sector Landscape and Outlook

As per the Ministry for Primary Industries, the food, and fibre sector has indicated strong momentum despite the challenging business environment due to COVID-19 circumstances. Export revenue for the year ending June 2021 is anticipated to fall 1.1% to $47.5 billion. However, for the year ending June 2022, export revenue is anticipated to rebound and reach a record $49.1 billion, driven by international demand for New Zealand’s main export market products in destination markets.

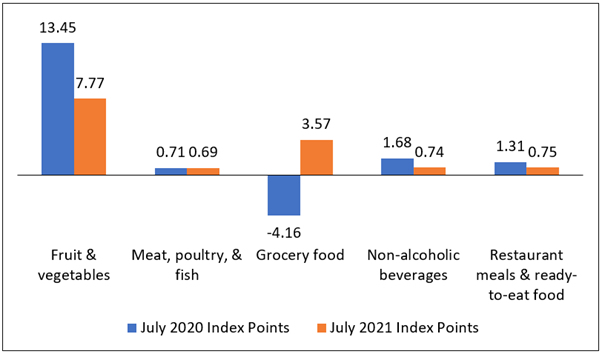

The Food Price Index Continue to Rise in July 2021

As per Stats.NZ, the food prices increased by 1.3% in July over June 2021, while after seasonal adjustment, the index was up 0.5%. This rise was contributed by the rise in fruit and vegetable prices by 5.1% (up 0.8% after seasonal adjustment), followed by meat, poultry, and fish prices that increased 0.5%. Also, grocery food prices increased 1.0% (up 0.9% after seasonal adjustment), non-alcoholic beverage prices increased 0.7%, and restaurant meals and ready-to-eat food prices increased 0.3%.

Meanwhile, the food prices grew 2.8% in the year ended July 2021 over the same month last year, where fruit and vegetable prices grew 4.9%, followed by restaurant meals and ready-to-eat food prices that grew 4.2%. Further, the grocery food prices rose 2.7%, and meat, poultry, and fish prices rose 0.4%, while the non-alcoholic beverage prices fell 0.2%.

Exhibit 1: Monthly Index Points Contribution to Food Price Index Continues to Rise

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

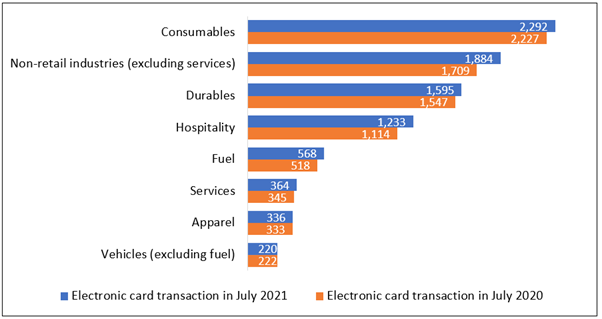

Electronic Card Transactions Continued its Rising Trend in July 2021

As per Stats.NZ, the electronic card transactions series includes all debit, credit, and charge card transactions with New Zealand-based merchants. This measure could be used to understand the changing pattern in consumer spending and economic activity. For July 2021 over June 2021 indicates that spending in the retail industries increased 0.6% ($39 million) and spending in the core retail industries increased 0.5% ($27 million).

Meanwhile, the non-retail (excluding services) category grew by $43 million (up 2.4%), which includes medical and other health care, travel and tour arrangement, postal and courier delivery, and other non-retail industries. However, the services category was down $2 million (down 0.5%), which includes repair and maintenance and personal care, funeral, and other personal services.

The total value of electronic card spending, combining the two non-retail categories (services and other non-retail) grew by $77 million (up 0.9%) compared with June 2021.

