I. Sector Landscape and Outlook

According to the Reserve Bank of New Zealand, house prices in NZ are witnessing decline as mortgage rates are increasing. Nationally, the prices are down 11% as compared to November 2021 peak. Moreover, Wellington and Auckland have witnessed larger falls. Even though financial system as a whole is robust, certain households as well as businesses are expected to come under stress as a result of higher interest rate environment. The bank has been strengthening its regulatory, supervisory as well as enforcement frameworks in order to support financial system’s stability. The bank has highlighted that registered banks’ profitability was robust as there were lower levels of non-performing loans. Notably, New Zealand’s financial system is well positioned when it comes to handling an environment of higher interest rates as well as subdued economic growth.

Rise in Total Housing Lending Stock

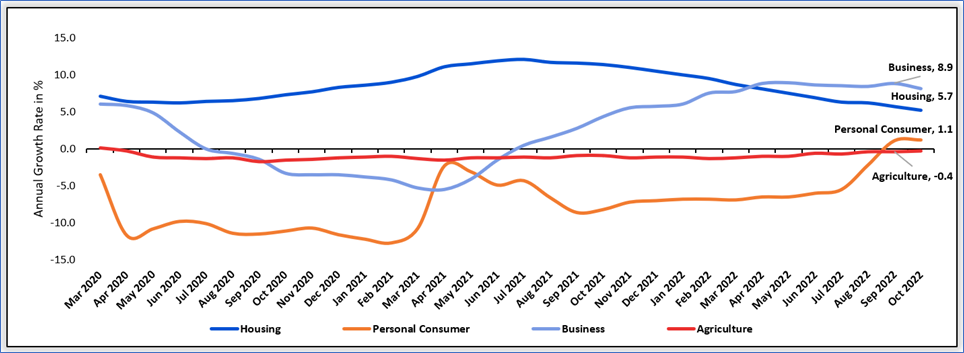

As per RBNZ, total housing lending stock witnessed a rise of $947 Mn (0.3%) in the month of October 2022. Also, the total personal consumer lending stock witnessed a rise of $117 Mn (0.9%) in the month of October 2022, thereby continuing the positive movement from the previous month. Notably, the annual growth rate remained positive this month. In the same release, RBNZ mentioned that total business lending stock rose $548 Mn (0.4%), reflecting a fall on the $1.6 billion increase which was witnessed in the last month. Therefore, annual growth witnessed a fall from 8.9% to 8.2%.

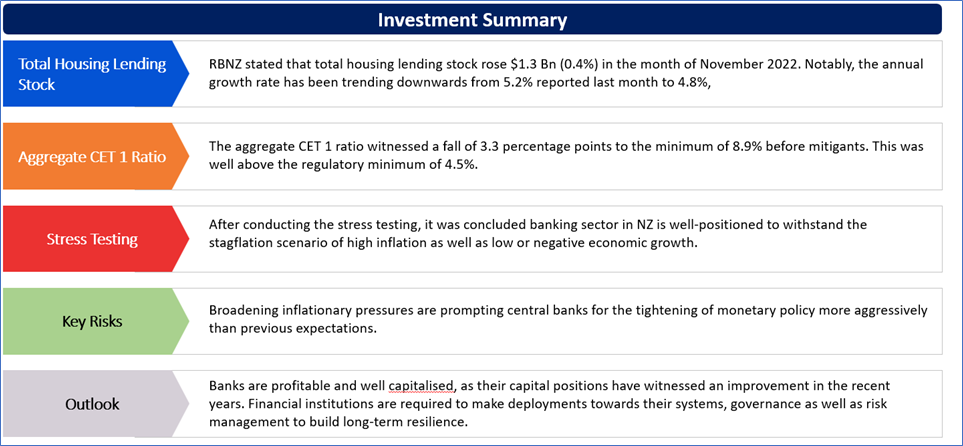

RBNZ stated that total housing lending stock rose $1.3 Bn (0.4%) in the month of November 2022. Notably, the annual growth rate has been trending downwards from 5.2% reported last month to 4.8%, implying the lowest annual growth rate since the month of February 2015.

