Introduction

Generally speaking, REITs have been considered to be the leading players in commercial property space in New Zealand. Globally, the industry is known for its resilience and its income-generating capability to counter medium-term and short-term blows, with some support from strong government-led initiatives, financial flexibility, liquidity, and high transparency. In particular, defensive characteristics and growing industrial sector are the backbone of the country’s real estate sector.

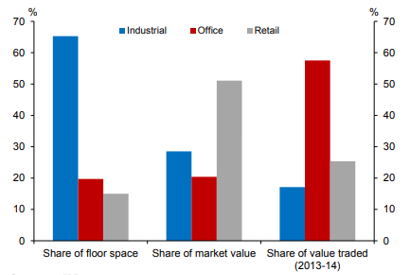

Nowadays, global investors are banking upon the country’s real estate market primarily because of decent employment levels as well as robust and sound financial system. As per the Reserve Bank of New Zealand’s Financial Stability Report (November 2014), NZ commercial property stock has been estimated to be worth around $180 billion. Generally, the commercial property is categorised into four submarkets: 1) Accommodation buildings, 2) Industrial space, 3) Office buildings, and 4) Retail.

Key Numbers (Source: Reserve Bank of New Zealand)

With this backdrop, let us look at the relative size of NZ commercial property sub-markets:

Increased Role of Real Estate in New Zealand Economy

Residential property markets are very important for the broader economic growth and for attracting investment from global players, and ‘Housing’ occupies central part of New Zealand’s economy and makes up for around half of the assets of NZ households. Below are some key points in this regard:

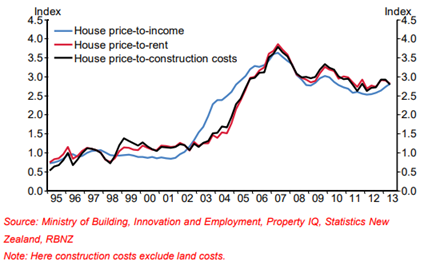

History shows us that the house prices have witnessed a strong momentum over time, while volatility keeps on charting out some changes in the trend. As per the report by RBNZ, between 2002 and 2007, house prices were doubled because demand to purchase houses surpassed new supply of houses and residential land on the market. House prices rose relative to rents, incomes and (non-land) construction costs and these prices may remain elevated relative to the fundamental factors for the extended period of time.

House Prices Relative to Fundamentals (indexed) (Source: RBNZ)

Investors’ Access to High Growth Real Estate Market

Owning a house is like an investment which could provide capital appreciation in the long-term subject to 1) Demand and supply factors, 2) Performance of broader economy, 3) Industrial growth, and 4) Interest rates. One form of making investment in real estate is through REITs (or Real Estate Investment Trusts). Key points include the following:

From investment perspective, REITs provide a sustained business model as opposed to capital appreciation model. Capital appreciation will come from rise in rentals and resettling of unit price. It will be for those who want slightly more return than bond yields without taking too much risks. However, the growth of the portfolio will depend on the growth in rentals which will, in turn, depend on the performance of the real estate sector. Affordability, Liquidity, and Stability (less exposure to broad level volatility) set out the chart for REITS, while risks around becoming out of favour or oversupplied, vulnerability to economic downturns, limited growth potential, and steep changes in interest rates are need to be considered to weigh investments in the sector.

COVID-19 and its Impact on REITs

In the wake of COVID-19, the Government realized that there is a great need to ensure that tenancies are sustained, and tenants do not have to face the prospect of homelessness. It was also critical from a public health perspective that people self-isolate in their own homes during the crisis.

Accordingly, on 23 March 2020, the Government announced a freeze to residential rent increase and greater protection to tenants against having their tenancies terminated. The rent increase freeze has been made applicable for an initial period of six months.

The Ministry of Housing and Urban Development confirms that housing and related service providers constitute towards essential services and they need to continue to operate during COVID-19. Like many other sectors, REITs have also suffered from the impact of pandemic. Industry veterans are leaving no stone unturned to minimize the impact and to cushion their financial positions. Some of the leading companies in REIT space have resorted to fund raising which could further strengthen their financial footing.

Most of the companies in REIT space are working to strengthen their balance sheet which could be used to finance the future growth opportunities. Leading banks of New Zealand are also helping the companies in REIT space to dodge the pandemic-led crisis.

