I. Sector Landscape and Outlook

As per the Ministry of Housing and Urban Development (HUD), the government planned a $3.8 billion Housing Acceleration Fund (HAF) focused on strengthening and scaling homebuilding. It aims to boost the mix of private-sector and government-led developments in areas with the highest housing supply and affordability challenges. The HAF is complemented by:

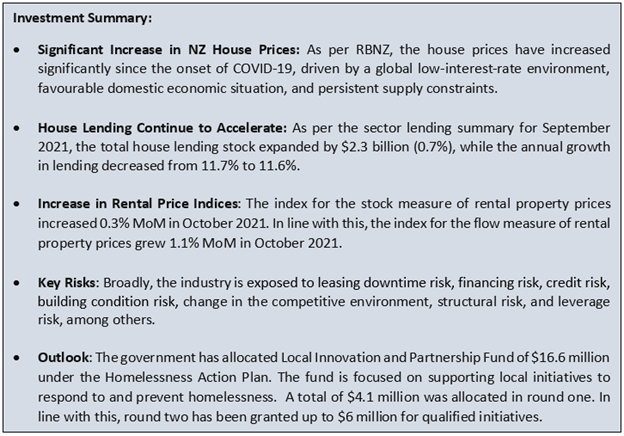

New Zealand House Prices Have Grown Significantly

As per the Reserve Bank of New Zealand (RBNZ), house prices have increased significantly since the onset of COVID-19, driven by a global low-interest-rate environment, favourable domestic economic situation, and persistent supply constraints. The low mortgage interest rates in the past 18 months indicate both a long-term, global trend and a cyclical response to a lower inflation and employment outlook. Market momentum has been retained robustly, although at a slightly slower pace in recent months. Valuation metrics like price-to-rent ratios indicate that prices are vulnerable to a fall as interest rates rise from their recent lows.

Exhibit 1: Value of Housing – Reporting a growth of ~91.2% Since March 2015 to March 2021

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

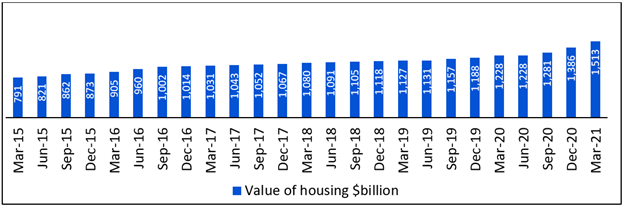

Housing Lending Continue to Increase in September 2021

RBNZ's total housing lending stock expanded by $2.3 billion (0.7%), rebounding marginally from August 2021 low. Meanwhile, the annual increase in lending decreased from 11.7% to 11.6% in September 2021. In addition, the total personal consumer lending stock was down by $252 million (1.9%) in September 2021, and annual growth decreased to -8.9%. Further, the entire business lending stock increased for the fifth consecutive month, up by $1.0 billion (0.9%), and the annual growth rose to 2.9% from 1.7%. On the other hand, total agriculture lending stock fell by $196 million (0.2%), with its yearly growth remaining negative at -0.9% in September 2021.

Exhibit 2: Trend in Lending Since September 2018 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

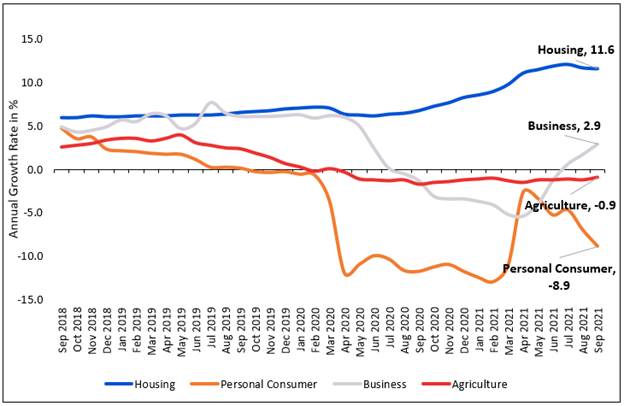

Rise in Rental Price Indexes – Changes in Prices That Households Pay for Housing Rentals

As per Stats.NZ, the index for the stock measure of rental property prices, increased 0.3% MoM in October 2021. In line with this, the index for the flow measure of rental property prices grew 1.1% MoM in October 2021. Also, the stock index rose by 3.3% YOY in October 2021, and the flow index increased by 5.8% YOY in October 2021. The flow measure captures the fluctuation in rental price only for dwellings that have a new tenancy started in the reference month, as it tends to be more volatile than the stock movement. This indicates rental price changes across the whole rental population, including renters currently in tenancies.

