This report is an updated version of the report published on 28th April 2022 at 5:07 PM (GMT +12)

I. Sector Landscape and Outlook

As per the Ministry of Business, Innovation and Employment (MBIE), the renewable energy share of the Total Primary Energy Supply (TPES) was ~39% in 2019. It is now expected to rise to 46% by 2035. Further, the government forecasts transport energy consumption to rebound by 7.8% in 2021, followed by a growth of 3.8% and 1.3% in 2022 and 2023, respectively. After that, demand for transport energy is forecasted to plateau for the next four years as the uptake of EVs (Electric Vehicles) increases.

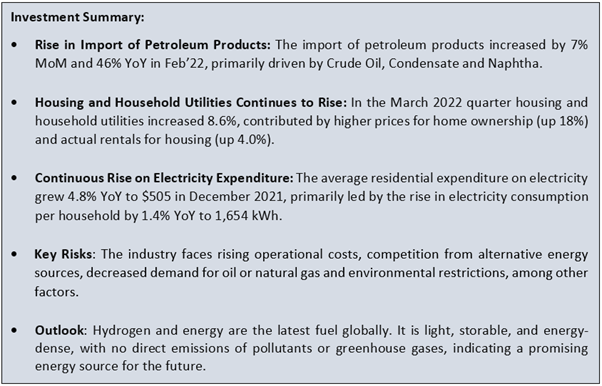

Import of Petroleum Products Increased in February 2022

As per MBIE, the import of petroleum products increased by 7% MoM and 46% YoY in February 2022, primarily driven by Crude Oil, Condensate and Naphtha, which grew by 5% MoM and 77% YoY in February 2022, followed by Diesel that grew by 59% MoM and 179% YoY and Other Petroleum Products that grew by 15% MoM and 139% YoY. The rise in imports could also be interpreted as volume risk, which originates from NZ being the net importer of petroleum products, indicating dependency on foreign suppliers. The second interpretation could be price risk, as oil prices are increasing dramatically in the international market on political risk.

Exhibit 1: Trend in Monthly Import of Petroleum Product Since January 2021

Data Source: This work is owned by the Ministry of Business, Innovation and Employment on behalf of the Crown which are licensed for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

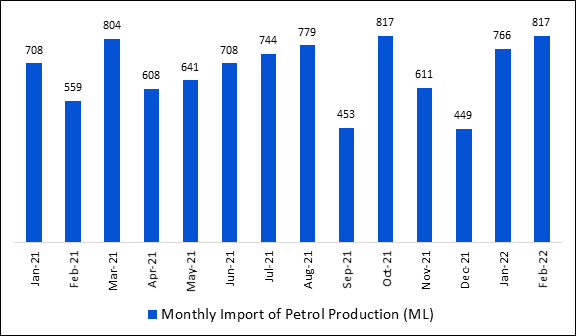

Rising Demand for Housing and Household Utilities

As per Stats.NZ, in the March 2022 quarter versus March 2021 quarter CPI Index, housing and household utilities increased 8.6%, contributed by higher prices for home ownership (up 18%) and actual rentals for housing (up 4.0%). Further, the transport group increased by 14.0%, contributed by private transport supplies and services (up 23.0%) and purchase of vehicles (up 5.6%). The rise in utilities and transportation group indicates rising demand for electricity and oil & gas consumption.

In March 2022 quarter, the average price for 1 litre of 91 octane petrol was $2.67, an increase from $2.45 in the December 2021 quarter and an increase from $2.00 in the March 2021 quarter.

Exhibit 2: Trend in Utilities and Transportation Groups in March 2022 Quarter CPI Index

Data Source: This work is based on/includes Stats NZ’s data which are licensed by Stats NZ for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Rise in Average Residential Expenditure on Electricity

As per MBIE, the average residential expenditure on electricity grew 4.8% YoY to $505 in December 2021, primarily led by the rise in electricity consumption per household by 1.4% YoY to 1,654 kWh. The nominal residential cost of electricity (including GST) grew 3.3% YoY to 30.50 c/kWh, contributed by an increase in lines component by 3.3% YoY to 11.62 c/kWh and energy & other components by 3.3% YoY to 18.88 c/kWh. This uptick in electricity consumption and pricing indicates a revival in demand and economic growth.

