Sector Landscape and Outlook

The real estate sector which comprises of residential as well as commercial property, among others plays a primary role in the economic development of the country. New Zealand housing sector is witnessing a sustained rapid growth along with boom in housing market for both residential as well as business purposes. With acceleration in demand, the housing sector is seeing favourable housing prices with record high prices particularly in Auckland, where prices are amongst the highest in the world. Therefore, huge investment is pumped into the sector, resulting broader level of employment prospects across business vertical. The robust property demand scenario in the country is clearly visible from the property transfers activities in the year ended December 2020 which stood at 152,532, driven by supportive fiscal policies and lucrative bank rates for housing.

Importantly, housing debt accounts for ~30% of the housing stock in value terms, while over 50% of the lending by banks are through mortgages.

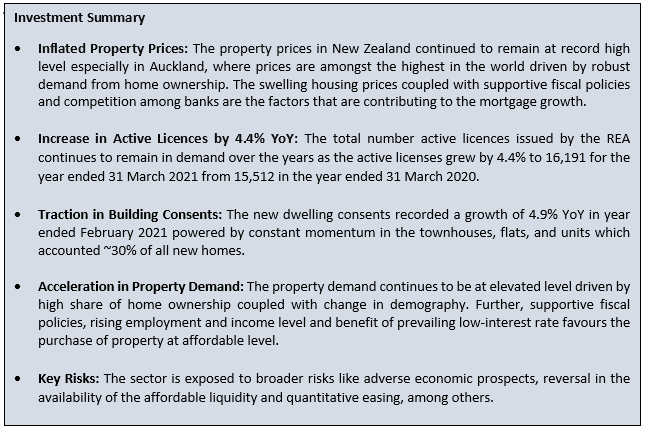

The S&P/NZX All Real Estate sector has slightly outperformed the S&P/NZX All Index with a 1-year return (15 April 2020 - 15 April 2021) of 20.63% as against the index’s 1-year return of 20.29%.

Exhibit 1: S&P/NZX All Real Estate (Sector) v/s S&P/NZX All Index (One-Year Chart) *

Source: S&P Global; Chart Created by Kalkine Group

*Till April 15, 2021

Housing Prices at Record High

The housing prices in New Zealand continued to soar to reach a record $826,300 in March 2021. According to the latest data from the Real Estate Institute of New Zealand (REINZ), which showed that the median residential property prices across the country rose by 24.3% YoY during the period from the level of $665,000 in March 2020. Further the record high median housing prices was witnessed across 12 regions and 32 districts. Importantly, the median housing prices without Auckland reached a new high as it reported a healthy growth of 23.6% YoY to $680,000. Meanwhile, the median housing prices in Auckland reached a new high of $1,120,000, up by 18.5% YoY.

Resultantly, the national median also recorded a robust growth of $46,300 from last month to touch a fresh record. The momentum in the housing prices are expected to prevail going forward, however the pace of growth is likely to be slower as compared to the pace over the last 6 to 12 months.

Decent Issue of Licences

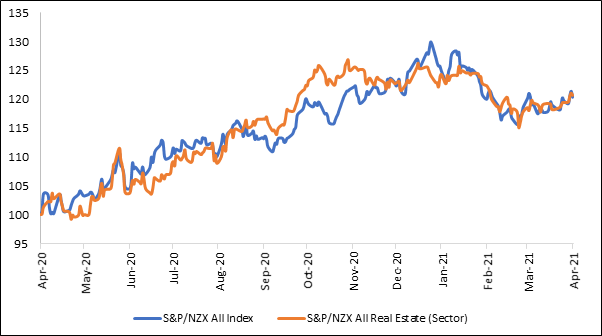

The real estate sector of the country is governed by the Real Estate Authority (REA) that provides licenses to the people as well as companies employed in the real estate industry. The total number of licenses issued by the REA for the year ended 31 March 2021 stood at 19,301, of which issued active licenses was 16,191, while the rest accounted for inactive licenses. Overall individual licenses issued during the period were 18,308, while 933 licenses were being issued to the company, as reflected in Exhibit 2 below.