Exhibit 3: Trend in Monthly Percent Change in Rental Price Indexes, Oct 2019–Oct 2021

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

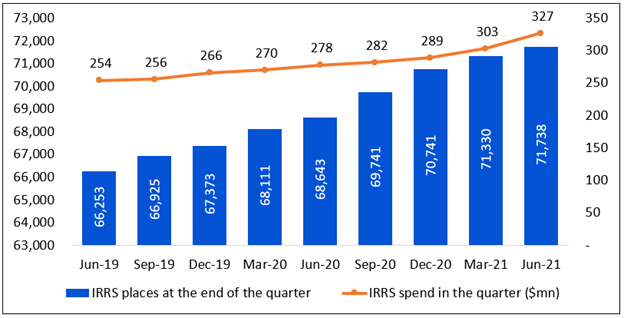

Increase in IRRS Payments for Individual Housing

As per the public housing quarterly report June 2021, published by the Ministry of Housing and Urban Development, Income-Related Rent Subsidy (IRRS) payments for individual households grew in June 2021 quarter from last quarter, with the total number of IRRS tenancies rising by 408 over the June quarter. Most public housing tenants (71,738) receive IRRS. A further 763 public housing tenants pay market rent. The public housing provider fixes market rent as per comparable rent charged for other properties of a similar type, size, and location.

Exhibit 4: Trend in Income-Related Rent Subsidy Since June 2019 Quarter

Data Source: This work is based on/includes hud.govt.nz which are licensed by Te Tūāpapa Kura Kāinga - Ministry of Housing and Urban Development on behalf of the Crown for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

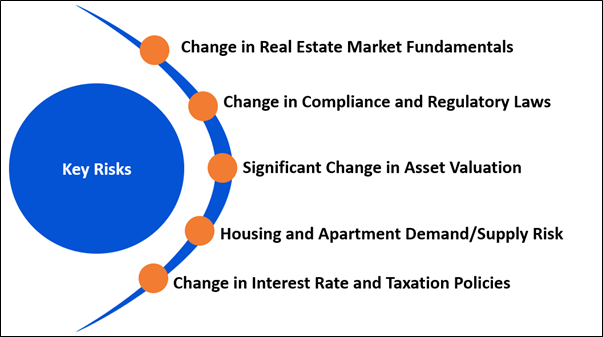

Key Risks and Challenges:

As per RBNZ, rising inflationary pressure is pressuring some central banks to think about reducing monetary stimulus, while others are closely monitoring current inflation as largely transitory and needed to support growth. The continuing rise in inflation could prompt a faster increase in interest rates. Further, weaker economic growth could lead to a fall in asset valuations and a rapid tightening in financial conditions. Meanwhile, the valuation metrics like price-to-rent ratios indicates that housing prices are vulnerable to a fall as interest rates rise from their recent lows.

Exhibit 5. Key Risks in Real-Estate Sector:

Sources: Analysis by Kalkine Group

Outlook:

As per HUD, the government has parked Local Innovation and Partnership Fund of $16.6 million under the Homelessness Action Plan. The fund is focused on supporting local initiatives to respond to and prevent homelessness. A total of $4.1 million was allocated in round one, in the 2H’2020. In round two of the fund, up to $6 million will be allocated to qualified initiatives that meet the criteria and align with the fund's priorities. In addition, a slice of the fund, $1 million, will be allocated to small grants.

As per RBNZ, the equities and other income-producing assets (like Housing) have realized continued growth in valuations because of lower interest rates. Further, the financial market health remains accommodative, driven by low sovereign yields, tight credit spreads, and high equity prices. However, there are concerns about the potential discrepancy between asset prices and relevant long-term earnings potential as per current circumstances. Moreover, the near-term outlook for global economic growth has weakened somewhat because of the spread of the Delta variant, rising energy prices, ongoing supply chain issues, and an indicative slowdown in the Chinese real estate market.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Kiwi Property Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.77 billion, Gross Dividend Yield: 5.736%)

Business Description:

Kiwi Property Group Limited (NZX: KPG) is a property company that owns and manages a real estate portfolio comprising retail and office buildings. The objective is to provide a reliable investment in New Zealand property through the ownership and active management of a diversified, high-quality portfolio.

