Company Overview:

Delegat Group Limited (NZX: DGL) is a New Zealand-based wine company. The Colonial Motor Company Limited (NZX: CMO) owns motor vehicle dealerships throughout the country (NZ).

Kalkine’s Sector Report covers the Key Financial Metrics, Risks, Outlook, Technical Analysis along with the Valuation, Target Price, and Recommendation on the stock.

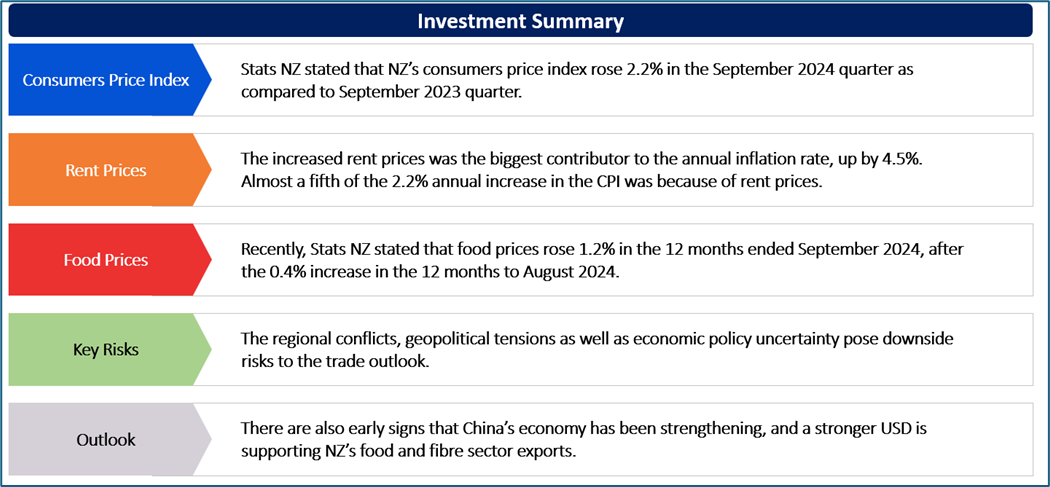

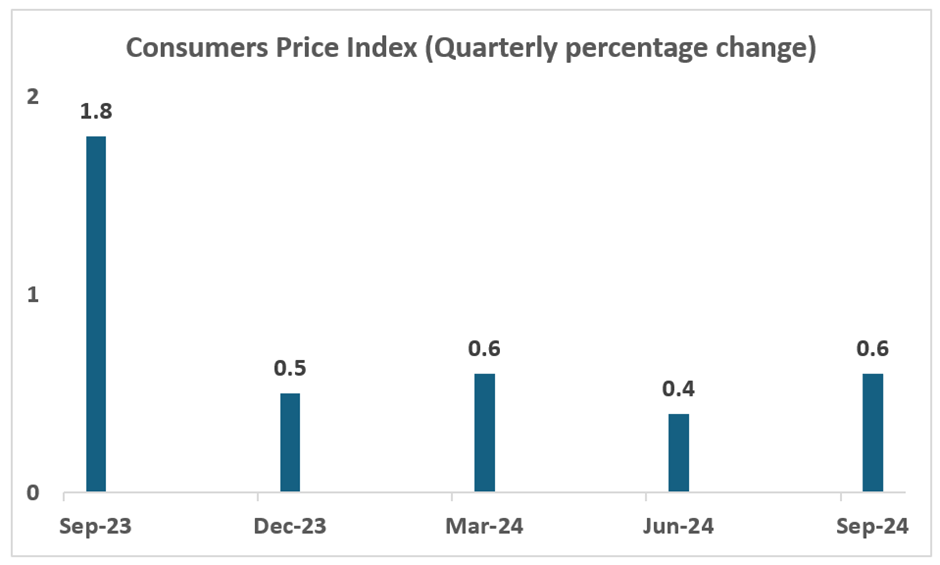

Stats NZ stated that NZ’s consumers price index rose 2.2% in the September 2024 quarter as compared to September 2023 quarter. For the first time since March 2021, the annual inflation was within the Reserve Bank of New Zealand’s target band of 1% - 3%. Prices are still rising, but not as much as was previously recorded. As per the release, increased rent prices was the biggest contributor to the annual inflation rate, up by 4.5%. Almost a fifth of the 2.2% annual increase in the CPI was because of rent prices.