Exhibit 2: REA Licensing Data (31 March 2021)

Source: REA NZ; Table Created by Kalkine Group

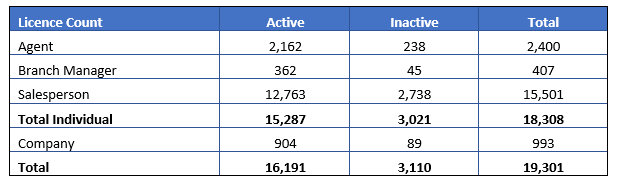

Notably, the overall active licenses issued by the REA continue to remain steady over the years from 31 March 2019 to 31 March 2021, which is visible from Exhibit 3 below.

Exhibit 3: Active Licences Trend

Source: REA NZ; Chart Created by Kalkine Group

Traction in Consumer Confidence

The consumer confidence in the country’s real estate sector has increased in 2020 with acceleration witnessed across all parameters, as visible in exhibit 4 below. This has been driven by enhanced professional, competent licensees, and effective redressal mechanisms. The below depicts the percentage of consumers who have rated each attribute 4 or 5 where 5 rating was given when a consumer feels a lot of confidence.

Exhibit 4: Consumer Confidence in the Real Estate Industry

Source: REA NZ; Chart Created by Kalkine Group

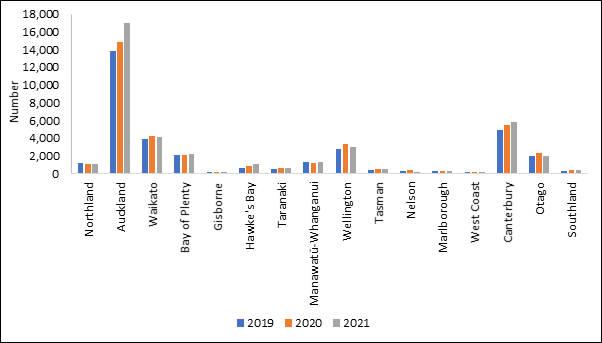

Rise in Building Consents in the Year Ended February 2021

The country witnessed an improvement in the actual number of new dwellings consented during the year ended February 2021. This reported a growth of 4.9% YoY to 39,725 with Auckland region witnessing the highest number of new dwellings consent up by 15% YoY to 17,060 followed by Canterbury and the rest of North Island that reported a growth of 7.2% YoY and 6.1% YoY to 5,859 and 6,308, respectively.

The rise in new homes was led by townhouses, flats, and units which accounted for ~30% of all new homes. The new houses posted a growth of 37.7% in the year ended February 2021 to around 12,000 over previous year.

Exhibit 5: Region Wise New Dwellings Consented for the Year Ended February 2019–2021

Source: Stats NZ; Chart Created by Kalkine Group

While, in February 2021 alone, the new dwellings consented rose ~3% from the previous month to 3,129, where stand-alone houses contributed 1,944 and the townhouses, flats, and units contributed 884 units. While the new dwellings consented for retirement village units and apartments stood at 155 and 146, respectively.

Ease in Non-Residential Construction

However, the total value of consents for non-residential buildings for the year ended February 2021 witnessed a fall of 2.7% YoY to $7.1 billion. This was weighed by the reduction in values of shops, restaurants, and bars which were down $298 million along with a decline in values of social, cultural, and religious buildings by $192 million and hostels, boarding houses, and prisons by $178 million. However, the uptick in the value of consents for education buildings as well as storage buildings by $267 million and $232 million have restricted the overall decline during the period.

Outlook

The demand prospect of the country’s real estate sector has predominantly been driven by the prevailing employment scenario. New Zealand witnessed a rebound in the employment generation in the December 2020 quarter after a straight two-quarters of continuous decline. The seasonally adjusted number of employed people in the December 2020 quarter increased by 17,000 against a decline of 7,000 and 19,000 in the June 2020 quarter and September 2020 quarter, respectively.