Property Market in NZ is Expected to Recover with Some Boost Coming from Initiatives and Settlement of the Wave Emanating from COVID-19

As per the monthly property report released by the Real Estate Institute of New Zealand (or REINZ), median house prices for NZ (excluding Auckland) rose 13.3% to $555,000, a rise from $490,000 in March last year.

In Auckland, median house prices witnessed an increase of 11.1% to the new record median price of $950,000. This is up from $855,000 in same time last year, and an increase of $65,000 as compared to February 2020. March was a buoyant month for the broader residential property throughout New Zealand.

Prior to the spread of coronavirus, the property market of New Zealand was in a robust period of growth that now includes Auckland market, which had 5 consecutive months of YoY growth, after 2 years of price stability.

The effects of coronavirus are still questionable, but impact would be dependent on a number of factors, which include the level of unemployment, business and consumer confidence levels, ability of people to access finance as well as how much time the broader economy takes to recover. However, property happens to be a long-term investment while market recovery is on the ‘watch radar.’

New Zealand’s Plan of Action

As per the announcement by the Government official under housing ministry on May 9, 2020, building activities across the country have recommenced with all 300 work sites across New Zealand expected to be up and running again shortly. Another key message as unveiled by the Government is that real estate sector has been put forth to be one of the significant sectors in creating jobs and homes. Construction activity is one of the best investment destinations where one dollar spent is estimated to deliver three dollars in the wider economy.

It is also worth a mention that Kāinga Ora is a significant player in the space, with share of 7% in the country’s residential build market, and residential building accounts for half of all construction in New Zealand. Restart of operations sends strong signal across the industry and encourages to work hard for revival of the economy. Official stats suggest that Kāinga Ora has around 3,000 state, market and affordable homes under construction and contracted, valuing at around $1.5 billion. One third of 300 Kāinga Ora sites are in the Auckland region with another third in the Wellington region. Others are in Christchurch, Hamilton, and spread throughout other locations around the country.

Expectations to meet-up demand for quality homes to counter the increased demand is likely to be strong, and robust initiatives by the Government and better lending policies might support the overall scenario.

Drivers to Boost Real Estate Market Moving Forward

Commercial property market is expected to gain pace with the ease in restrictions along with strong government initiatives to drive the economy back on track. The key occupiers driving office sector growth are from finance, insurance and real estate sectors. Many tenants with non-availability of prime hotspots, opt for traditional leasing. However, the rise in coworking, serviced office space and other variations, with the focus on the small and medium enterprises and start-up sectors, are changing the dynamics of commercial market. Growing risk appetite, strong economic growth, along with ease in credit conditions have earlier led to the surge in commercial property prices.

Now that we have a broad idea of NZ real estate sector, let us now quickly have a look at some stocks in REITs space (APL, GMT, VHP and PFI)

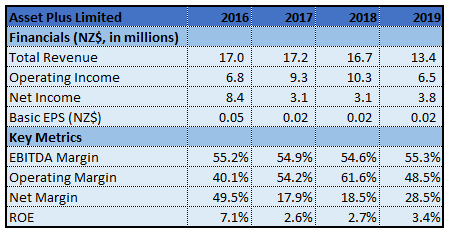

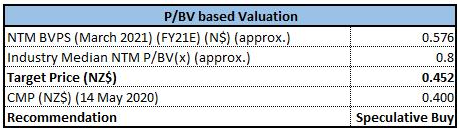

1. Asset Plus Limited (NZX: APL) (Recommendation: Speculative Buy, Potential Upside: Lower Double-Digit Growth) (M-Cap: ~$64.76 million, Gross Dividend Yield: 10.498%)

Business Description: Asset Plus Limited (NZX: APL) is a listed commercial property investment company investing solely in New Zealand real estate.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company has received a number of rent relief requests from tenants alongside claims for rental abatement in accordance with lease terms. Given the uncertainty regarding the length of the lockdown and ongoing conditions for the various alert levels, it is unable to currently quantify the impact of the lockdown for the 2021 financial year.