Out of the 5 broad regions Stats NZ measures, the rent prices in the South Island excluding Canterbury had the biggest annual increase, rising by 6.6%. Notably, the Wellington had the smallest annual increase, up by 2.0%. The cigarettes and tobacco prices also witnessed an increase, rising 10.0% in the 12 months ended September 2024 quarter (14% contribution to the 2.2% increase). This increase was because of annual tobacco excise tax increase on 1 January 2024.

The lower petrol prices, which declined 8.0%, aided in offsetting rising prices.

Exhibit 1: Consumers Price Index (Quarterly percentage change) September 2023–September 2024 Quarters

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Increase in Food Prices

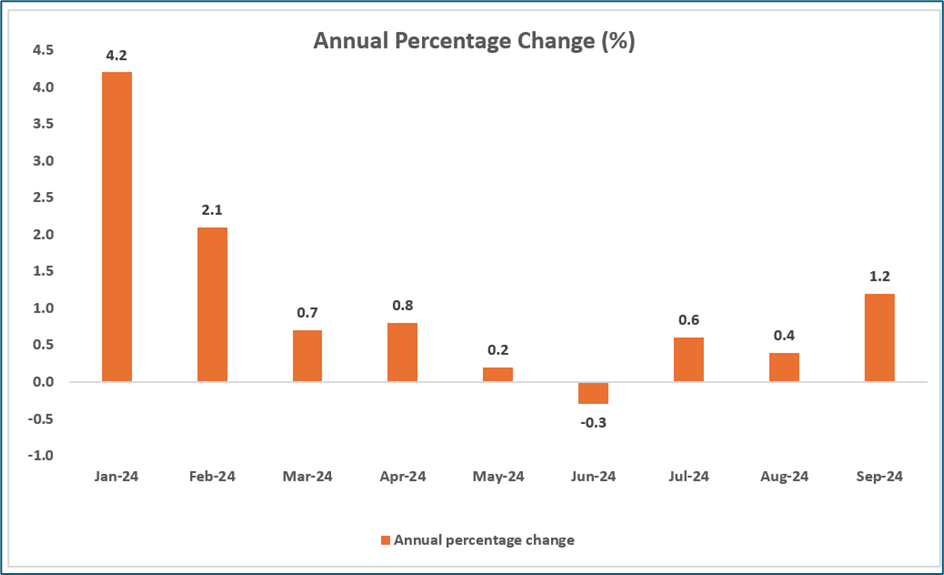

Recently, Stats NZ stated that food prices rose 1.2% in the 12 months ended September 2024, after the 0.4% increase in the 12 months to August 2024. Notably, the increased prices for restaurant meals and ready-to-eat food and grocery food drove the annual increase in food prices, rising 3.5% and 2.7%, respectively. The price increase in restaurant meals and ready-to-eat food because of increased prices for lunch/brunch, takeaway coffees, and hamburgers.

The price increase in grocery food was because of increased prices for olive oil, butter, and chocolate biscuits. As per the release, the price for a 1-litre bottle of olive oil rose by ~58% YoY, with an average price of $21.56. Despite an overall rise in food prices, decreasing prices in the fruit and vegetables group had the largest impact on food prices, declining 8.3% in the 12 months to September 2024.

Exhibit 2: Food prices (Annual Percentage Change)

Data Source: This work is based on/includes MPI’s data which are licensed by MPI for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Electronic Card Transactions: September 2024

Stats NZ released data about electronic card transactions (September 2024). In September 2024 month, the spending in retail industries remain unchanged as compared to August 2024. During the same period, the spending in the core retail industries rose 0.3% ($19 Mn). With respect to the retail spending category, hospitality rose by $12 Mn (or 1.0%), consumables increased $4.1 Mn (or 0.2%) and apparel rose by $3.6 Mn (or 1.1%).

The non-retail (excluding services) category rose $31 Mn (or 1.4%) from August 2024. This category includes medical and other health care, travel and tour arrangement, postal and courier delivery, and other non-retail industries. In actual terms, cardholders made 157 Mn transactions throughout all industries in September 2024, with an average value of $55 per transaction.