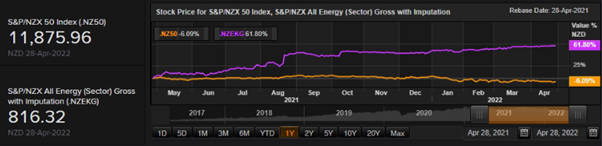

Index Performance:

The S&P/NZX All Energy (Sector) Index generated a 1-year return of ~61.80% versus ~-6.09% by the S&P/NZX 50 Index. Therefore, NZX All Energy Index overperformed NZX50 Index by ~67.89% in 1-year.

Exhibit 3: S&P/NZX All Energy (Sector) vs S&P/NZX50 Index

Source: REFINITIV

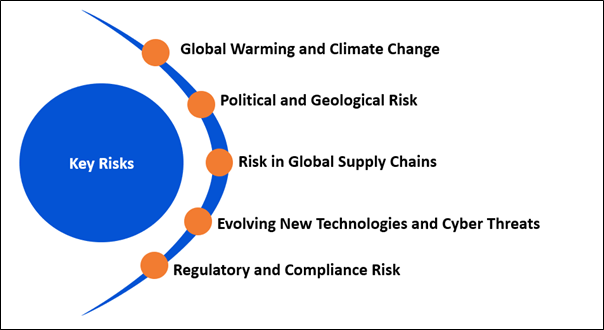

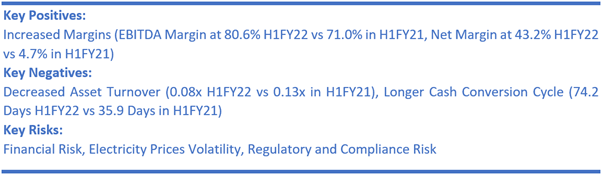

Key Risks and Challenges:

The government is working closely on projects to reduce carbon and improve air quality in the long run. It focuses on improving the quality of driving, periodical emission checks, engine replacement, and mass awareness.

Further, the geo-political unrest due to the war between Russia and Ukraine has increased international prices of crude oil, natural gas, coal, and other major commodities. These spikes are pushing inflation on fire, thereby denting the economy and hurting consumers in the short run.

Exhibit 4. Key Risks in Utilities & Energy Sector:

Source: Analysis by Kalkine Group

Outlook:

Hydrogen and energy are the latest fuel globally as it is light, storable, and energy-dense, with no direct emissions of pollutants or greenhouse gases. Hydrogen is expected to play a vital role in transport, buildings, and power generation. On 15 July 2021, NZ and Singapore signed an arrangement about cooperation on low-carbon hydrogen and drawn a framework for future cooperation.

As per the government, the operators expect a sharp rise in gas production, reaching a peak in 2024, primarily driven by drilling campaigns at Pohokura in 2022/23 and Maui and the continuing developments at Turangi, Mangahewa and Maui.

Apart from the sector-specific factors, we have also analysed four NZX-listed companies operating in the same sector. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Genesis Energy Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$3.00 billion, Gross Dividend Yield: 8.224%)

Genesis Energy Limited (NZX: GNE) is an energy company involved in the generation of electricity, retailing and trading of energy, and the development and procurement of fuel services.

Outlook

The company is continuously focusing on Future-gen strategy by signing additional power purchase contracts for wind, geothermal generation, and a joint venture contract with FRV Australia. It plans to build a pipeline of development opportunities. The company has guided FY22 EBITDAF to stay between $430 to $440 million subject to hydrological conditions, gas availability, any material events, one-off expense or other unforeseeable circumstances.

On 20 April 2022, the company released Q3FY22 performance report where from retail space, it reported Brand Net Promoter Score of 29 points, up 11 points on pcp, Gas Netback of $17.5/GJ, up 54% on pcp, and 67% of new C&I customers signed up to Energy Services in FY22 year to date.

