Company Overview:

Delegat Group Limited (NZX: DGL) is a New Zealand-based wine company. Restaurant Brands New Zealand Ltd (NZX: RBD) is the corporate franchisee which specialises in managing multi-site branded food retail chains.

Kalkine’s Sector Report covers the Key Financial Metrics, Risks, Outlook, Technical Analysis along with the Valuation, Target Price, and Recommendation on the stock.

I. Sector Landscape and Outlook

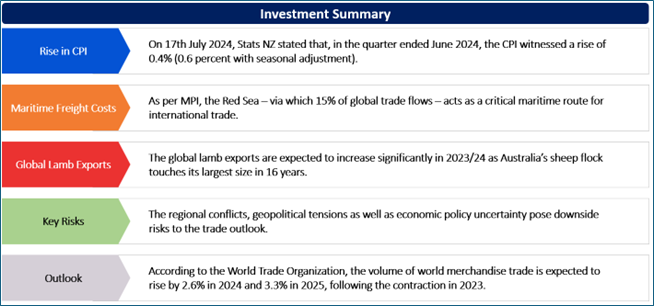

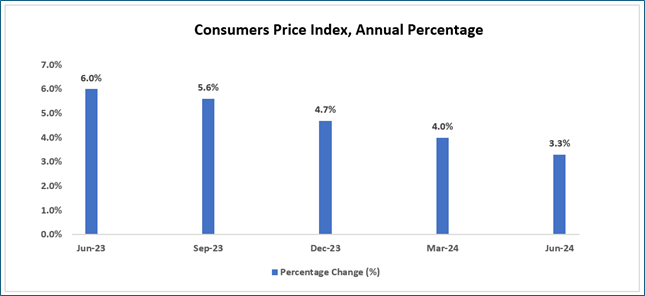

On 17th July 2024, Stats NZ stated that, in the quarter ended June 2024, the CPI witnessed a rise of 0.4% (0.6 percent with seasonal adjustment). The housing and household utilities increased 1.1%, influenced by actual rentals for housing (up 1.2%), home ownership (up 0.9%) and household energy (up 2.8%). Notably, miscellaneous goods and services witnessed a rise of 1.8%, influenced by insurance (up 3.1%), other miscellaneous services (up 1.2%) and personal effects (up 2.3%).

The largest downwards contributor to the 0.4% quarterly increase was recreation and culture, that declined 1.9%. For the 12 months ended June 2024 quarter, the CPI inflation rate stood at 3.3%.

As per Situation and Outlook for Primary Industries (or SOPI) (June 2024), in 2023/24, the prices as well as revenue for many exports have witnessed correction from highs in 2021/22 and 2022/23. This is because of cyclical nature of commodity markets with subdued global growth, specifically in the key export market China. Notably, the slowdown in global economic growth over previous 2 years is because of considerable surge in inflation, tightening of monetary policy as well as higher geopolitical tensions.

Looking ahead to the year to 30 June 2025, food and fibre sector export revenue is expected to rebound 6% to $58.1 Bn. This is despite elevated volatility and altered global trading landscape. Notably, strengthening export revenue in dairy, meat, forestry, horticulture, seafood, and processed food and other products sectors might drive growth.

Exhibit 1: Consumers Price Index, Annual percentage change, June 2023–June 2024 Quarters

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Rise in Maritime Freight Costs

As per MPI, the Red Sea – via which 15% of global trade flows – acts as a critical maritime route for international trade. The attacks on commercial ships in Red Sea as well as the Gulf of Aden since mid-November 2023 had unfavourable impact on trade. The global transportation costs have increased, implying rerouting of cargo from Suez Canal to the Cape of Good Hope. Notably, trade disruptions from climate extremes in Panama Canal impacted trade.

Because of these disruptions, maritime freight costs have increased. The Drewry World Container Index rose to $4,072 per 40-foot container on 23rd May 2024. This reflects an increase of 142% as compared to same week last year.