Exhibit 2: Percent Change in Card Transaction Values by Industry, June 2021–July 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysed by Kalkine Group

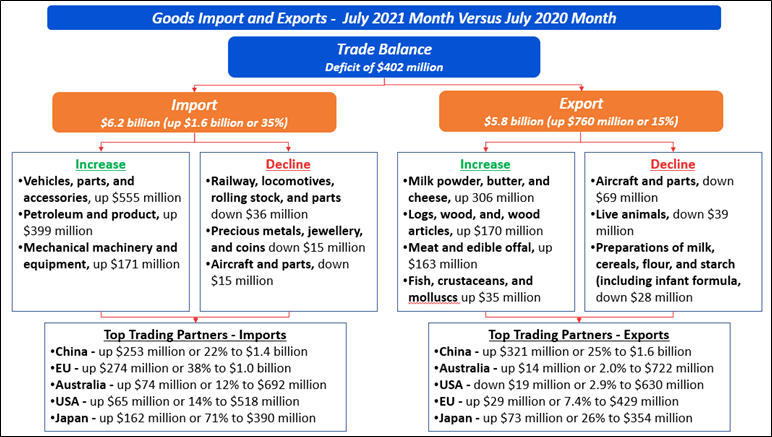

Export of Milk Powder, Butter, and Cheese Increased by 27% in July 2021

As per Stats.NZ, goods exports increased $760 million or 15% YoY to $5.8 billion in July 2021, and goods imports increased swiftly, up $1.6 billion or 35% to $6.2 billion in July 2021. This resulted in a monthly trade balance deficit of $402 million. Meanwhile, annual goods exports were valued at $61.2 billion, up $856 million (1.4%) from the previous year, while annual goods imports were valued at $62.3 billion, up $2.0 billion (3.3%) from the previous year, therefore the annual goods trade balance was a deficit of $1.1 billion. In the year ended July 2020, there was a surplus of $26 million.

Meanwhile, exports of milk powder, butter, and cheese drove the rises in total export value in July 2021, up $306 million or 27% whereas preparations of milk, cereals, flour, and starch decreased by $28 million or 15%. This indicates a promising future ahead seeing a revival in demand from international customers and supported by an improvement in supply chain management despite COVID-19 circumstances.

Exhibit 3: Overseas Merchandise Trade of July 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

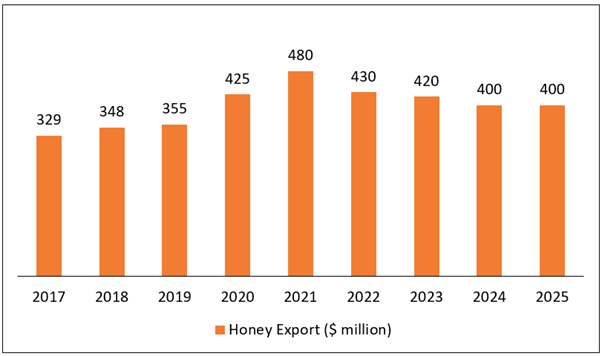

Export of Honey is Expected to be Under Pressure in Future Period

As per the Ministry for Primary Industries, honey exports are anticipated to reach $480 million for 2020-21, primarily led by a rise in export volumes, before dropping from 2021-22 onwards as international demand is expected to decrease in the future.

Exhibit 4: Trend Export Revenue of Honey 2017-2025

Data Source: mpi.govt.nz, Copyright material on the Ministry of Primary Industry website is protected by Crown copyright. It is licensed for re-use under a Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