Key Risks and Challenges:

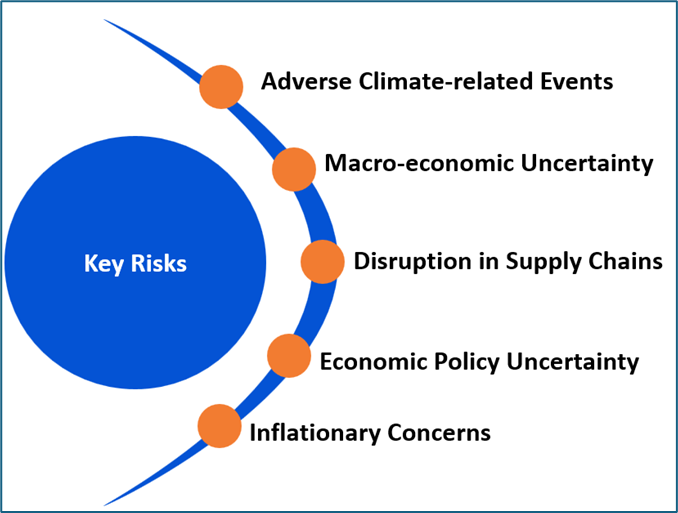

The regional conflicts, geopolitical tensions as well as economic policy uncertainty could impact the broader consumer discretionary sector of New Zealand. Additionally, the sector is exposed to risks such as increased labour shortages, inflationary concerns, etc.

The Consumer discretionary industry is cyclical in nature. Therefore, rising and falling interest rates, growth momentum in wages, unemployment or inflation could impact the broader consumer discretionary sector.

Exhibit 3. Key Risks in Consumer Discretionary Sector:

Source: Analysis by Kalkine Group

Outlook:

As per Situation and Outlook for Primary Industries (SOPI) (June 2024), there are expectations of sustained growth in overall food and fibre export revenue reaching $66.6 Bn for the year ended 30 June 2028. There are also early signs that China’s economy has been strengthening, and a stronger USD is supporting NZ’s food and fibre sector exports. While cost pressures remain, global shipping costs have remained well below the high levels seen in 2021/22. In addition, the energy and fertiliser prices have been declining faster than anticipated, with the latter nearing pre-pandemic levels, offering some relief for the farmers and growers. However, the prices are elevated, which is affecting on-farm profitability.

As per Situation and Outlook for Primary Industries (SOPI) (June 2024), the climatic conditions remained favourable for most crops recovering from the impacts of the previous wet summers as well as cyclone damage. Kiwifruit, apples, cherries, and vegetables witnessed increases in production. While there is temporary dips in some sectors, the outlook remains positive, and there continues to be robust demand for the high-quality food and fibre.

Over the previous 10 years, food and fibre exports have grown on average by 3.6% per year whereas other merchandise exports have grown by 1.6%. By 2021/22, 92% of the vineyards and wineries had initiatives to conserve or reduce water use with increased investment in new equipment which enables water efficiencies in the wine sector.

Apart from the sector-specific factors, an analysis on three NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Delegat Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 546.1 million, Annual Dividend Yield: 5.14%1)

Business Description:

Delegat Group Limited (NZX: DGL) is a NZ-based wine company. It invests in wineries and vineyards in the prime grape growing regions of New Zealand and Australia.

Outlook:

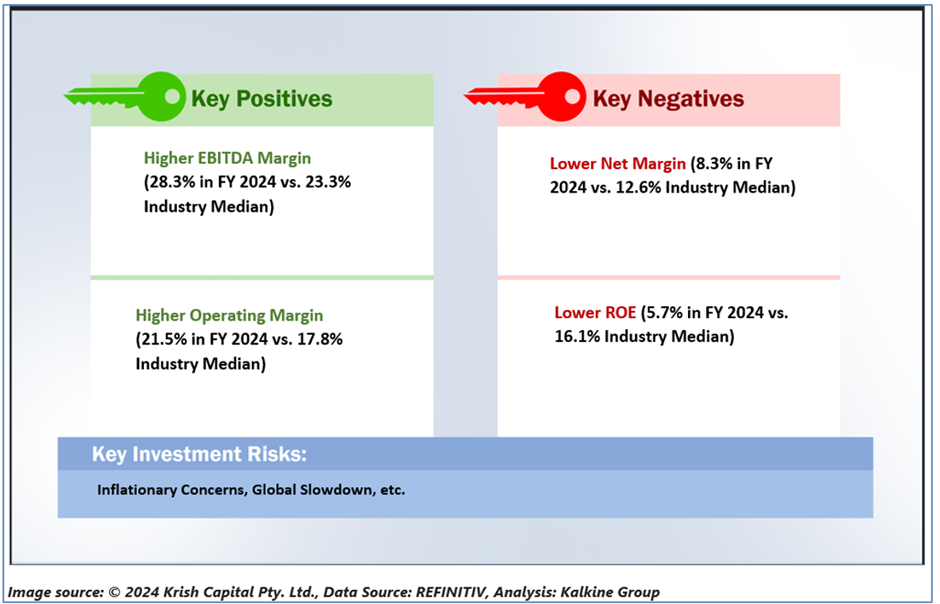

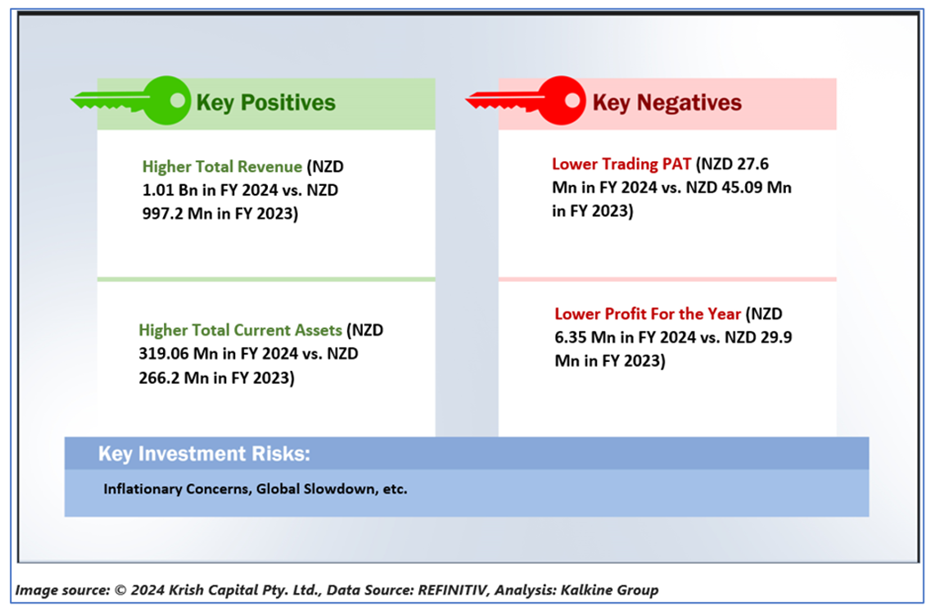

The company is confident in its ability to prosper and drive sustainable sales and earnings growth over the long term. With more than 96% of the wine sold offshore, DGL is the number one exporter of New Zealand wine. The group’s sales continue to be well diversified by market, with 48% in North America, 33% in the United Kingdom, Ireland and Europe, and 19% in Australia, New Zealand and the Asia Pacific region.

Technical Overview:

DGL Daily Technical Chart, Data Source: REFINITIV

DGL Daily Technical Chart, Data Source: REFINITIV

Technical Commentary

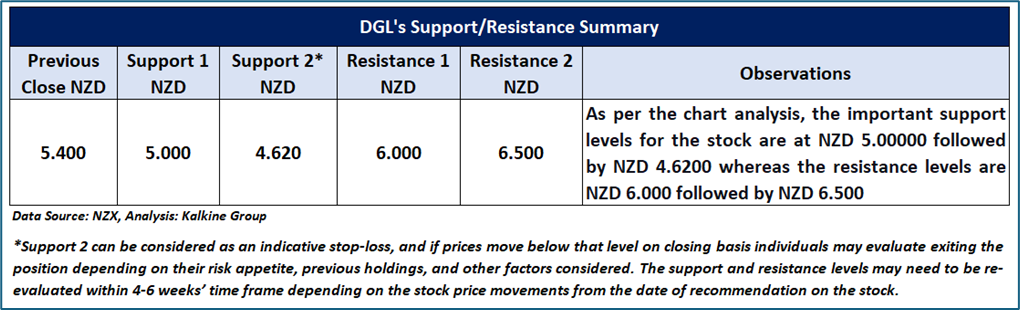

On the daily chart, while experiencing a downtrend, DGL’s stock prices are reversing from the upper boundary of a downward slope channel, indicating a negative bias. Moreover, the momentum oscillator RSI (14-period) is heading southward from its midpoint, adding further evidence to the mentioned recommendation. Prices are trading between its previous peak and trough, which might function as resistance and support levels for the stock, respectively. A significant support level for the stock is positioned at NZD 5.0, while critical resistance level is located at NZD 6.0