Separately, economic prospects of the country coupled with rising population level, record low-interest rate environment as well as access to easy funding are also driving the demand momentum of the real estate sector of the country. The benefits of these opportune scenarios have been reflected in the momentum in the construction sales which recorded an uptick of 4.8% YoY to $19.6 billion in the December 2020 quarter. This was followed by 8.9% YoY growth in the September 2020 quarter supported by traction in home building and construction services.

Key Risks and Challenges:

With record-low borrowing cost that is driving the demand for the real estate sector, housing prices have reached at its high level in the country. This is hindering the buyers with lower incomes to participate in the housing market where demand is outpacing supply. Moreover, the anticipation of continued high housing prices would lead to a property bubble and a burst in property prices.

Further, a slowdown in economic growth and adverse economic prospects would have a negative impact on the employment generation and resultantly would unfavourably effect demand. Importantly, the recent data from Stats NZ suggests that the unemployment level in the country fell to 4.9% in the December 2020 quarter as compared to the unemployment level of 5.3% in the September 2020 quarter.

Exhibit 6: Key Risks in Real Estate Sector

Source: Analysis by Kalkine Group

Apart from the sector-specific factors, we have also analyzed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Property for Industry Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.43 billion, Gross Dividend Yield: 3.445%)

Business Description:

Property for Industry Limited (NZX: PFI) is an NZX listed property vehicle specializing in industrial property. It has a nationwide portfolio of 93 properties, valued at over $1.47 billion.

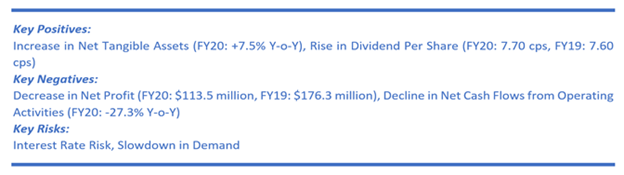

Outlook:

Its portfolio strength is reflected by the weighted average lease term that stood at 5.28 years with a sturdy occupancy level of 99.4% and just 3.3% of contract rent that is slated to expire in 2021. Further, the company has a strong balance sheet with 7.5% growth in net tangible assets to 220.9 cents per share along with availability of additional bank facility. Further its healthy liquidity position of more than $110 million, with a gearing of 30.0% also aided to its balance sheet strength.

Meanwhile, the company has raised its dividend guidance for 2021 to be in the range of 7.85-7.90 cents per share driven by strong results performance in 2020 along as well as robust balance sheet and expected growth from the rental business.

Moreover, in 2021 the company will continue to focus on acquisitions of core industrial properties to drive further growth.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

.png)

Stock Recommendation

The stock price reported a de-growth of ~1.39% in 3 months, while in 9-month and 1-year the stock grew by ~16.39% and ~41.29%, respectively. The stock is trading marginally higher than the average of the 52-week high price of $3.01 and 52-week low price of $2.01.

We have applied EV/Revenue based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to EV/Revenue Multiple (NTM) (Peer Average) considering its sustained focus on acquisitions of core industrial properties, significant investment in its core industrial property and divestment of non-core property which has cemented it at better position to benefit from trends supporting long-term growth.

For this purpose, we have taken peers like Asset Plus Ltd (API.NZ) and Goodman Property Trust (GMT.NZ).

Considering its decent FY20 financial performance, portfolio strength as well as strong balance sheet with high levels of liquidity and decent outlook, we give a “Buy” recommendation on the stock at the current market price of $2.84 per share, up by 0.53% on 15th April 2021.

2) Fletcher Building Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$5.803 billion, Gross Dividend Yield: 1.712%)

Business Description:

Fletcher Building Ltd (NZX: FBU) is engaged in a diversified business which ranges from manufacturing building products, distribution of building products, residential and development, construction, among others. It is also a fully integrated manufacturer of cement, through its Golden Bay Cement business.