Global Lamb Exports Anticipated To Increase

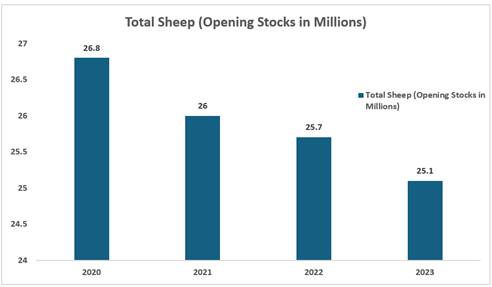

The global lamb exports are expected to increase significantly in 2023/24 as Australia’s sheep flock touches its largest size in 16 years. The Australian farmers have undergone extensive flock rebuilding after 2019 drought, leading to increased numbers of sheep available for slaughter as well as driving higher export volumes in 2023/24.

The Australian national flock rose 4% to 79 Mn head as at 30th June 2023. Notably, sheepmeat exports from Australia make up for ~50% of global sheepmeat exports by volume.

Australia’s sheepmeat export volumes witnessed a rise of 30% in 9 months ended 31 March 2024 as compared to same period in 2022/23. These increases follow the 12% rise in sheepmeat export volumes in 2022/23.

Exhibit 2: Sheep Numbers 2020–23

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Key Risks and Challenges:

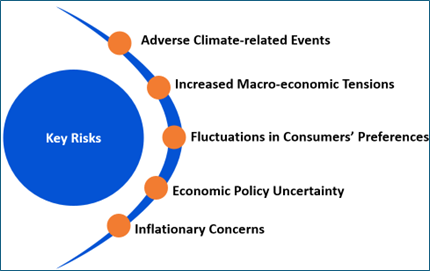

The regional conflicts, geopolitical tensions as well as economic policy uncertainty pose downside risks to the trade outlook. The resilience is being tested by disruptions on 2 of the world’s main shipping routes. These routes include the Panama Canal, that is impacted by freshwater shortages and the diversion of traffic away from the Red Sea as a result of attacks on merchant and naval vessels by Houthis.

Overall, consumer staples sector is exposed to risks including increased labour shortages, inflationary concerns, etc. Moreover, increased global meat production and a slowdown in Chinese economy could impact the meat prices.

Exhibit 3. Key Risks in Consumer Discretionary Sector:

Source: Analysis by Kalkine Group

Outlook:

According to the World Trade Organization, the volume of world merchandise trade is expected to rise by 2.6% in 2024 and 3.3% in 2025, following the contraction in 2023. In 2023, high energy prices as well as inflation weighed heavily on demand for manufactured goods, leading in 1.2% decline in world merchandise trade volume for 2023. Notably, the fall was larger in revenue terms with merchandise exports down 5% to US$24 trillion.

Even though productivity at the farm level is appearing to be good in NZ overall, the continuous improvements in the productivity and sustainability would be required to increase comparative and competitive advantage of food and fibre producers. The adoption of emerging agritech would be important to achieve this. Moving forward, agritech is expected to be an important driver of productivity growth and enabler of long-term sustainability in NZ’s primary industries. The agritech innovations are important for tackling environmental sustainability challenges in NZ’s agricultural sector.

Apart from the sector-specific factors, an analysis on three NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

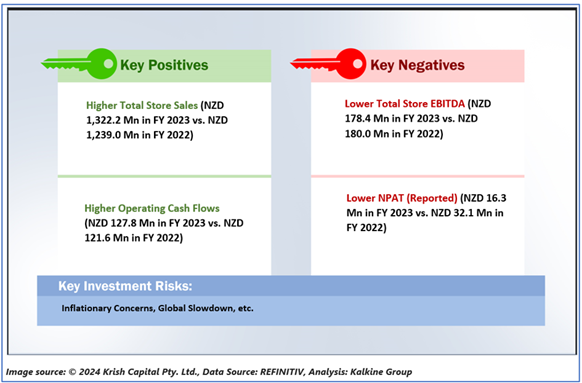

1. Restaurant Brands New Zealand Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 386.7 million)

Business Description:

Restaurant Brands New Zealand Ltd (NZX: RBD) is the corporate franchisee which specialises in managing multi-site branded food retail chains.

Outlook:

RBD is focused towards driving improved margins as well as higher profit levels while maintaining brand health, protecting the strong customer base as well as continuing to position the business to post sustainable long-term value. This is supported by ongoing strategic pricing and cost control programmes throughout all the markets, alongside deployments towards technology, product innovation, network expansion and brand experience.