Exhibit 1: Lending Pattern Since March 2020 – Banks and NBLIs

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Created by Kalkine Group

Stress Testing Reflects Decent Positioning

As per RBNZ, the 2022 bank solvency stress test included the stagflation scenario which shares elements of the present economic environment. It consisted of global downturn in broader economic activity. This is because central banks are increasing the interest rates due to high inflation as well as COVID-19 pandemic. After conducting the stress testing, it was concluded banking sector in NZ is well-positioned to withstand the stagflation scenario of high inflation as well as low or negative economic growth. Notably, this stability was partly because of the build-up of capital since global financial crisis.

The aggregate CET 1 ratio witnessed a fall of 3.3 percentage points to the minimum of 8.9% before mitigants. This was well above the regulatory minimum of 4.5%. The results before mitigating actions also reflect that the banks possess sufficient capital for lending. At the same time, they will be able to maintain capital ratios above the regulatory minima.

Credit Card Spending Patterns

RBNZ has released credit card summary report, wherein, NZ’s seasonally adjusted total billings witnessed a decline from $4.5 billion in the month of October to $4.4 billion in November, implying a decline of 2.6%. Notably, seasonally adjusted total advances outstanding in the month of November amounted to $6.2 billion. Compared with one year ago, this reflects an increase of 3.9% from $5.9 billion.

As per the report, total credit limits amounted to $21.3 billion (not seasonally adjusted), same as October. Therefore, total credit limits were 2.5% lower as compared to November 2021 and lowest since April 2015.

Insurers’ Solvency Margin To Remain Steady

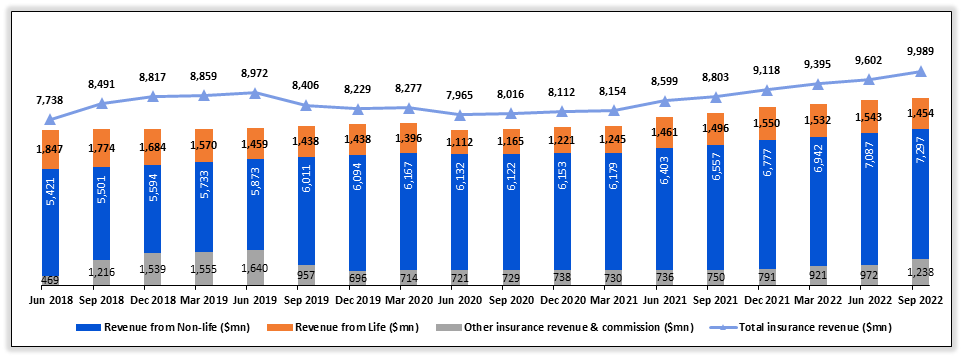

RBNZ, in their Financial Stability Report (November 2022), stated that NZ insurers have managed to retain capital during the COVID-19 pandemic period. This has supported the solvency ratios when there was economic uncertainty. High inflation has been increasing the claim expenses as well as premium, which might increase underinsurance. As per the report, general insurers are making up for the largest part of NZ’s insurance sector (~61% of the total gross premium revenues). Notably, life insurers are accounting for ~25 percent, and health insurers ~14%.

RBNZ stated that, in 2023, insurers are required to be in compliance with updated solvency standards. These reflect changes in the insurance accounting standards in IFRS17. For most of the insurers, the new requirements will make their published solvency ratios decline. However, this is because of the increase in the numerator of the ratio (actual capital held) as well as the denominator (minimum amount of capital that must be held).

Therefore, it would reflect the change in calculation rather than increase in risk. Notably, the dollar value difference between those two values reflects solvency margin, which is expected to remain steady.

Exhibit 2: Trend in Insurer Revenue in NZ ($million)

Data Source: This work is based on/includes rbnz data which are licensed by rbnz.govt.nz for reuse under the Creative Commons Attribution 4.0 International Licence; Chart Analysis by Kalkine Group

Index Performance:

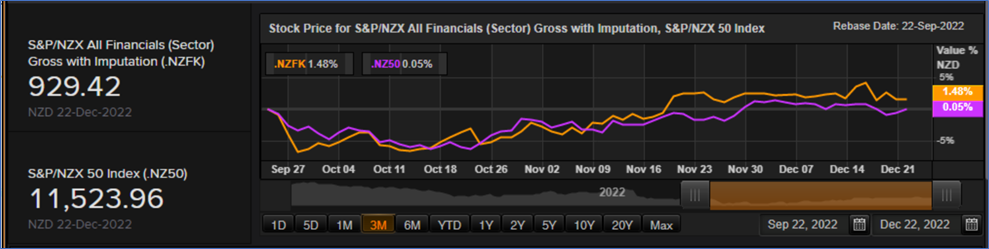

The S&P/NZX All Financials Index generated a 3-month return of ~1.48% versus ~0.05% by the S&P/NZX 50 Index. Therefore, S&P/NZX All Financials Index overperformed S&P/NZX 50 Index by ~1.43% in 3 months.