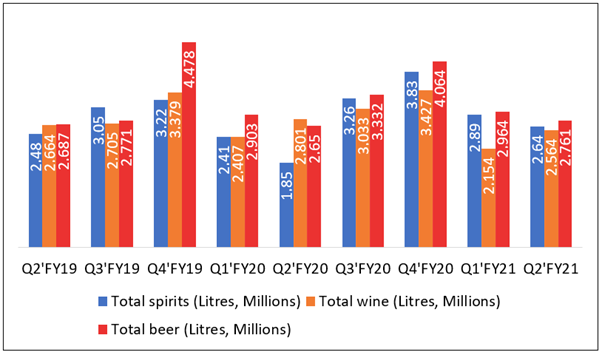

Decreasing Trend in Alcohol Available for Consumption in Q2FY21

As per Stats.nz, total sprits available for consumption fell by 8.6% QoQ to 2.641 million litres in Q2’FY21, whereas total wine available for consumption increased by 19.0% QoQ to 2.564 million litres in Q2’FY21. Meanwhile, total beer available for consumption fell by 6.8% QoQ to 2.761 million litres in Q2’FY21. This indicates the alcohol available to the consumer in New Zealand is in a decreasing trend in the recent quarters, indicating lower spending on alcohol and consumer shift towards substitutes.

Exhibit 5: Trend in Alcohol Available for Consumption – For the Quarter Ended June 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

The S&P/NZX All Consumer Staples Index generated a 5-year return of ~57.64% versus ~51.84% by the S&P/NZX All Index. Therefore, S&P/NZX All Consumer Staples Index overperformed S&P/NZX All Index by ~5.8% in 5 years.

Exhibit 6: S&P/NZX All Consumer Staples Index vs S&P/NZX All Index

Source: REFINITIV

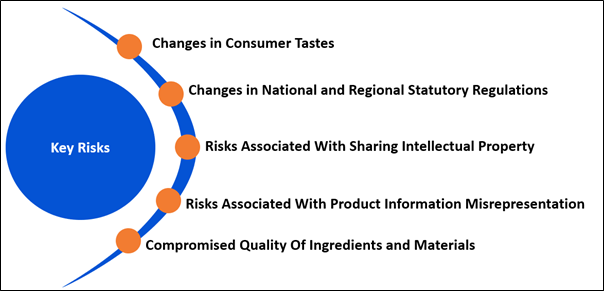

Key Risks and Challenges:

New Zealand exports its dairy products in the international market after consumption is addressed by its small population (New Zealand’s estimated resident population was provisionally 5,122,600 as of 30 June 2021). Therefore, its customer/client base is predominantly offshore and mostly, but not exclusively, includes those countries that are not self-sufficient in dairy. The focus of NZ dairy is, therefore, global by definition and the factors influencing dairy trade are global. So, it can be interpreted that the NZ dairy export must maintain and grow as per the international quality standard to sustain its export momentum, otherwise, this stream of export will be impacted and accordingly disrupt the national trade balance.

Meanwhile, key challenges faced by the honey industry include queen problems, management of the varroa mite, anticipated starvation of bees, and wasps, and other bee-robbing behaviours. Most of the losses are realized in winter due to lower nectar sources during this time of the year. Also, bees are primarily dependent on the stocks of honey they have collected in summer or supplementary feeding from beekeepers.

The alcohol industry is struggling to make its strong presence in online sales to reach broader markets, like other successful online industries. While some alcohol brands have demonstrated a successful online presence, others have found that it helps to create strategic partnerships. Further, the industry is facing intense competition than ever and must deal with frequent development in regulations and compliance.

Exhibit 7. Key Risks in Consumer Staples Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per the Ministry for Primary Industries, dairy export revenue is anticipated to fall by 5.4% to $19.0 billion for the year ending June 2021, led by the COVID-19 related circumstances, and an appreciation of the New Zealand dollar (NZD) as compared with foreign currencies. In the first half of 2021, dairy revenue was down significantly due to global supply chain and market disruptions, and subdued prices for key commodities. Meanwhile, global dairy prices increased phenomenally in the second half of 2021. Therefore, the milk production for the 2020-21 season is anticipated to rise 1.9%, supported by favourable weather conditions and a strong farmgate milk price.