Outlook

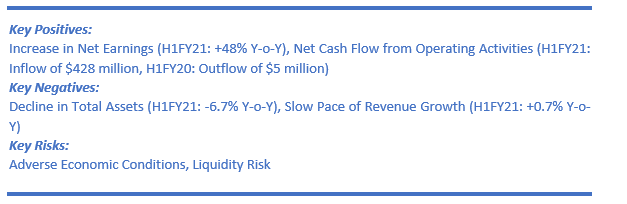

The company has witnessed growth in NZ Core and Residential housing which has been offset by softer demand in commercial and mixed conditions in infrastructure in New Zealand and Australia. Driven by its sustained focus on efficiencies of its operations along with the benefits of pricing disciplines, targeted share gains, consolidation and automation of manufacturing and supply chains and better overhead cost base, the company has logged sustainable improvement in margins. Owing to its strong cash generation and balance sheet strength, the company has declared interim dividend of 12.0 cents per share and expects to declare a final FY21 dividend.

Based on current indicators, the company expects the core volumes in New Zealand and Australia to remain at present levels in H2FY21 driven by robust demand for residential housing in New Zealand. Meanwhile, it has guided its FY21 EBIT before significant items to be in the range of $610-$660 million.

.png)

Stock Recommendation

The stock price reported a growth of ~17.61% in 3 months, while in 9-month and 1-year the stock grew by ~104.62% and ~76.56%, respectively. The stock is trading marginally higher than the average of the 52-week high price of $7.31 and 52-week low price of $3.16.

We have applied EV/EBITDA multiple based relative valuation (on an illustrative basis) and the target price reflects a rise of low double digit (in % terms). We have applied a slight premium to the peer average EV/EBITDA (NTM Trading Multiple) considering its sustained focus on enhancing the underlying disciplines as well as efficiencies of its operations across businesses and better working capital management. For this purpose, we have taken peers like Boral Ltd (BLD.AX), Incitec Pivot Ltd (IPL.AX) and Genesis Energy Ltd (GNE.NZ). Meanwhile, investors should keep any eye on softer commercial as well as AU civil markets and reduced revenue on legacy projects.

Considering its robust H1FY21 results performance, strong liquidity position, balance sheet strength and decent outlook, we give a “Buy” recommendation on the stock at the current price of NZ$7.040 per share, up by 0.43% on 15th April 2021.3) Goodman Property Trust (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.186 billion, Gross Dividend Yield: 2.860%)

Business Description:

Goodman Property Trust (NZX: GMT) is engaged in the business of owning, developing, and managing industrial real estate globally, which includes logistics facilities, warehouses, and business parks. It has a robust property portfolio of $3.3 billion with 11 properties under management in New Zealand.

Outlook

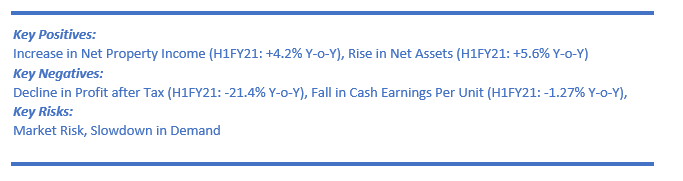

The company enjoys the benefit of a well-capitalised balance sheet which has aided in exploring potential new investment opportunities for growth. Its balance sheet strength is reflected by its loan to value ratio which stood at just 21.5%. Further driven by the benefits of refinancing of bank facility which has not only increased the weighted average debt term to 5.1 years at the end of 30 September 2020 from 4 years as on 31 March 2020 but has also provided $400 million of available funding capacity at the end of 30 September 2020. Therefore, this will enable the company to tap future investments. Meanwhile, the company expects its FY21 cash earnings to be at least 6.3 cents per share driven by an improved favourable economic outlook.

Valuation Methodology: EV/EBITDA Based Relative Valuation (Illustrative)

.png)

The stock price declined by ~5.56% in 6 months, while in 9-month and 1-year the stock grew by ~6.99% and ~5.52%, respectively. The stock is trading marginally higher than the average of the 52-week high price of $2.52 and 52-week low price of $2.03.