Exhibit 3: S&P/NZX All Financials Index vs S&P/NZX 50 Index

Source: REFINITIV

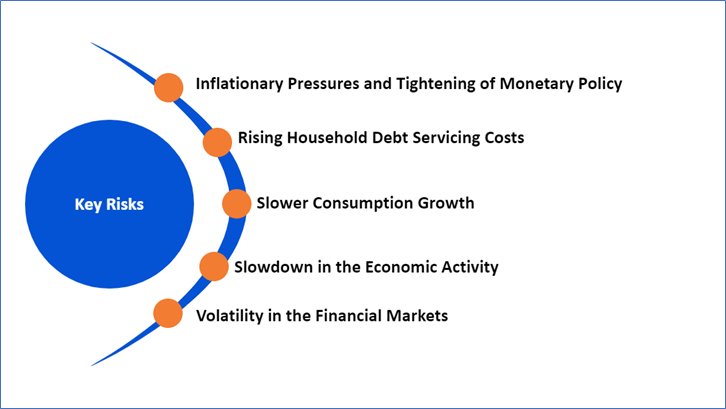

Key Risks and Challenges:

As per RBNZ, increased number of downside risks to the global economic outlook are present. Notably, broadening inflationary pressures are prompting central banks for the tightening of monetary policy more aggressively than previous expectations. The financial markets are volatile, and there has been increasing uncertainty regarding the extent to which economic activity could slow down due to the tightening of monetary policy. Therefore, financial stability risks have increased. Housing prices in NZ are declining as mortgage rates are increasing.

RBNZ highlighted that negative equity as well as mortgage servicing arrears are not widespread. However, they will grow if prices fall continuously and as mortgages reprice to increased interest rates. Another important concern is higher unemployment, which could lead to further stresses among households.

Exhibit 4. Key Risks in Financial Sector:

Source: Analysis by Kalkine Group

Outlook:

As per RBNZ’s annual report 2022, banks and insurers are operating in the robust position to provide support to the economy as well as financial services. Banks are profitable and well capitalised, as their capital positions have witnessed an improvement in the recent years. As debt-servicing costs rise as well as house prices decline after tightening of the monetary conditions, improved capital positions of banks would help their resilience to deterioration in asset quality.

Additionally, the reintroduction of loan-to-value-ratio restrictions managed to limit accumulation of higher-risk mortgage lending when house prices witnessed a significant increase during 2021. As at 30th June 2022, RBNZ held deposits from banks amounting to $45.1 Bn (2021: $30.5 Bn) as well as deposits and loans from the government of $34.6 Bn (2021: $40.4 billion). Notably, the increase of $14.8 Bn in deposits from banks was mainly because of lending under the FLP and TLF.

Financial institutions are required to make deployments towards their systems, governance as well as risk management to build long-term resilience. RBNZ has been focusing towards strengthening of regulatory, supervisory as well as enforcement frameworks in order to support financial stability in the long term.

Apart from the sector-specific factors, an analysis on two NZX-listed companies is provided. This report covers their insights, outlook, performance and potential as expected to be delivered in the near to medium term.

1) Kingfish Limited (Recommendation: Buy, Potential Upside: Low Double-Digit) (M-Cap: NZD455.52 million, Annual Dividend Yield (TTM) 1: 9.49%)

Business Description:

Kingfish Limited (NZX: KFL) is a New Zealand based investment company. It invests in various sectors, such as industrials, healthcare, utilities, consumer staples and information technology.

Outlook:

In November 2022, KFL’s gross performance return was up 2.4% as well as the adjusted NAV return was up 2.3%. This compares to the benchmark S&P/NZX50G, which rose 1.9%. The company has made portfolio adjustments over the last 6 months, and it is confident in the prospects for its portfolio of high-quality growth companies moving forward. KFL investors received distributions consistent with the company’s distribution policy (2% of average NAV per quarter) as it paid 5.99 cents per share to shareholders during the six months to 30th September 2022.