Meanwhile, honey exports are anticipated to reach $480 million for the year ending June 2021, up 13% on 2019-20. Export volumes are forecasted to surpass 12,500 tonnes for the year ending June 2021, up from the 10,287 tonnes exported in 2019-20. Exports of monofloral mānuka honey reached 4,950 tonnes in the first nine months of 2021, while exports of multi floral and nonmānuka honey have reached 4,739 tonnes in the same period. However, the exports for the year to June 2022 are forecasted to drop back to around 11,500 tonnes as international demand is expected to drop back from current very high levels.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

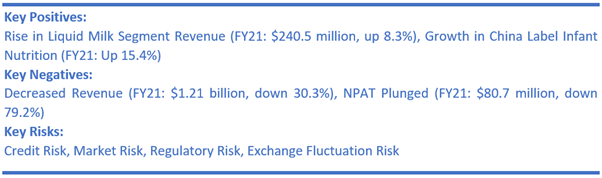

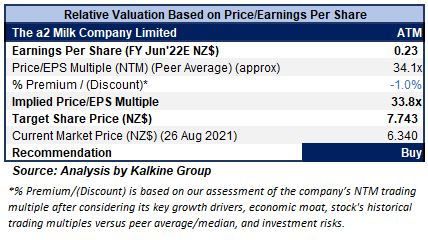

1) The a2 Milk Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$4.71 billion)

Business Description:

The a2 Milk Company Limited (NZX: ATM) improves the lives of its customers by providing the nutritional values of nature through the naturally occurring a2 Milk difference.

Outlook:

As per the annual report released on 26 August 2021, the company is confident of its fundamentals and relevant growth opportunities in core markets. Further, it is focused on product innovation, category expansion, and new markets, supported by a healthy brand and strong balance sheet, for the long-term positive outlook. However, continuing uncertainty and volatility in the consumer markets due to COVID-19 circumstances and other market dynamics, particularly in China, the company has determined not to share specific guidance on revenue or EBITDA margin at this time.

Valuation Methodology: Price/Earnings per Share Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight discount to its peers’ average, considering continuing uncertainty and volatility in the consumer markets, primarily due to COVID-19 related circumstances and other rapidly changing market dynamics, particularly in China.

For the purposes of relative valuation, we have taken peers such as Synlait Milk Ltd. (SML.NZ), Sanford Ltd. (SAN.NZ), Murray Cod Australia Ltd. (MCA.AX), to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $6.34 per share, down 11.33%, on 26th August 2021.

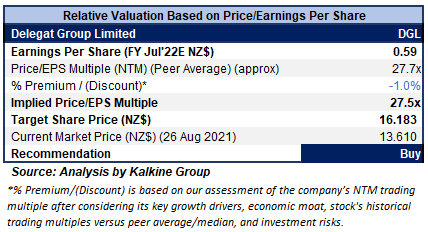

2) Delegat Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.43 billion, Gross Dividend Yield: 1.735%)

Business Description:

Based in New Zealand, Delegat Group Ltd (NZX: DGL) is the country’s leading player in the export of wine with 20 vineyards and 4 wineries under its kitty.

Outlook

As per the release dated 13th July 2021, the operating net profit after tax for FY22 is anticipated to be in the ambit of $57-$61 million. This is below this year’s unaudited result, primarily led by the impact of the lower-yielding 2021 vintage and higher grape prices resulting in an increased cost of goods per case. Also, FY22 is expected to be impacted by unfavourable exchange rate movements, higher freight costs, and higher operating expenses due to Covid-19 related circumstances.

The company plans to release its audited results for FY21 on Friday 27 August 2021.

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight discount to its peers’ average, considering lower guidance for FY22, primarily due to the impact of COVID-19 related circumstances.

For the valuation purpose, we have taken peers such as Australian Vintage Ltd. (AVG.AX), Lark Distilling Co Ltd. (LRK.AX) and Treasury Wine Estates Ltd. (TWE.AX) to name a few.

Considering the aforesaid facts, we give a “Buy” recommendation on the stock at the current market price of $13.61 per share, (New Zealand Time: 11:24 AM (GMT +12) on 26th August 2021.