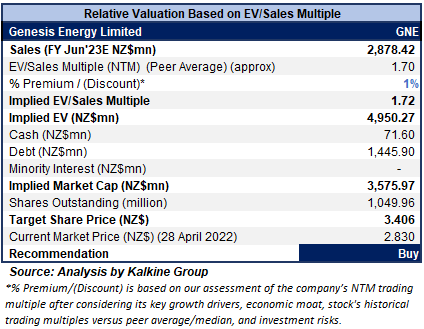

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

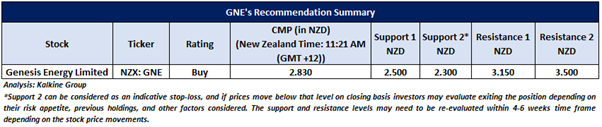

Stock Recommendation

The stock has been valued using an EV/Sales multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average) considering its future growth strategies and decent outlook.

Considering the aforementioned factors, we recommend a “Buy” rating on the stock at the current market price of $2.83 per share as of 28th April 2022 (New Zealand Time: 11:21 AM (GMT +12)).

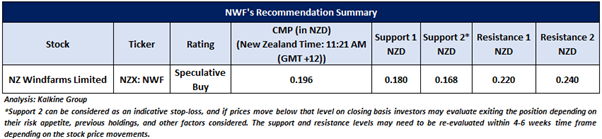

2) NZ Windfarms Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit) (M-Cap: NZ$56.75 million, Gross Dividend Yield: 4.150%)

Business Description:

NZ Windfarms Limited (NZX: NWF) is engaged in operating a wind power generation asset to generate and sell electricity.

Outlook

Decreased average wind speeds have impacted FY22 EBITDAF expectations. The revised FY22 generation is anticipated to be ~106 GWh based on actual generation. (FY21: 110.5 GWh). This generation impact is partially offset by higher fixed price for electricity in H2FY22 due to the VVFPA. Factoring the generation and an increased fixed price, FY22 EBITDAF is projected to be in the range of $6.5-$7.5 million, which is higher than $5.1 million EBITDAF in FY21.

On 21 April 2022, the company announced that it has received the Order in Council to have the project referred to a Panel for consideration under the FTCA.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation:

Considering the aforementioned factors, decent outlook, and the associated business risks, a “Speculative Buy” recommendation has been assigned on the stock at the current market price of $0.196 per share as of 28th April 2022 (New Zealand Time: 11:21 AM (GMT +12)).

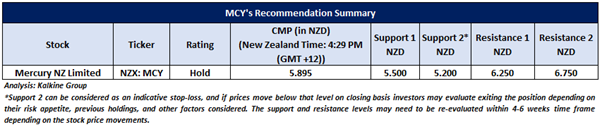

3) Mercury NZ Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$8.33 billion, Gross Dividend Yield: 4.328%)

Mercury NZ Limited (NZX: MCY) is engaged in generating electricity from renewable sources. The company sells electricity through its retail brands - Mercury and GLOBUG.

Outlook

The company projects full year EBITDAF ~$570 million indicating impacts of the Tilt Renewables and Trustpower retail acquisitions and excludes possible interim insurance payment arising from Kawerau station unplanned outage. The capex guidance remains at $70 million, ordinary dividend guidance remains at 20.0cps, fully imputed, indicating a 18% rise on FY21.

On 26 April 2022, the company announced that it is planning to make an offer of up to $200 million of unsecured, subordinated capital bonds to institutional investors and New Zealand retail investors. The proceeds are planned to be used to refinance drawn debt relating to the Trustpower Retail acquisition and for general corporate purposes.

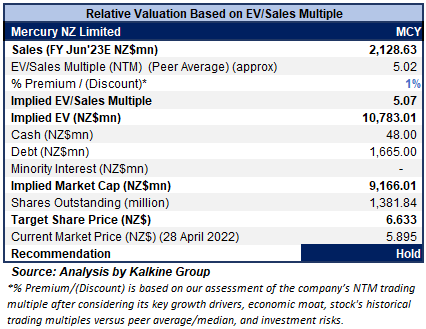

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

The stock has been valued using EV/Sales multiple-based illustrative relative valuation and the target price so arrived reflects a rise of low double-digit (in % terms). A slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average), considering its extensive renewable generation pipeline, and the acquisition of Tilt Renewables’ New Zealand that adds over 1,100GWh to its total annual generation.

