Company Overview:

Delegat Group Limited (NZX: DGL) is a New Zealand-based wine company. The company invests in wineries and vineyards in the prime grape- growing regions of Australia and New Zealand. Foley Wines Limited (NZX: FWL) is an integrated wine company producing table wines with the marketing and sales of premium wines in New Zealand and various export markets.

Kalkine’s Sector Report covers the Key Financial Metrics, Risks, Outlook, Technical Analysis along with the Valuation, Target Price, and Recommendation on the stock.

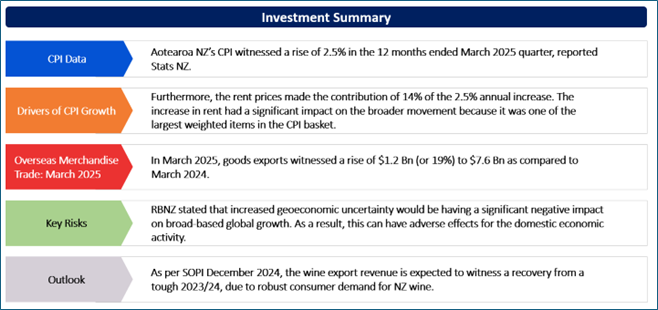

Aotearoa NZ’s CPI witnessed a rise of 2.5% in the 12 months ended March 2025 quarter, reported Stats NZ. The 2.5% rise follows a 2.2% annual increase to the December 2024 quarter. As per the release, the annual inflation rate remains within the RBNZ’s target band of 1% - 3% for the third consecutive quarter. Rent was the largest contributor to the annual inflation rate as it increased by 3.7%. Furthermore, the rent prices made the contribution of 14% of the 2.5% annual increase. The increase in rent had a significant impact on the broader movement because it was one of the largest weighted items in the CPI basket.

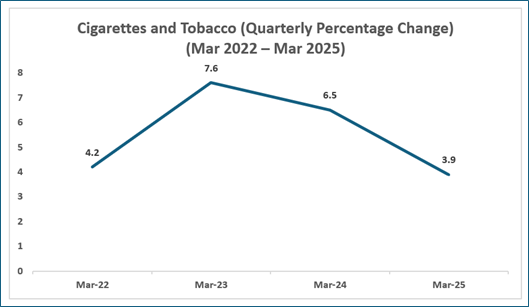

On 1 January 2025, for tobacco products, new excise duty rates came in. Notably, the cigarettes and tobacco prices witnessed a rise of 3.9% in the March 2025 quarter as compared to the December 2024 quarter. This rise in the price was lower than it was typically witnessed in a March quarter.

Exhibit 1: Cigarettes and Tobacco (Quarterly Percentage Change) (March 2022 – March 2025)

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

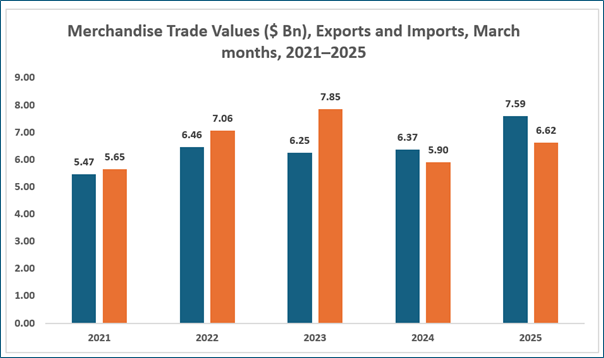

Overseas Merchandise Trade: March 2025

Stats NZ released data about overseas merchandise trade (March 2025). In March 2025, goods exports witnessed a rise of $1.2 Bn (or 19%) to $7.6 Bn as compared to March 2024. Over the same time period, goods imports increased $723 Mn (or 12%) to $6.6 Bn. Therefore, the monthly trade balance was a surplus amounting to $970 Mn. With respect to exports, milk powder, butter, and cheese increased $596 Mn (or 35%) to $2.3 Bn.

Talking about China, the total exports rose $371 Mn (or 23%) and the largest increases were witnessed in milk powder, butter, and cheese, up $287 million.