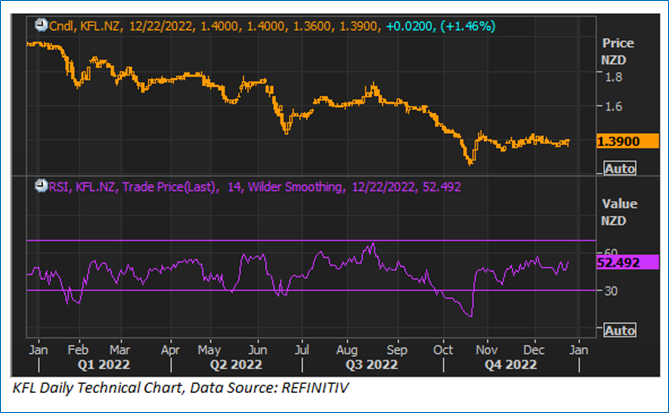

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Commentary:

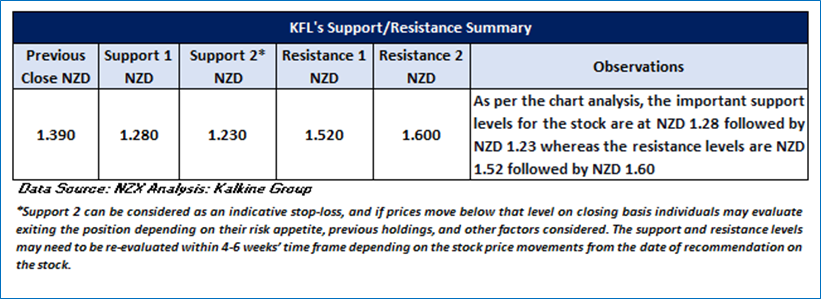

KFL stock prices have been in a consolidation phase in recent weeks, indicating a possible recovery going forward. On the daily chart, prices are hovering around the 21 & 50-period SMA, while the momentum oscillator RSI-14 period rises above midline (~52.49), suggesting a potential up move. On the higher side, KFL stock prices may face resistance near NZD 1.52 and NZD 1.60 levels, whereas it might struggle to test the NZD 1.28 and NZD 1.23 support levels.

Stock Recommendation

KFL has been deploying in the companies that have proven track record of growing profitability. Considering the aforementioned factors, a ‘Buy’ recommendation has been assigned on the stock at the closing market price of NZD 1.390 per share, up by 1.46% as of 22 December 2022.

2) Templeton Emerging Markets Investment Trust PLC (Recommendation: Hold, Potential Upside: Low Double-Digit) (M-Cap: NZD3.25 billion, Annual Dividend Yield (TTM)1: 3.35%)

Business Description:

Templeton Emerging Markets Investment Trust PLC (NZX: TEM) is an investment trust company. The Company’s objective is to provide long-term capital appreciation for private and institutional investors seeking exposure to global emerging markets, supported by a culture of both its customer service and corporate governance.

Outlook:

TEM is deploying towards the companies based on their individual attributes. Investment style is on finding good quality companies with sustainable earnings power and whose shares trade at a discount relative to their intrinsic worth. It focuses on companies which have high standards of corporate governance, respect their shareholder base and understand the local intricacies. The Company is confident that this approach will help to navigate the challenging market and economic backdrop.

Technical Overview:

Daily Price Chart

Source: REFINITIV, Note: Purple color line reflects Relative Strength Index (14-Period)

Technical Commentary:

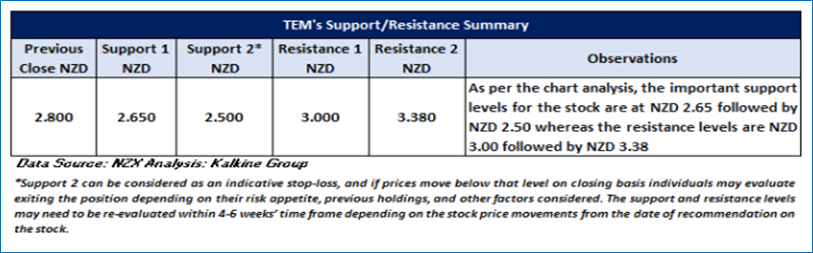

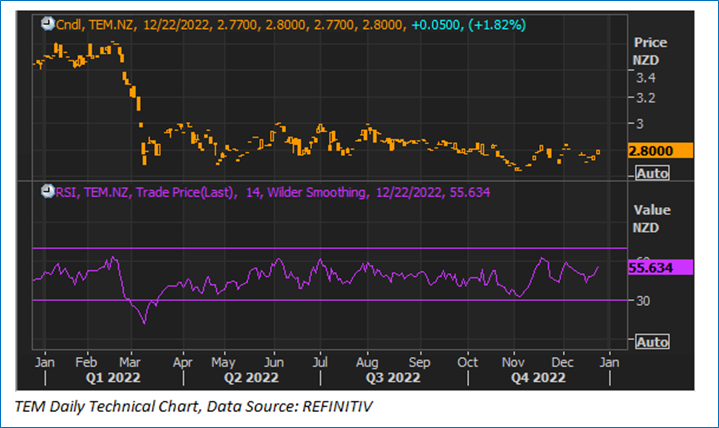

On the daily chart, TEM stock prices seem to rebound after forming a base near the immediate support at NZD 2.65 level. Currently, prices are holding above the 21 & 50-period SMA with a rise in volume in recent sessions. Moreover RSI-14 period is inching higher with a reading of ~55.63, suggesting momentum build-up in the stock. Moving ahead, a recovery is expected in the TEM stock, where prices may face resistance near NZD 3.00 and 3.38 levels. In contrast, support could be seen near NZD 2.65 and NZD 2.50 levels.

Stock Recommendation

Considering the facts above, a ‘Hold’ recommendation on the stock has been provided at the closing price of NZD 2.80 per share, up by 1.82% as on 22nd December 2022.

Markets are trading in a highly volatile zone currently due to certain macro-economic issues and geopolitical tensions prevailing. Therefore, it is prudent to follow a cautious approach while investing.

Note 1: Past performance is neither an indicator nor a guarantee of future performance.

Note 2: The reference date for all price data, currency, technical indicators, support, and resistance levels is December 22, 2022. The reference data in this report has been partly sourced from REFINITIV.

Note 3: Investment decisions should be made depending on an individual's appetite for upside potential, risks, holding duration, and any previous holdings. An 'Exit' from the stock can be considered if the Target Price mentioned as per the Valuation and or the technical levels provided has been achieved and is subject to the factors discussed above.

Note 4: Annual Dividend Yield is on a Trailing Twelve Month (TTM1) basis and are subject to change based on factors such as company performance, stock price changes, etc.

Technical Indicators Defined: -

Support: A level at which the stock prices tend to find support if they are falling, and a downtrend may take a pause backed by demand or buying interest. Support 1 refers to the nearby support level for the stock and if the price breaches the level, then Support 2 may act as the crucial support level for the stock.

Resistance: A level at which the stock prices tend to find resistance when they are rising, and an uptrend may take a pause due to profit booking or selling interest. Resistance 1 refers to the nearby resistance level for the stock and if the price surpasses the level, then Resistance 2 may act as the crucial resistance level for the stock.

Stop-loss: It is a level to protect further losses in case of unfavourable movement in the stock prices.

Disclaimer

Kalkine New Zealand Limited is a Financial Advice Provider (“FAP”) and is authorised by a Transitional FAP license issued by Financial Markets Authority (“FMA”) to provide financial advice. Kalkine provides only general financial advice through its research reports following a person becoming a member. The reports contain buy/sell/hold and other recommendations in relation to equity financial products. The recommendations and opinions [on this website] / [in this report] do not take into account any of your investment objectives, financial situation or needs. Before you make a decision about whether to acquire a financial product, you should obtain the Product Disclosure Statement from the product issuer. You should consider the appropriateness of advice taking into account your own objectives, financial situation and needs and seek independent financial advice before making any financial decisions. If you act on the advice in the research reports, you may have to pay fees, expenses or other amounts (but not to Kalkine). Further information about the complaints and dispute resolution process, as well as information about Kalkine’s duties are available on Kalkine’s website. Please read our Financial Advice Provider (FAP) disclosure statement and Complaints Handling Guide, which are available on the website.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...