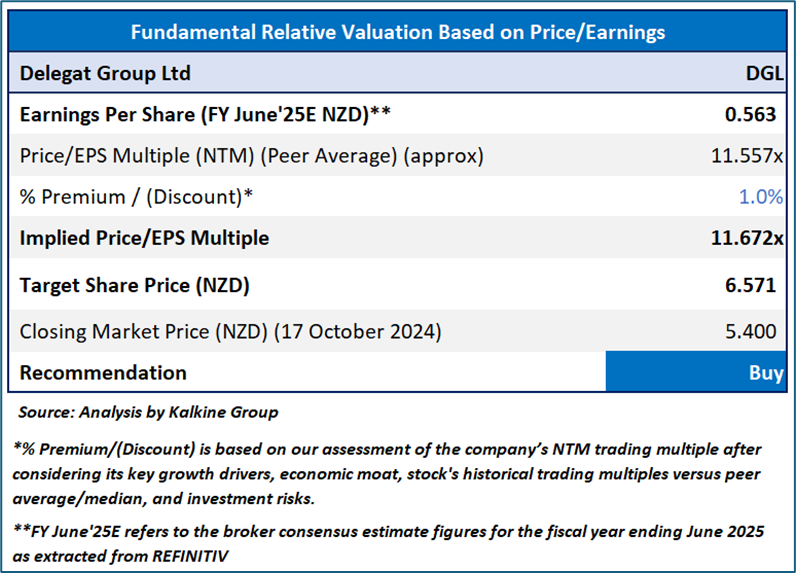

Fundamental Valuation

P/E Based Relative Valuation

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 5.40 per share, down by 1.82% as on 17 October 2024.

2) The Colonial Motor Company Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD 225.5 Mn, Annual Dividend Yield: 7.04%1)

Business Description:

The Colonial Motor Company Limited (NZX: CMO) owns motor vehicle dealerships throughout the country (NZ).

Outlook:

CMO is confident that the ongoing investment in the JAC Motors brand would be bearing fruit in future years. The team has been working through vehicle compliance, on-road testing and the set-up of a sales and service network. The Ranger and Everest are expected to maintain their momentum, offering a degree of support to the Ford dealerships. There has been one positive development which is the Government’s decision to align NZ and Australian emissions standards.

Technical Overview:

CMO Daily Technical Chart, Data Source: REFINITIV

Technical Commentary

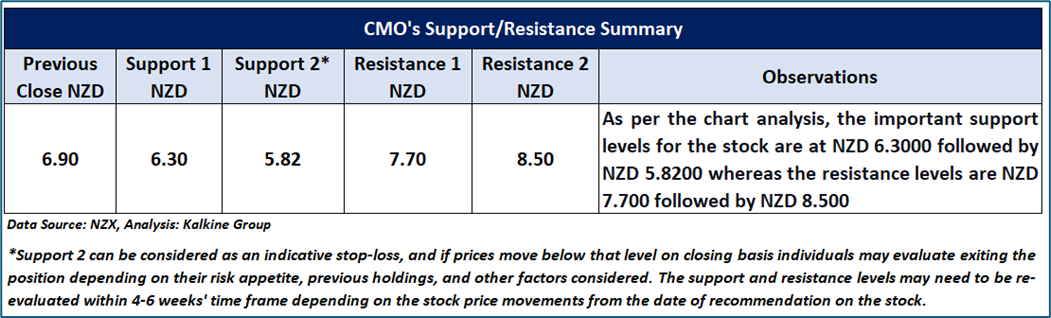

On the daily chart, CMO’s stock prices are forming a trading range during a downtrend, suggesting that the current sideways period in the stock might continue to persist in the near future. Moreover, the momentum oscillator RSI (14-period) is trading near its midpoint, providing more support to the previous observation. Prices are trading between its previous peak and trough, which might function as resistance and support level for the stock, respectively. A significant support level for the stock is located at NZD 6.30, while critical resistance level is placed at NZD 7.70.

Stock Recommendation

Considering the facts above, a ‘Buy’ recommendation on the stock has been provided at the closing market price of NZD 6.90 per share, up by 0.73% as on 17 October 2024.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is not a reliable indicator of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is October 17, 2024. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer This report has been issued by Kalkine New Zealand Limited (FSP691351) (NZBN:9429047678101) (“Kalkine”). Kalkine is a Financial Advice Provider (“FAP”) and is authorised by a Class 1 Financial Advice Provider Licence issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity securities, managed funds and other managed investment schemes and other financial advice products. The recommendations and opinions in this report and on Kalkine website do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...