Outlook:

The company enters FY22 with solid momentum and a clear focus to create value for shareholders and other stakeholders. As per the management, the year ahead can be decisive for the company. It advances the delivery of its strategy, reduces retail exposure, and extends the journey to create mixed-use spaces inspired by the people and places of Aotearoa.

On 21 September 2021, the company confirmed to move ahead with the construction of NZ’s first significant build-to-rent development, demonstrating a crucial milestone in delivering a mixed-use strategy.

As per the release dated 28 October 2021, the company confirmed to release its interim results for the six months ended 30 September 2021 on 22 November 2021.

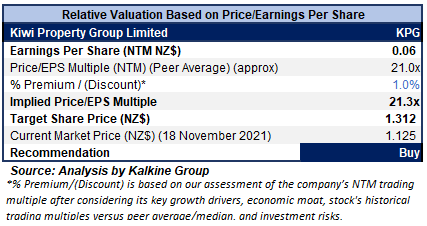

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

.png)

Stock Recommendation

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price of low double-digit rise (in percentage terms). The company might trade at a slight premium to its peers’ average, considering a better net margin of 84.0% in FY21 versus an industry median of 49.8%. Also, the ROE rebounded from -9.3% in FY20 versus +9.6% in FY21.

We have taken peers such as Precinct Properties New Zealand Ltd. (PCT.NZ), Vital Healthcare Property Trust for the valuation purpose. (VHP.NZ), and Stride Property Ltd. (SPG.NZ), to name a few.

Considering the factors above, along with its healthy liquidity position and decent outlook, we give a “Buy” recommendation on the stock at the current market price of $1.125 per share as of 18th November 2021 (New Zealand Time: 12:21 PM (GMT +12).

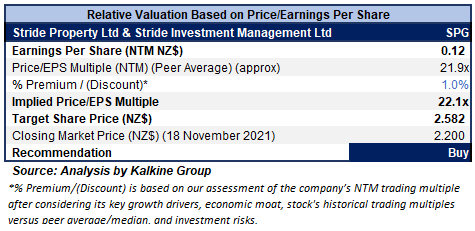

2) Stride Property Ltd & Stride Investment Management Ltd (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$1.04 billion, Gross Dividend Yield: 5.661%)

Business Description:

Stride Property Ltd & Stride Investment Management Ltd (NZX: SPG) consists of Stride Investment Management Limited (SIML) and Stride Property Limited (SPL). SIML is an investment manager and staff employer for the group company, and SPL owns the property portfolio and has an ownership interest in each of the Stride portfolios.

Outlook

On 21 September 2021, the company announced a withdrawal from the current demerger plan and the IPO of Fabric Property Limited. Broadly, the company would continue strengthening its real estate investment management business and continuing a core investment in the office sector. The acquisition of property at 110 Carlton Gore Road, Newmarket, Auckland, is conditional, purely dependent on the success of the IPO before 31 March 2022. As per the management, the company will continue to assess market conditions and evaluate an approach in the interests of both existing Stride shareholders and potential investors.

As per the business update released on 3 November 2021, the portfolio of Stride Property Limited (SPL) is valued at $1,216.4 million as of 30 September 2021, up $13.7 million or +1.1% from 31 March 2021.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

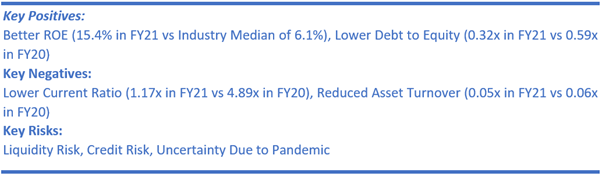

The stock has been valued using a P/E multiple based illustrative relative valuation method and arrived at a target price growth of low double-digit rise (in percentage terms). The company might trade at a slight premium to its peers’ average, considering a higher current ratio at 1.17x in FY21 versus an industry median of 0.74x and a lower debt to equity at 0.32x in FY21 versus an industry median of 0.42x.

We have taken peers such as Asset Plus Ltd. (APL.NZ), Precinct Properties New Zealand Ltd. (PCT.NZ), and Vital Healthcare Property Trust for the valuation purpose. (VHP.NZ) to name a few.