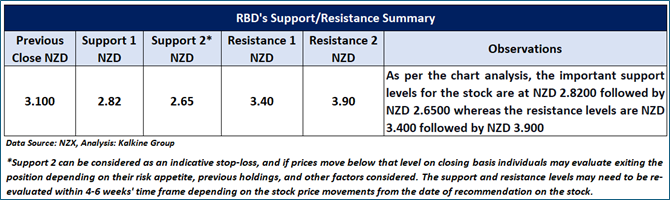

Technical Overview:

RBD Daily Technical Chart, Data Source: REFINITIV

Technical Commentary

On the daily chart, RBD’s stock prices are experiencing a downtrend, characterized by lower highs and lower lows, indicating a negative bias. Although the stock is currently in a minor rally, it showed signs of weakness when testing a major resistance at its previous peak, suggesting the downtrend might resume. The prices are fluctuating between the previous peak and trough, which may act as resistance and support levels for the stock, respectively. A significant support level is at NZD 2.82, while a crucial resistance level is at NZD 3.40.

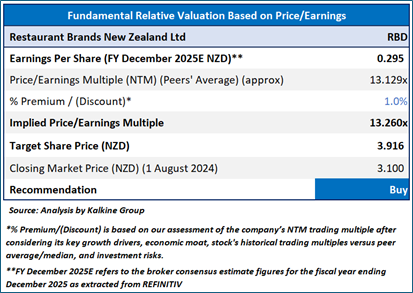

Fundamental Valuation

P/E Based Relative Valuation

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 3.10 per share, up by 1.31% as on 1 August 2024

2. Delegat Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 512.7 Mn, Annual Dividend Yield: 5.48%)

Business Description:

Delegat Group Limited (NZX: DGL) is a New Zealand-based wine company.

Outlook:

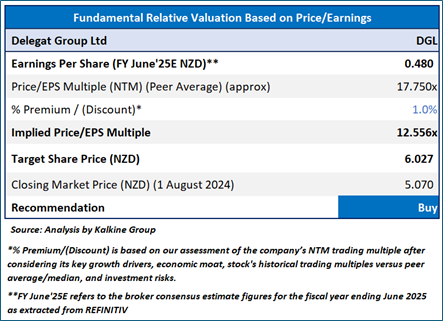

DGL stated that New Zealand remains the fastest growing country of origin with respect to premium US wine. The group maintains the FY 2024 Operating Profit guidance of $57 Mn - $61 Mn. Moving forward, ongoing deployment towards vineyard plantings and winery capacity expansion would support the future earnings growth. The Group implemented price increases globally, helping to maintain YoY operating revenue.

Technical Overview:

DGL Daily Technical Chart, Data Source: REFINITIV

Technical Commentary

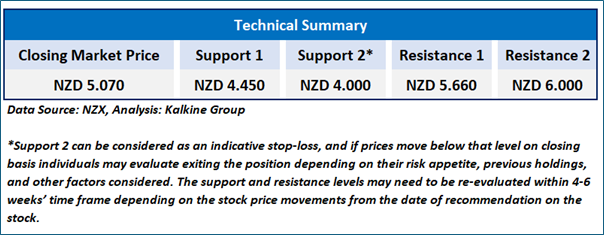

On the daily chart, while experiencing a downtrend, DGL’s stock prices are fluctuating between the two boundaries of a downward slope channel, suggesting that the current sideways period stock might continue to persist in the near future. Moreover, the momentum oscillator RSI (14-period) is trading near the midpiont, adding further evidence to the mentioned recommendation. Prices are trading between its previous peak and trough, which might function as resistance and support levels for the stock, respectively. A significant support level for the stock is positioned at NZD 4.45, while critical resistance level is located at NZD 5.66.

Fundamental Valuation

P/E Based Relative Valuation

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 5.07 per share as on 1st August 2024.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is August 1, 2024. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer This report has been issued by Kalkine New Zealand Limited (FSP691351) (NZBN:9429047678101) (“Kalkine”). Kalkine is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity securities, managed funds and other managed investment schemes and other financial advice products. The recommendations and opinions in this report and on Kalkine website do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...