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: The company has conditionally agreed to develop a new office building for Auckland Council at Munroe Lane, Albany, Auckland. As per the release, Auckland Council would be occupying around two thirds of the building. APL has also confirmed that Auckland Council has agreed to extend satisfaction date for the funding as well as shareholder approval condition to July 31, 2020. We have applied P/BV based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

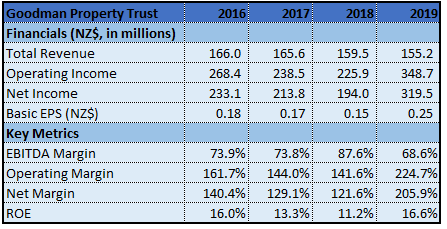

2. Goodman Property Trust (NZX: GMT) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~$3.09 billion, Gross Dividend Yield: 3.469%)

Business Description: Goodman Property Trust (NZX: GMT) is an externally managed, listed unit trust.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company’s investment strategy has been refined to meet the growing requirement for warehouse and distribution space across Auckland. The city’s industrial property market remains to be New Zealand’s best performing commercial real estate sector led by a strong regional economy. The company is expecting full-year distributions of 6.65 cents per unit.

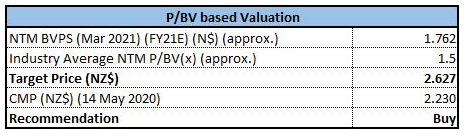

P/BV Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: New equity initiatives have also provided greater financial flexibility. The balance sheet capacity this has created will be invested into new opportunities over time. We have P/BV based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

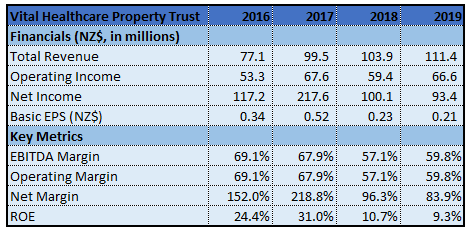

3. Vital Healthcare Property Trust (NZX: VHP) (Recommendation: Buy, Potential Upside: Lower Double-Digit) (M-Cap: ~$1.08 billion, Gross Dividend Yield: 4.356%)

Business Description: Vital Healthcare Property Trust (NZX: VHP) is an NZX-listed fund that invests in high-quality healthcare-related properties in New Zealand and Australia.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company’s tenants are hospital and healthcare operators who provide a wide range of medical and health services. The company started FY20 with a strong position. The company’s balance sheet has been strengthened by NZ$107 million of additional debt facilities as well as term extensions for near-term debt expiries. These enhancements to VHP’s financial flexibility and liquidity reflect that VHP now has more than NZ$243 million in undrawn debt facilities available from the long-term financiers and no debt expiring before March 2021 while only NZ$128.5 million expiring before September 2021.

P/E Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: The company stated that hospital operators in Australia (~60% of VHP’s revenue) have either agreed, or are in the process of finalising agreements, with each state government to give facilities as well as services during this pandemic. The operators are expected to recover significant portion of their costs from Australian governments. We have applied P/E based relative valuation (on an illustrative basis) and the target price reflects a growth of lower double-digit (in % terms).

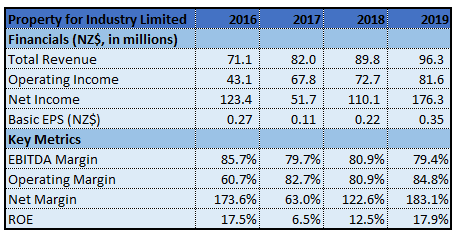

4. Property for Industry Limited (NZX: PFI) (Recommendation: Hold, Potential Upside: Higher Single-Digit) (M-Cap: ~$1.15 billion, Gross Dividend Yield: 4.379%)

Business Description: Property for Industry Limited (NZX: PFI) is an NZX listed property vehicle specialising in industrial property and its nationwide portfolio of 93 properties valued at over $1.4 billion dollars.

Key Metrics (Source: Refinitiv (Thomson Reuters))

Outlook: The company remains well placed to continue to take advantage of the current low interest rate environment. On 17th March 2020, the New Zealand Government announced the reintroduction of a depreciation deduction for commercial and industrial buildings. The company estimates that this deduction will result in an increase in Funds and Adjusted Funds from Operations (FFO and AFFO) earnings of approximately $1.85 million in FY20. The company has been working closely with its tenants to understand the impact of the COVID-19 virus on their operations.

EV/Sales Based Relative Valuation (Source: Refinitiv (Thomson Reuters)) (Illustrative)

Valuation: The company has recently made an announcement that it has secured a new $50 million liquidity facility from Commonwealth Bank of Australia, New Zealand Branch (or CBA). It stated that new facility is for 18 months and is in addition to bonds as well as syndicated bank facility the company already has in place. We have applied EV/Sales relative valuation method (on an illustrative basis) and have arrived at the target price which reflects a growth of higher single-digit (in % terms).

Comparative Price Chart (Source: Refinitiv (Thomson Reuters))

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...