Exhibit 2: Merchandise Trade Values ($ Bn), Exports and Imports, March Months, 2021–2025

Data Source: This work is based on/includes MPI’s data which are licensed for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Electronic Card Transactions: February 2025

Stats NZ released data about electronic card transactions (March 2025). In March 2025 month, spending in the retail industries fell 0.8% (or $52 Mn) and spending in the core retail industries declined 0.8% ($46 Mn) as compared to February 2025. By retail spending category, durables were down by $39 Mn (or 2.5%), hospitality declined $14 M (or 1.1%), and fuel fell $12 Mn (or 2.3%). Notably, there was a decline of $76 Mn (or 3.3%) from February 2025 in the non-retail (excluding services) category. This category consists of medical and other health care, postal and courier delivery, travel and tour arrangement, along with several other non-retail industries.

Key Risks and Challenges:

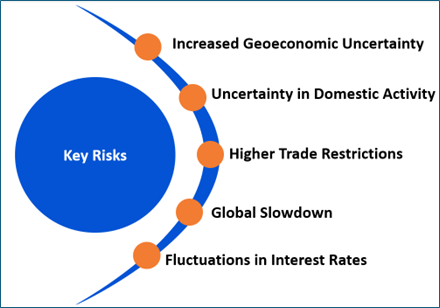

Recently, RBNZ stated that increased geoeconomic uncertainty would be having a significant negative impact on broad-based global growth. As a result, this can have adverse effects for the domestic economic activity. As per RBNZ, numerous factors resulting from the tariff increases can place some sort of upward pressure on global prices in the medium term. Also, the costs of trade can also witness a rise. This is because global supply chains would be adapting to the higher trade restrictions as well as geo-economic fragmentation.

Exhibit 3. Key Risks in Consumer Discretionary Sector:

Source: Analysis by Kalkine Group

Outlook:

As per SOPI December 2024, the wine export revenue is expected to witness a recovery from a tough 2023/24, due to robust consumer demand for NZ wine. Also, the apple and pear export revenue is expected to surpass $1.0 Bn. This would be helped by the recovering export volumes post the cyclone-impacted 2023 season. SOPI also highlighted that the fresh and processed vegetable export revenue can also recover, rising by 7%.

Also, the export revenue for the processed food and other products sector is expected to witness a rise of 1% to $3.5 billion for the year ended 30 June 2025. This is expected to be influenced by modest growth throughout most of the production categories, offsetting a fall in export revenue from inedible oils being exported for purposes including biofuel feedstock in the US.

Apart from the sector-specific factors, an analysis on 2 NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

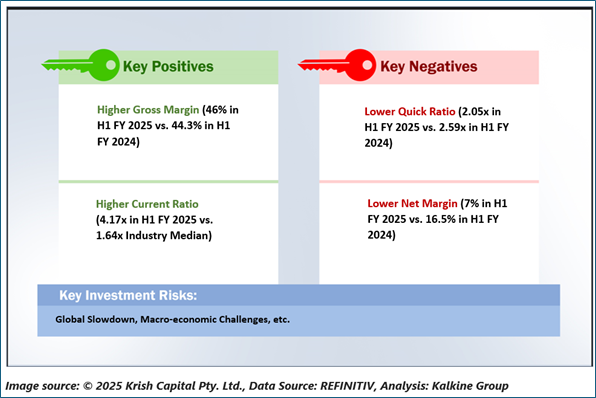

1) Delegat Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 384.2 Mn, Annual Dividend Yield: 7.31%)

Business Description:

Outlook:

DGL announced that it concluded the 2025 harvest and managed to deliver excellent quality across regions. DGL’s 2025 harvest stood at 47,461 tonnes, reflecting a rise of 39% on the low-yielding 2024 harvest of 34,150 tonnes. Furthermore, the figure also demonstrates 5% increase from the 2023 harvest of 45,340 tonnes. For FY 2025, the company is forecasting global case sales of 3,182,000 cases. DGL revised its guidance range on Operating NPAT to $47.0 million - $50.0 million for the same time.

Technical Overview:

DGL Daily Technical Chart, Data Source: REFINITIV

Technical Commentary

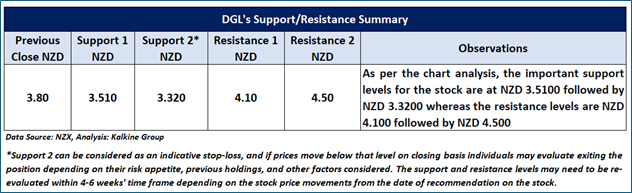

On the daily chart, while experiencing a downtrend, DGL’s stock prices broke below its previous trough during a downtrend, indicating a negative bias. Moreover, the momentum oscillator RSI (14-period) is heading southward from its midpoint, adding further evidence to the mentioned recommendation. Prices are trading its previous trough, which might function as resistance level for the stock; in contrast, the stock’s nearest round level may act as a support. A significant support level for the stock is positioned at NZD 3.51, while critical resistance level is located at NZD 4.1.