Considering the facts above and the current trading level, we give a “Buy” recommendation on the stock at the closing market price of $2.20 per share, down 0.90% as of 18th November 2021.

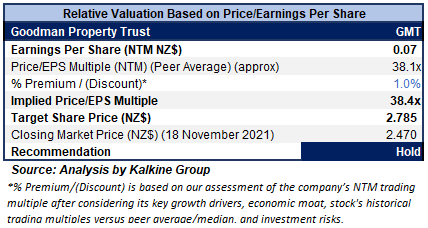

3) Goodman Property Trust (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.45 billion, Gross Dividend Yield: 2.643%)

Business Description:

Goodman Property Trust (NZX: GMT) is engaged in owning, developing, and managing industrial real estate globally, including logistics facilities, warehouses, and business parks.

Outlook

As per the H1FY22 interim result, statutory profit stood at $570.0 million before tax in H1FY22 (including investment property valuation gains of $504.7 million) versus $186.4 million before tax (including investment property valuation gains of $140.2 million) in H1FY21. Phenomenal new leasing, high occupancy levels, continuous rental growth, further development progress and strategic acquisitions have contributed to the 7.5% rise in operating earnings before tax to $60.2 million in H1FY22.

Despite current circumstances due to COVID-19, the company remains well-positioned for sustainable long-term growth. A solid-quality portfolio inclined on urban logistics will continue to benefit from the structural trends driving demand for distribution facilities close to consumers. Moreover, amid a low loan to value ratio of 17.5% and limited drawn debt facilities, as of 30 September 2021, the company retains over $300 million of available liquidity for future investment.

Valuation Methodology: Price/Earnings Per Share Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using a P/E multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to P/E Multiple (NTM) (Peer Average), considering its improved profitability in H1FY22 and the benefit of the scale of its portfolio that offers further opportunity.

For the valuation purpose, we have taken peers such as Lifestyle Communities Ltd. (LIC.AX), Home Consortium Ltd. (HMC.AX) and PEXA Group Ltd. (PXA.AX), to name a few.

Considering the above factors, a “Hold” rating has been assigned on the stock at the closing market price of $2.47 per share, up 1.65% as of 18th November 2021.

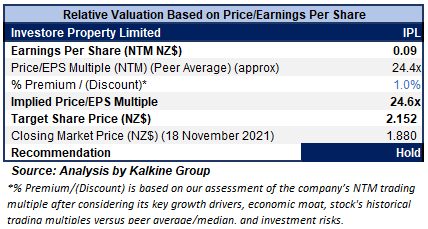

4) Investore Property Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$692.09 million, Gross Dividend Yield: 4.583%)

Business Description:

Investore Property Limited (NZX: IPL) invests in quality, large format retail properties throughout New Zealand and manage shareholders’ funds to maximise total returns over the medium to long-term.

Outlook:

The company continues to negotiate with its tenants about abatement arrangements that ensure profitability and sustainable businesses whilst minimising rental abatement costs. Further, the board is considering the issuance of a third listed bond in FY22. Moreover, it will continue to focus on growth strategy, as seen through the increased dividend guidance stated in August 2021. Cash dividend guidance for FY22 is indicated at 7.90 cents per share.

Valuation Methodology: Price/Earnings Per Share Multiple Based Relative Valuation (illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

The stock has been valued using a P/E multiple-based illustrative relative valuation method and arrived at a target price of low double-digit rise (in percentage terms). The company might trade at a slight premium to its peers’ average, considering its targeted growth strategy, with $83.8 million of acquisitions, contributing to the growth in the portfolio value of $1.15 billion as of 30 September 2021.

For the valuation purpose, we have taken peers such as Property for Industry Ltd. (PFI.NZ), Asset Plus Ltd. (APL.NZ), and Vital Healthcare Property Trust. (VHP.NZ) to name a few.

Considering the facts above, we give a “Hold” recommendation on the stock at the closing market price of $1.88 per share, down 2.59% as of 18th November 2021.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

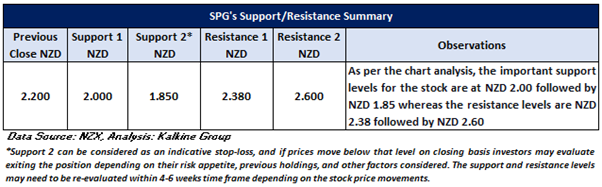

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...