Considering the aforementioned factors, we recommend a “Hold” rating on the stock at the current market price of $5.895 per share as of 28th April 2022 (New Zealand Time: 4:29 PM (GMT +12)).

4) Contact Energy Limited (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZ$6.38 billion, Gross Dividend Yield: 5.426%)

Contact Energy Limited (NZX: CEN) is involved in providing electricity, natural gas, and liquefied petroleum gas (LPG), along with broadband services. The electricity is generated through thermal, hydro, and geothermal sources.

Outlook

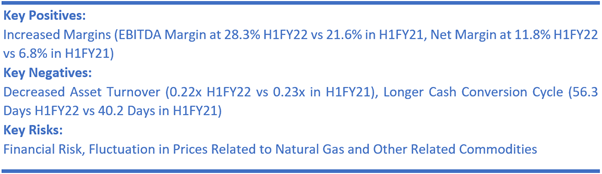

In the interim report of FY22, the company announced that it made decent progress on the Tauhara geothermal project despite COVID19-disruptions, with the power station’s expected capacity upgraded to 168MW, and the potential Tauhara geothermal field output upgraded by a further 0.2TWh p.a. Further, it plans to invest a further $37 million into a new afforestation partnership to strengthen further carbon capture through tree planting.

On 19 April 2022, the company released its March 2022 operating report where the customer business recorded an increase in mass-market electricity and gas sales of 298GWh (March 2021: 277GWh). The wholesale business also increased contracted electricity sales, including that sold to the customer business, totalling 627GWh (March 2021: 609GWh).

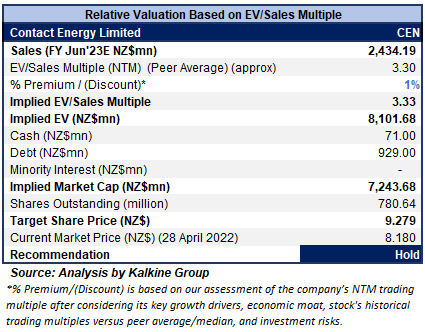

Valuation Methodology: EV/Sales Based Relative Valuation (Illustrative)

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Stock Recommendation

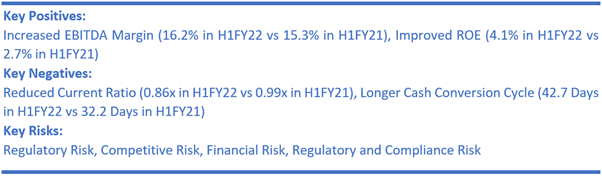

The stock has been valued using an EV/Sales multiple-based illustrative relative valuation, and the target price so arrived reflects a rise of low double-digit (in % terms). Accordingly, a slight premium has been applied to EV/Sales Multiple (NTM) (Peer Average), considering its strong financial performance in H1FY22 and robust balance sheet.

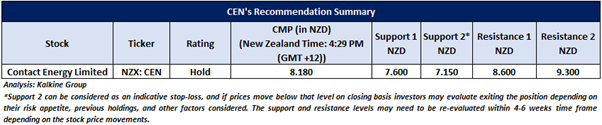

Considering the factors above, the current trading levels, and the associated business risks, we give a “Hold” recommendation on the stock at the current market price of $8.18 per share as of 28th April 2022 (New Zealand Time: 4:29 PM (GMT +12)).

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: The reference data in this report has been partly sourced from REFINITIV.

Note 2: Investment decisions should be made depending on the investors’ appetite on upside potential, risks, holding duration, and any previous holdings. Investors can consider exiting from the stock if the Target Price mentioned as per the analysis has been achieved and subject to the factors discussed above alongside support levels provided.

Technical Indicators Defined: -

Support: A level where-in the stock prices tend to find support if they are falling, and downtrend may take a pause backed by demand or buying interest.

Resistance: A level where-in the stock prices tend to find resistance when they are rising, and uptrend may take a pause due to profit booking or selling interest.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is authorised to provide general advice only. The information on this website does not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...