We have applied EV/Revenue based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight premium to EV/Revenue Multiple (NTM) (Peer Average) considering its healthy occupancy level, followed by its well-capitalized balance sheet and targeted investment strategy.

For this purpose, we have taken peers like Asset Plus Ltd (API.NZ) and Parkway Life Real Estate Investment Trust (PWLR.SI).

Meanwhile, investors should keep an eye on its higher debt level. However, considering, its sustained strong demand for property, robust underlying rental growth across its portfolio, improvement in business performance and a high-quality portfolio focused on urban logistics, we give a “Hold” recommendation on the stock at the current price of NZ$2.29 per share, down 0.87% on 15th April 2021.

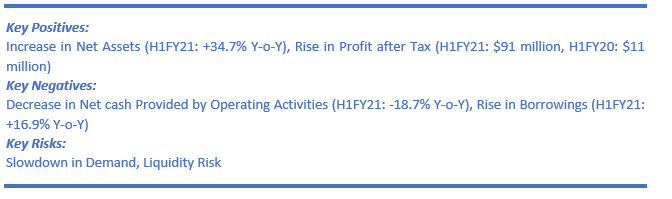

4) Investore Property Ltd (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$0.795 billion, Gross Dividend Yield: 4.070%)

Business Description:

Established in October 2015, Investore Property Ltd (NZX: IPL) is engaged in a commercial property ownership business which deals in investing in quality large format retail property assets.

Outlook

The company’s focus on large format stores as well as portfolio mix, that is largely skewed towards nationally recognised tenants, focus on “everyday needs” including supermarkets and benefit of geographical diversification provides an added advantage in withstanding the adverse impact of Covid-19. Moreover, IPL is eyeing on targeted growth to enhance its portfolio and boost growth through potential acquisitions and development of the existing portfolio, including refurbishment of stores. Meanwhile, the company has guided dividend of 7.60 cps for FY21.

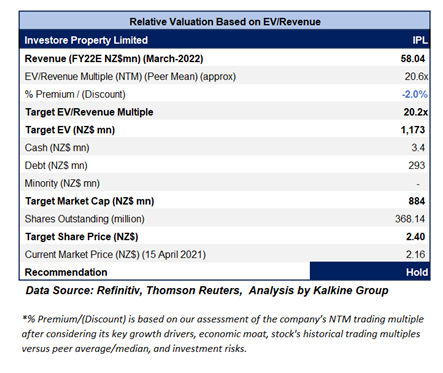

Valuation Methodology: EV/Revenue Based Relative Valuation (Illustrative)

Stock Recommendation

The stock price declined ~4.42% in 6 months, while the 9-month and 1-year prices grew ~12.50% and ~25.58%, respectively. The stock is trading marginally higher than the average of the 52-week high price of $2.29 and 52-week low price of $1.66.

We have applied EV/Revenue based relative valuation (on an illustrative basis) and the target price reflects a rise of low double-digit (in % terms). We have applied a slight discount to EV/Revenue Multiple (NTM) (Peer Average) as the company is anticipating lower gross rent receivable of around $1 million in FY21 as against the earlier guidance of $1-$2 million, which is a cause of concern for investors. However, the company expects growth in gross valuation of its property portfolio in H2FY21, through its continued focus on growth strategies through potential acquisitions and development of the existing portfolio.

For this purpose, we have taken peers like Asset Plus Ltd (APL.NZ), Goodman Property Trust (GMT.NZ), Vital Healthcare Property Trust (VHP.NZ), to name a few.

Given resilient portfolio and prudent capital management, and decent outlook, we give a “Hold” recommendation on the stock at the current market price of $2.160 per share, down by 0.46% on 15th April 2021.

Comparative Performance Chart (Source: Refinitiv, Thomson Reuters)

Note: Investment decision should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the Valuation has been achieved and subject to the factors discussed above.

Disclaimer

Kalkine New Zealand Limited is authorised to provide class advice only. The information on this site does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...