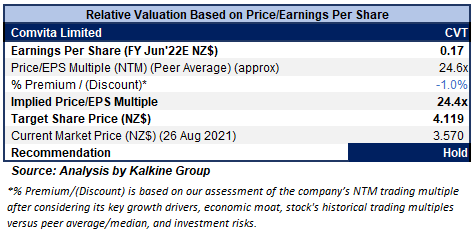

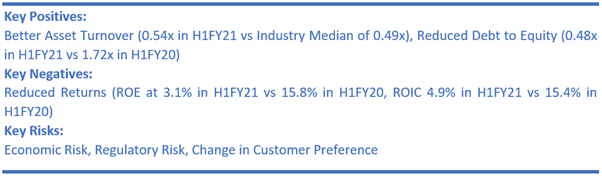

3) Comvita Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$250.97 million)

Business Description:

Comvita Limited (NZX: CVT) is one of the leading players globally in producing Manuka honey. The company has a wide geographical sales presence across Australia, New Zealand, China, and North America, among other countries.

Outlook

As per the investor presentation for FY21, released on 26 August 2021, the company anticipates FY22 EBITDA in the range of $27.0-$30.0 million, driven by an expectation of continued double-digit top & bottom-line growth in focus growth markets. Digital revenue is expected to contribute at least 38% to total revenue and mid-single-digit revenue growth is expected in the ANZ market. Meanwhile, the transformation program continues with a $2.5 million investment within guidance and aiming a further reduction in inventory from $100.0 million to $90.0 million. Capital expenditure investment of circa $18.0 million.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit (in percentage terms). The company might trade at a slight discount to its peers’ average, considering the higher inventory level, which the company is planning to reduce from $100.0 million to $90.0 million during FY22.

For the purposes of relative valuation, we have taken peers like Sanford Ltd. (SAN.NZ), The a2 Milk Company Ltd. (ATM.NZ), and Woolworths Group Ltd. (WOW.AX).

Considering the aforesaid facts, we give a “Hold” recommendation on the stock at the current market price of $3.57 per share, up 4.39%, on 26th August 2021.

4) Allied Farmers Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$17.86 million, Gross Dividend Yield: 2.874%)

Business Description:

Allied Farmers Limited (NZX: ALF) operates through its subsidiary, NZ Farmers Livestock Ltd, Farmers Meat Export Ltd, and NZ Farmers Livestock Finance Ltd whereby its activities involve the sale of livestock agencies services, the procurement, and processing of calves, and livestock financing.

Outlook

ALF noted the market update from New Zealand Rural Land Company Limited that, because of the positive adjustment to its net asset value during the process of audit, the performance fee amounting to $1.625 Mn is calculated as payable to NZRLM. This is for the period ended 30th June 2021. Notably, this would be satisfied in new NZL shares at ~$1.3968 per share. Consequently, ALF has confirmed that, subject to audit, the attributable earnings for FY 2021 is ~$1.16 Mn.

Meanwhile, the company plans to release its FY21 results on Monday, 30 August 2021.

Technical Analysis

Source: REFINITIV

Note: Purple colour lines are Bollinger Bands® with the upper band suggesting overbought status while the lower band oversold status, and yellow lines are Fibonacci retracement lines which measure price rebound and backtrack. https://www.bollingerbands.com/

The stock has been witnessing a rebound in its prices in the ongoing week with close on its peak price of $0.62 which also happens to be a converging point of 50% retracement level and the upper Bollinger band value. The technical indicator RSI with a reading around 58 and a curve at the end pointing a sharp up, suggesting no divergence in price and RSI performances and hence, the uptrend in stock to sustain.

Going forward, the stock may have resistance around the 23.6% retracement level of $0.73 whereas support could be around the 61.8% retracement level of $0.57.

Stock Recommendation

Given the sustained focus on growth strategies towards improving and growing its existing business and the capital raised in the process, the company is well-positioned to tap further growth opportunities.

Thus, we give a “Hold” recommendation on the stock at the current market price of $0.620 per share, up 6.90%, on 26th August 2021

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...