Fundamental Valuation

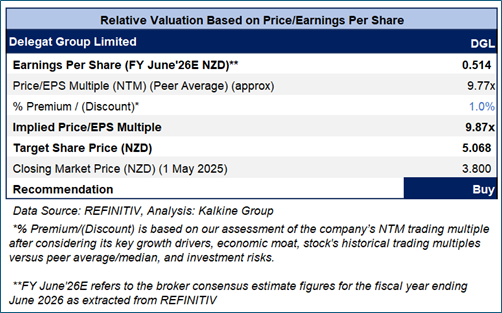

P/E Based Relative Valuation

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 3.80 pr share, down by 2.56% as on 1 May 2025.

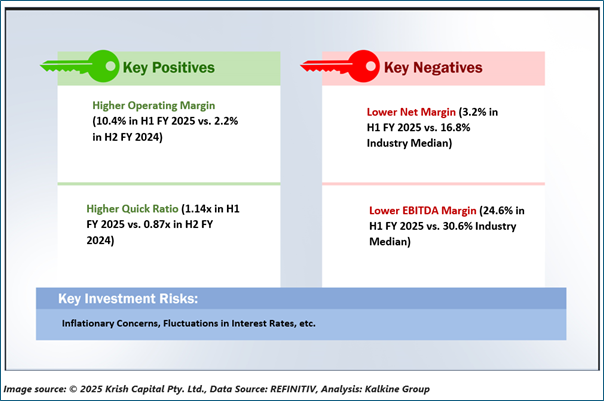

2) Foley Wines Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 39.4 Mn)

Business Description:

Foley Wines Limited (NZX: FWL) is a NZ-based integrated wine company.

Outlook:

FWL’s inventory remains in a good shape and is anticipated to roll on to the 2025 vintage on a timely basis, which can have a lower cost of goods. This is expected to result in increased gross margins, and considering the decline in interest rates, to an improved financial position for the 2026 year. The company has managed to establish routes to market for what it produces and is not dependent on the bulk wine market.

Technical Overview:

FWL Daily Technical Chart, Data Source: REFINITIV

Technical Commentary

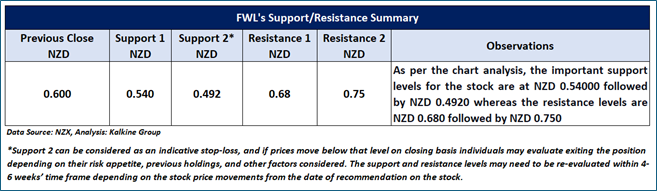

On the daily chart, FWL’s stock prices are forming a downtrend characterized by lower lows and lower highs, indicating a negative bias. Additionally, the momentum oscillator RSI (14-period) is trading below its midpoint, adding more support to the mentioned recommendation. Prices are trading between its previous peak and trough, which might function as a resistance and support levels for the stock, respectively. An important support level for the stock is situated at NZD 0.54, while crucial resistance level is placed at NZD 0.68.

Stock Recommendation

The stock price as on the close of 30th April 2025 was NZD 0.60 per share, the stock did not trade on 1st May 2025. Considering the facts above, a ‘Speculative Buy’ recommendation on the stock has been provided at the closing market price of NZD 0.60 per share as on 30th April 2025.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Note 5: Kalkine reports are prepared based on the stock prices captured either from REFINITIV or Trading View. Typically, REFINITIV or Trading View may reflect stock prices with a delay which could be a lag of 25-30 minutes. There can be no assurance that future results or events will be consistent with the information provided in the report. The information is subject to change without any prior notice.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer This report has been issued by Kalkine New Zealand Limited (FSP691351) (NZBN:9429047678101) (“Kalkine”). Kalkine is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity securities, managed funds and other managed investment schemes and other financial advice products. The recommendations and opinions in this report and on Kalkine website do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...